Yesterday the Justice Department announced that once again it's not going to pursue evidence of Wall Street crimes which has been sent its way. It has already failed to act on information sent to it by sources whose investigators are apparently more dogged than its own, including several other government agencies and the Financial Crisis Inquiry Commission. Now the bipartisan committee which was led by Senators Carl Levin and Tom Coburn can be added to the list of sources whose leads weren't pursued by Attorney General Eric Holder and his staff.

Holder was on the defensive yesterday, a sign that the mounting criticism of his inaction is getting his attention. He was also scornful of that criticism, saying that it's belied by "a troublesome little thing called facts."

There's something troublesome here, all right, but it isn't the facts.

A Justice Department press release announced that there will be no prosecutions based on the Levin/Coburn report:

After a careful review of the information provided in the report and more than a year of thorough investigation, the Department of Justice... the FBI and the Special Inspector General for the Troubled Asset Relief Program (and other agencies) have determined that, based on the law and evidence as they exist at this time, there is not a viable basis to bring a criminal prosecution with respect to Goldman Sachs or its employees in regard to the allegations set forth in the report.

The press release goes on to say:

the department and its investigative partners conducted an exhaustive review of the report and its exhibits, independently gathered and scrutinized a large volume of other documents, and tenaciously pursued potential evidentiary leads, including conducting numerous witness interviews.

The D.O.J. also boasts that "Since FY 2011, the Department of Justice's financial fraud enforcement efforts have resulted in at least $185 billion in civil and criminal forfeitures, restitution, civil settlements and other penalties." (Bankers have continued to collected huge salaries and bonuses, however, so the lack of criminal prosecution gives them no reason to stop committing crimes.)

The statement goes on to describe D.O.J.'s "aggressive" pursuit of bank fraud, adding that "The Department of Justice has not hesitated to investigate and take enforcement action when the evidence and facts support doing so."

Holder himself was considerably more testy: "There have been, I guess, 2,100 or so mortgage-related matters that we have brought here at United State Department of Justice. Our state counterparts have done a variety of things. The notion that there has been inactivity over the course of the last three years is belied by a troublesome little thing called facts."

Unfortunately, the Holder Justice Department has had a troublesome relationship with facts. That dates back to its ginned-up and ultimately discredited claims about something called "Operation Broken Trust," in which it claimed credit for dozens of mortgage-related convictions that it said had resulted from a coordinated operation of that name. As the New York Times noted, many of those investigations had actually concluded before the 2008 election, Holder's appointment, and the creation of "Broken Trust." The Columbia Journalism Review gave its review of the fiasco the headline "Obama Administration's Financial-Fraud Stunt Backfires."

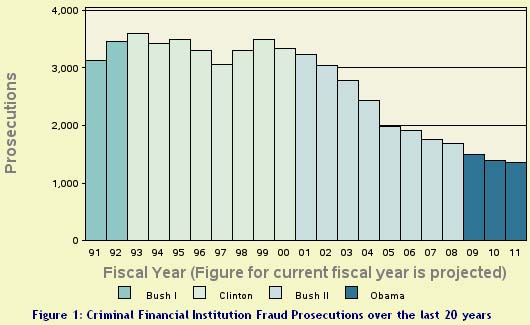

Then there's the graphic evidence of inactivity since the election of President Obama and the confirmation of Attorney General Holder, courtesy of Syracuse University's TRAC project:

(On the other hand, prosecution of immigration cases has soared under this administration.)

Most tellingly of all, there are the insider comments which suggest that the Justice Department has been dragging its feet in providing the mortgage fraud task force with the extremely modest resources it was promised (roughly 100 staff members to investigate a trillion-dollar fraud that involved all of the major U.S. banks, as opposed to 1,000 for the much smaller savings and loan scandal of the 1980s).

And despite Holder's claims, the convictions obtained over the least three and a half years have been strictly for small fry. The Justice Department hasn't even tried any cases against major financial executives, despite seemingly overwhelming evidence which includes:

The AIG allegations: We used the Levin/Coburn Report to review the list of potential criminal activity in that case here.

GE Capital deceptions: That's the company whose politically-connected CEO was given a presidential appointment. Referring investigators were stunned to find that no criminal charges would be filed over its fraudulent deception of investors, even though they had identified specific individuals in the accounting department who had cooked GE's books. GE Capital has also been implicated in fraudulent mortgage practices.

Wells Fargo drug-money laundering: That's the case in which bankers laundered money for the Mexican cartels that have killed tens of thousands of people. You know the gangsters we mean -- they're the guys who decapitate people.

JPMorgan Chase's "London Whale": With particular concern about the cover-up of billion-dollar losses, with special concerns about CEO Jamie Dimon's statement to investors that its London losses were "a tempest in a teapot." Dimon later admitted he had made mistakes. (If he had made false statements to investors, that would be stock fraud, a crime.)

And there are others, too numerous to mention all of them here: Countrywide. Citigroup. HSBC. The list goes on and on.

The Justice Department's argument for inaction seems to come down to this: Bank cases are complicated. They're hard to win. We don't want to try. And it has repeatedly used an argument that's also been made by the president and Treasury Secretary as well, as they've tried to explain away the inactivity: that bad banking behavior isn't necessarily criminal behavior. That claim's been repeated many times, especially in the context of "ABACUS" and other Goldman Sachs misdeeds contained in the Coburn/Levin report.

But it's not true. It's already illegal to lie to clients, to knowingly conceal important information from in order to get their money under false pretenses, or to withhold materially important information from shareholders. And yet that flimsy argument seems to lie at the core of the DOJ's explanation for once again declining to pursue the evidence wherever it may lead.

Here's what really happened in this case: Goldman was selling its clients "crap" investments (a Goldman employee's word), and which it knew to be "crap," while at the same time betting against those investments. And it concealed the fact that these investments were selected, not by the people it told investors were doing the choosing, but by somebody who was well-known for betting against the "crap" -- and who would make a fortune if they failed.

Under the massive civil settlement for ABACUS, the parties acknowledged that it was a "mistake" for Goldman marketing materials to claim that "the reference portfolio was 'selected by' ACA Management LLC without disclosing the role of Paulson & Co. Inc. in the portfolio selection process and that Paulson's economic interests were adverse to CDO investors."

"Mistake"? That's more of the linguistic evasion that's used when crooked bankers pay hundreds of millions to settle criminal and civil charges while "neither admitting nor denying wrongdoing." Goldman paid a record amount -- more than half a billion dollars -- to settle this case. The total settlement came to 550 million dollars. That's 550 million admissions of wrongdoing.

As they say: Money talks.

We're not into speculating about the motives for the Justice Department's inaction. But it's not surprising when others who do come to unflattering conclusions, and not just about Holder. This is an issue which the president himself will ultimately have to address -- for his campaign, and ultimately for his legacy.

Meanwhile, the cases the Justice Department hasn't prosecuted have led to billions of dollars in settlements. Eric Holder says that his department and this administration are doing everything they can to prosecute Wall Street fraud and make sure it doesn't happen again. There's only one thing that makes that statement hard to believe: It's a troublesome little thing called "facts."