The NYT's middle-class income series is back with an interesting list of the factors most commonly cited for the slump in median income in the U.S. (I posted a few initial thoughts about this series here). Though they left out a really important one (but you have to read this to the end to find out what it is).

Allow me to hold forth a bit on a few of the causes I think are most important (or less of a big deal). But first, one technical point: all of these causes are often discussed not in the context of slowing real income growth but in the context of increasing income inequality. It is implicit in the NYT series, I think, that aggregate income growth diverted from the middle class -- a feature of growing inequality -- is a "mechanical" factor leading to what they call the "income slump."*

Automation or technological change. The culprits here, as stated in the blurb next to the cause, are a) "labor-saving" technology, like robotics, and b) today's jobs demand more technical skills. "A" may well be in play but despite the fact that "b" is one the most commonly cited causes by economists, I'm a lot less convinced.

My hesitation can be summarized in one word: acceleration. It's a key concept in all of this causal analysis. It's not enough to cite a factor like tech change, demographic change, or globalization as something that hurts income growth. You have to show that this factor becomes more important over the period when incomes slowed.

Thus, you have to show that the factor became more prevalent, as in there was more global trade, faster demographic shifts, or in this case, a faster pace in the growth of employer skill demands. Or you have to show that for some reason, the steady pace of something that's been going on forever, like technological change, has a bigger impact on income growth over the period when that growth slowed.

This is rarely done. When Larry Mishel and I looked at this in the context of wage inequality, we found no statistical evidence for acceleration, so we found it hard to blame technological change, something that's literally been going on forever, as the cause of something new -- increasing wage inequality.

I do, on the other hand, wonder if the pace of labor-saving technology, like robotics, has in fact accelerated, as you can read about here.

Globalization. Global trade provides a good example of what I was talking about above. Figure 1 from this paper -- a paper that influenced a lot of people in this debate -- provides clear evidence of acceleration in import penetration from China over a period when middle-incomes were slumping pretty badly.

The slowdown in education attainment. I'm concerned about this one for a lot of reasons, particularly in terms of diminished economic mobility, and particularly for kids from less advantaged economic backgrounds.

But I'm not sure how much of it has to do with the income slump. In fact, recent wage analysis suggest college workers' real wages have also been a pretty slumpy of late (BTW: very important to focus on four-year college degree holders here -- trends are different and more favorable for those with advanced degrees beyond BA's).

There's a bit of a "Say's Law" fallacy to this part of the discussion -- increase the supply of college workers and you'll increase the demand for them.

Like I said, I'm not convinced. Which is by no means to say that kids shouldn't go to and finish college. They should. But I'm not sure how much that will do to offset the income slump.

Fiscal policy/tax code (and more!). As much as I like to point out that GW Bush's fiscal policy is a key factor in our past, current, and future budget deficits, the fact is that after-tax median household income has grown considerably faster than pretax over the recent slumpy period (as per CBO income data). However, don't get too cozy with that result; we simply can't count on middle-class tax cuts to continuously -- year-after-year -- offset the fundamental economic factors depressing middle-class income growth.

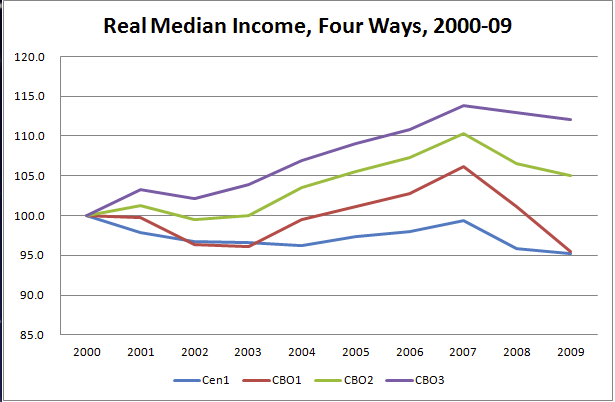

The figure below makes this case, and actually, a lot more cases. It's a collection of different series -- not all of which are as consistent as they should be -- on real median household incomes, 2000-09, indexed to the first year in the series to make it easier to compare growth paths.

Source: Census Bureau and CBO (see text)

Source: Census Bureau and CBO (see text)

The first series -- Cen1 -- is the only one directly from the Census Bureau and is just real, pre-tax, market income of the median household without any of the add-ons/adjustments made by the CBO in their very comprehensive series. Excuse the inconsistencies -- e.g., the Census series is not adjusted for HH size (which actually doesn't matter over this relatively short period) -- but I plotted it because a) it most clearly shows the slump, and b) some of the CBO ad-ons, especially the value of employer-provided health care -- are controversial.

CBO1 is market income as above with a bunch of stuff added in -- see here for definitions, but I think the most important one is employer-provided health care (more on why I'm concerned that this addition imparts an upward bias in a later post).

CBO2 adds government transfers, including the value of non-cash ones like Medicare (note that cash transfers are also in Cen1 -- I just don't have the data I need to make clean comparisons here yet -- sorry).

CBO3 is after-tax (federal only), which grew faster than the others in part because federal tax liabilities went down in these years. Note also how tax breaks helped insulate median HHs from the full ravages of the Great Recession (see here for more on this point).

So, I don't think you can blame fiscal policy for the slump, but two points. First, fiscal policy that fails to raise needed revenues will make it impossible for an amply funded government to support measures like educational access or countercyclical policies. This in turn will hurt -- is hurting -- middle class income growth.

Second, to punt on the pretax outcomes and figure we'll offset the lost market income through tax breaks can work every once in a while. It cannot work over decades.

Finally, a big, egregious omission from the NYT's list: Full Employment, as I discuss here and wrote a book about here (with Dean Baker). History is very clear on FE's role in boosting the incomes of low- and middle-income families -- a phenomenon we saw as recently as the latter 1990s. I'll have more to say about that in a follow-up post as well, but it's hard for me to imagine solid, sustainable, pretax middle-class income growth without it. So please, NYT -- add it to the list so people can vote for it!

*I've been working on these issues for decades, particularly through nine editions of the State of Working America. In that regard, I should cite my various co-authors with whom these ideas were developed, especially Larry Mishel, but also John Schmitt, Heather Boushey, and Heidi Shierholz.