The nation's payrolls grew by 217,000 last month and the unemployment rate held steady at 6.3%, according to this morning's report from the Bureau of Labor Statistics. It's a good report, solidly in line with expectations. One could make the case that the job market has settled into a decent trend, adding north of 200,000 jobs per month.

But before I'd make that case, I'd want to see growth that's significantly above trend for a number of months in order to tighten the job market sooner than later. That is, in a job market that's at full employment, the trend is your friend. But with remaining gaps in jobs, wages, and participation, there's a danger of settling into the trend too soon.

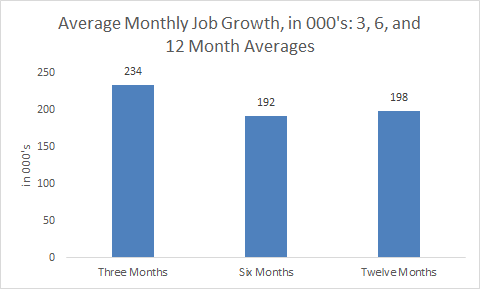

The figure below shows average monthly job growth over the past three, six, and twelve months--I find this to be a useful way of pulling recent trends out of the bouncy monthly data. The underlying pace of payroll job growth has accelerated in recent months from around 200,000 to around 230,000. Especially given the low rate of labor force participation, that should be fast enough job growth to lower the unemployment rate, and of course, it has been falling in recent months.

However, much of that decline has been precisely due to the declining labor force, and the participation rate was unchanged in May, holding at 62.8%, 0.6 percentage points below last May's level, and sticking at rates we haven't seen since the late 1970s. To be sure, part of the decline is demographic, as boomers phase out of their working years, but part--I'd say maybe half the decline off of its pre-recession peak--is a function of persistently weak labor demand.

Real wages, another important measure of slack, were up 2.1% over the past year, and this too is both around where it's been lately and about the pace of recent inflation readings, implying stagnant real earnings. Interestingly, however, production/non-managerial wages--a series that broadly tracks median pay--grew a bit faster, up 2.4%, perhaps signaling an improvement in the mix of net new jobs in terms of quality.

That said, many labor-market watchers expect the negative trend in the LFPR to partially reverse as the job market tightens; similarly, a tighter market should lift workers' bargaining power and place some upward pressure on wage growth. We did not see much of either last month and thus slack remains a serious labor market problem.

A few other notables from the morning's report:

-Long-term unemployment (jobless for a least six months) remains elevated, though it's coming down. The share of long-termers among the unemployed was 34.6% last month, the lowest share since 2009. As a share of the labor force, long-termers were 2.2%. Note that whenever this metric has been this elevated, Congress has extended UI benefits. Yet, at great cost to both the unemployed and the macro-economy (UI has a big multiplier--the unemployed spend the money), they failed to do so at the end of last year, despite the obvious remaining weakness in the job market.

-The most expansive measure of under-employment--the U6 rate, which includes over seven million involuntary part-timers--ticked down to 12.2%, its lowest rate in the recovery which began in the second half of 2009. That too signals tightening, but it also reflects the downward bias in the unemployment rate due to labor force exits.

-There will be some fireworks today because total payrolls have finally climbed back to where they were before the recession. Payrolls fell by 8.7 million from January 2008 through February 2010, when they started to rebound. As of last month, they've added back 8.8 million.

That's obviously good news, but again--context is essential: we've filled a big job hole and we're back at ground zero--more than six years later! Yes, of course it's a very good thing to be back at ground level. But it's also a very low bar. The goal must be full employment, and after all this time, we're still not there.

This post originally appeared at Jared Bernstein's On The Economy blog.