This week, amid the hullabaloo over President Barack Obama's Deficit Dinner Diplomacy, and Sen. Rand Paul's 13-hour filibuster-cum-dissertation on drone strikes and civil liberties, financial news-watchers touted a milestone in their lives of Market Worship. We speak, of course, of the Dow Jones Industrial Average, which on Tuesday hit an "all-time high" of 14,253.77. The good times rolled steady on through the week, and the Dow closed Friday at 14,397.07.

Of course, the notion that these were "record" highs was not, strictly speaking, true. As Jeff Cox as CNBC pointed out, "in inflation-adjusted dollars, the Dow would need to hit 15,731.54 to break the record." Nevertheless, the exciting new ordinal number sitting on the stock market index set off a chorus of hallelujahs. After all, this was the highest mark it had hit since October 2007. (Of course, if we recall correctly, it was about that time that all of our more recent tragic economic events began to occur.)

The fluctuations of the Dow are typically pored over, by the media, in the same way the ancient oracles pieced through the entrails of birds, seeking for whatever path leads to the most prosperity. And in the world of politics, partisans on both sides are quick to point to the Dow as generic confirmation that their policies are working. As long as the story suits their narrative, anyway.

And those narratives can sure get woolly and weird quickly. Seemingly within moments of the Dow's peak, Nobel Laureate For Dumbness In Extremis and “Dow 36,000” author James K. Glassman was in the pages of Bloomberg View (proving once again that there’s a sort of “Greater Fool Theory” at work in the media, incentivizing normally sensible editors to immediately reach out to capture the point of view of the biggest nincompoops in their Rolodexes), crowing about how his old, failed predictions were well on the way to coming true.

Of course, as Jonathan Chait pointed out, Glassman has to toss out the entire underlying thesis of “Dow 36,000” (he and coauthor Kevin Hassett theorized that the stock market, circa 1999, was being so undervalued that it should have been at 36,000 in the days ahead of the massive tech-bubble bust, as opposed to theorizing “some day maybe the Dow will hit 36,000, probably, just you watch”) in order to claim vindication now.

Former Reagan domestic policy adviser Bruce Bartlett just called Glassman a “nitwit” and left it at that.

All of which leads to an obvious point: although we recognize that the long-term trend of the stock market is that it has an overall upward trajectory -- punctuated in snapshots by the susurrations of the greed/fear cycle -- it’s nevertheless catnip for a lot of wild-eyed prognosticators. And the over-reliance of using the stock market as evidence of economic recovery, or proof of economic fundamentals, is acute.

So what does it say about the Dow that it can hit this dizzying new height -- impressive by any measure in any era, post-crash or otherwise -- at a time when the overall global economic outlook is so dismal, and the domestic recovery is barely felt by the citizens who sacrificed their capital to save the world from calamity? It says that we should be gravely concerned. It says that we have a two-tiered economy, one where profits flow and another where risks lurk. It says that a lot of people are being left behind. And if October 2007 is any guide, it says that this display of prosperity may simply be an illusion.

The distribution of the stock market's largesse has been perhaps the most un-egalitarian aspect of American economics for years. A full 50 percent of all capital gains go not to the richest 1 percent of Americans, but to the richest 0.1 percent, according to The Washington Post.

But the stock market's persistent upward climb since the spring of 2009 has revealed another massive disparity: the multinational corporate machinery that generates stock gains has become unmoored from the economic reality in which the vast majority of Americans live and die.

The Dow hits a peak this week amid a host of gloomy global economic forecasts. Back in January, the World Bank “sharply reduced its estimate of global economic growth in 2013, projecting that the downturn in Europe and the United States’ fiscal problems will continue to weigh on investment and spending.” The World Bank's take on U.S. growth was similarly dismal -- its 1.9 percent forecast for the coming year was less than the most-pessimistic estimates from the Federal Reserve.” There’s no end in sight to the austerity orgy that’s exacerbating Eurozone pain -- despite the fact that the EU projects that their economy “which generates nearly a fifth of global output, will shrink 0.3 percent in 2013.” (Analysts are currently divided on whether or not China is also experiencing a slowdown at the moment as well.)

Closer to home, we received a gentle boost from this month’s employment numbers -- 236,000 jobs were created this past month (pending after-the-fact revisions in the months to come), which is closer to the ideal in terms of keeping ahead of labor market growth and digging out of the post-crash hole. The overall unemployment rate has subsequently dropped to 7.7 percent. But those numbers can mask a bevy of problems. As Matt Yglesias points out, the situation for the long-term unemployed is becoming a bona fide crisis that calls for “targeted interventions.”

And even if the unemployment number continues to drop, there’s a real concern over what sort of jobs are being added back to the economy. Will they be quality jobs that put those entering (and re-entering) the labor force on a sustainable path to household prosperity? Or is everyone heading to a future of toil in Amazon shipping warehouses? It’s worth being fretful -- many of those who will be entering the job market for the first time will be carrying student loans out of a period of sky-high college tuition, which taken as a whole, may form the backbone of the next great financial crisis.

Even as the economy has tipped and trended in the direction of what we might nominally call “recovery,” the answer to the question, “Who has recovered?” reveals some stark truths.

As University of California, Berkeley economics professor Emmanuel Saez calculated, losses in average family income during the Great Recession were felt across the board. Average real income per family declined by 17 percent. And the top income earners took it on the chin a little harder. As the bottom 99 percent experienced a 12 percent drop in average income, the uppermost percentile’s income fell 36 percent. As Saez reports, “The sharp fall in top incomes is explained primarily by the collapse of realized capital gains due to the stock-market crash.”

Of course, the top 1 percent nevertheless were largely sheltered from the stresses that afflicted the most vulnerable, as you would expect. What you perhaps didn’t expect was how the recovery distributed itself across the same groups (emphasis ours):

From 2009 to 2011, average real income per family grew modestly by 1.7% but the gains were very uneven. Top 1% incomes grew by 11.2% while bottom 99% incomes shrunk by 0.4%. Hence, the top 1% captured 121% of the income gains in the first two years of the recovery. From 2009 to 2010, top 1% grew fast and then stagnated from 2010 to 2011. Bottom 99% stagnated both from 2009 to 2010 and from 2010 to 2011. In 2012, top 1% income will likely surge, due to booming stock-prices, as well as re-timing of income to avoid the higher 2013 top tax rates. Bottom 99% will likely grow much more modestly than top 1% incomes from 2011 to 2012.

This suggests that the Great Recession has only depressed top income shares temporarily and will not undo any of the dramatic increase in top income shares that has taken place since the 1970s.

Much of the economic recovery is simply an increase in the value of financial assets: stocks and bonds. And most people just don't own stocks. In 2011, only 21 percent of American adults even had a 401(k) retirement account, according to a HuffPost analysis of data from the Investment Company Institute. Only 52 percent of all adults older than 65 receive money from financial assets at all, with half of that set receiving less than $1,260 a year, according to the Pension Rights Center.

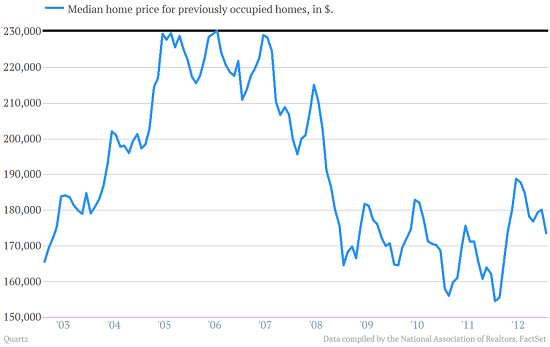

Growth that everyone relies on, like that of home values and wages, has been sluggish. At the end of 2012, the S&P/Case-Shiller home price index was roughly where it was at the beginning of 2009 (which was also roughly where it was in the fall of 2003).

And even as the stock market hits this celebrated peak, the wages that average Americans are bringing home to, you know, "put food on their family,” are plunging into a trough -- despite measurable gains in overall productivity.

In fact, as Robert Reich points out, the way those productivity gains are being achieved leaves out workers altogether, and they are coming about as a result of actions taken by policymakers:

Corporations have been investing in technology rather than their workers. They get tax credits and deductions for such investments; they get no such tax benefits for improving the skills of their employees. As a result, corporations can now do more with fewer people on their payrolls. That means higher profits.

Reich adds:

Joblessness all but eliminates the bargaining power of most workers -- allowing corporations to keep wages low. Public policies that might otherwise reduce unemployment -- a new WPA or CCC to hire the long-term unemployed, major investments in the nation's crumbling infrastructure -- have been rejected in favor of austerity economics. This also means higher profits, at least in the short run.

In other words, the labor force is being squeezed for every last drop of productivity, because employers know that they’re holding all the cards. If the economy were approaching full employment, discontented or overworked employees would have options and leverage. Right now, they don’t. If you’ve got a job, you need to hang onto it for dear life. That’s an environment for scraping out survival, not the economic mobility we rightly celebrate during boom-years.

Another thing to keep in mind is that the Dow is hitting this peak at a time when everyone in the world knows that the debate over the sequestration -- whose cuts have awesome recession-generating powers! -- has gone into vapor-lock, with the GOP refusing to compromise on raising revenues, through the very tax reform proposals that formed the basis of the party's recent presidential campaign.

Everyone has been warned about the consequences of the sequestration, it’s just that corporate America currently has the fortunate position of being able to greet the news with a shrug, as The New York Times reported this week:

With $85 billion in automatic cuts taking effect between now and Sept. 30 as part of the so-called federal budget sequestration, some experts warn that economic growth will be reduced by at least half a percentage point. But although experts estimate that sequestration could cost the country about 700,000 jobs, Wall Street does not expect the cuts to substantially reduce corporate profits — or seriously threaten the recent rally in the stock markets.

“It’s minimal,” said Savita Subramanian, head of United States equity and quantitative strategy at Bank of America Merrill Lynch. Over all, the sequester could reduce earnings at the biggest companies by just over 1 percent, she said, adding, “the market wants more austerity.”

Well, if that’s true, the market is going to love the dire, short-term consequences that the sequestration is going to bring to many Americans closer to the ground-level of the economy. Reich rounds up those who’ll be hit the hardest and most immediately: 125,000 people are going to lose their rental subsidies, 10,000 more will be cut off from similar subsidies intended to assist Americans living in rural areas, 100,000 people face getting kicked out of emergency homeless shelters, and cuts are coming to unemployment insurance, Title I education programs, Head Start, and anti-hunger subsidies.

It’s not like those who bid on the stock market can’t grasp the looming disaster, they’re just completely unconcerned. (As you may recall, the market didn’t exactly take to its fainting couch as the so-called “fiscal cliff” loomed, either, despite dire warnings of a market spasm.) That’s what carting off 121 percent of an economic recovery will do for a person, safely ensconced atop the income ladder.

Fittingly, even as the sequestration’s hammer is poised to come down, The Wall Street Journal reports that the market for luxury goods is booming.The newspaper characterizes this as evidence of the economic robustness, connecting “The economy has bounced back from recession” to “As a result, wealthy Americans are spending freely on expensive clothing, accessories, jewelry and beauty products.”

The Wall Street Journal quotes “HSBC luxury-goods analyst Antoine Belge” thusly, "Trends in luxury consumption in the U.S. have continued to outperform overall consumer trends" This is actually evidence that you and most of the people you know are getting left, far behind, in the post-crash economy.

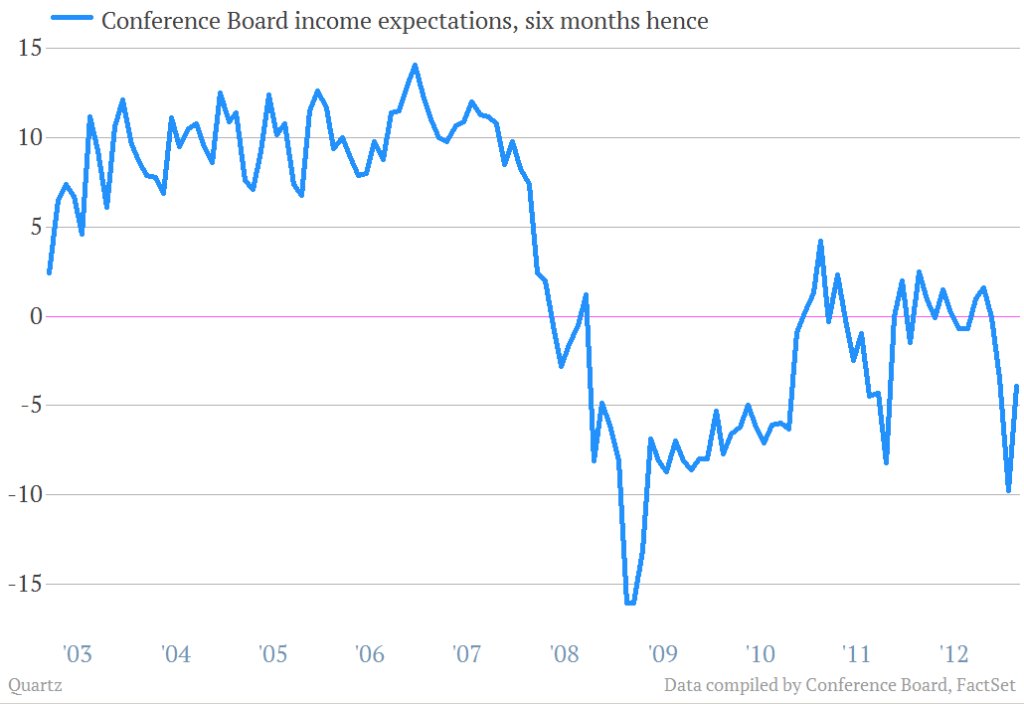

The average participant in the overall American economy isn’t fooled by any of this. They well know what Matt Phillips points out at Quartz, household incomes “haven’t gone anywhere but down.” As Phillips relates, “Real median US household income -- that’s “real,” as in “adjusted for inflation” -- was $50,054 in 2011, the most recent data available from the US Census Bureau. That’s 8% lower than the 2007 peak of $54,489.”

He goes on to show that consumer expectations strike a serious contrast with the mood from within the Dow Jones Revival Tent:

We are led, then, inevitably, to a conclusion that we all feel, but no one says aloud. The American middle class, in other words, no longer lives in a financial economy. But the gold-standard economic metrics that we hold out as the key measurements of prosperity -- the economy of Wall Street, of gross domestic product figures, and the Dow Jones Industrial Average is purely financial.

For the time being, assume that you and everyone who you care about is screwed. Congratulations.

[Would you like to follow me on Twitter? Because why not?]

(Editor's Note: We compared 2007 data to the most recent full-year data. This explains why some most up-to-date data is from 2011.)