The economy is not clicking along like it should -- the recovery is slow, halting and uncertain. The United States now has a large cadre of long-term unemployed, and many of them are in their twenties and early thirties.

These people are obviously not saving for retirement. Many of them are living at home, many are working at low-income jobs and many are facing student loans and other debts that have immediate priority.

Their parents, mostly Baby Boomers, might help make up this retirement deficit. Now is the time for Boomers to start considering whether they should. If resources are limited, it may well be wiser to help prepare children for retirement than to help with their current bills.

The Numbers

Financial planners know that saving early in a career is crucial to meeting retirement goals. A recent article in The Wall Street Journal illustrated that more than half of a successful 40-year retirement accumulation can come from savings in the first 10 years of working life.

The implications for today's young people are serious: if they miss the first 10 years of retirement saving, they will need to double their savings rate. Instead of saving, say, 10 percent of their incomes for 40 years, they will need to save 20 percent for the remaining 30 years to make up for missing the first 10 years.

If parents decide to help, how much should they save for a child's retirement? A reasonable answer is that they should save 10 percent per year of what they believe a normal income would be for their child. If their children expected to be earning about $40,000 per year during their early career, parents should plan to invest $4,000 per year on each child's behalf.

If young people save 10 percent of a constant real income for 40 years, if the real returns are six percent annually on their investments, they can have a retirement income from their investments that will approximate their working income. If the real returns average five percent annually, they will accumulate enough to provide a retirement income of 75 percent to 80 percent of their working income. These conclusions are based on running the 40-year accumulations through ImmediateAnnuities.com, which offers estimates of lifetime incomes, state by state, for any stipulated retirement accumulation.

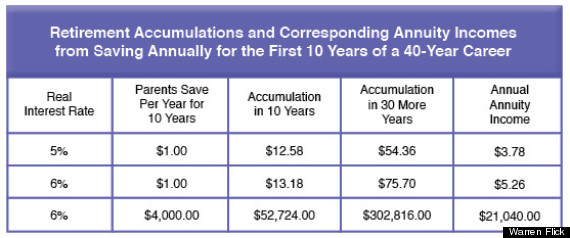

Here are general results for a five percent and six percent real, annual, interest rate:

For two real interest rates and each dollar saved annually for 10 years, the third column shows the amount accumulated at the end of the 10-year period. The fourth column shows what that 10-year amount would grow to over 30 more years.

The results can be easily scaled to describe any amount of annual savings by parents. For example, the third row of the table shows the results if parents saved $4,000 (10 percent of an expected $40,000 salary) per year for 10 years at six percent interest. At the end of the 10 years of saving, they would have almost $53,000, and 30 years of additional growth will produce an accumulation of almost $303,000.

Parents can choose among a large variety of investment vehicles, depending on the needs of their particular families. They may set aside money in their own investment or retirement accounts, earmarking it for their children. Then if the parents needed the money themselves, they could use it. Parents might gift the money annually, asking their children to invest it in a retirement account. And parents and children may elect any asset allocation that fits their risk tolerance and other characteristics.

No one can predict 30 or 40 years of their children's lives. The point is merely to set some reasonable savings goals to provide some extra help for currently unemployed children when they reach retirement age.

Beyond the Numbers

Setting aside $4,000 per year per child adds up quickly. There are many parents who cannot afford to set large amounts aside for their children. For parents who choose to help, the task may involve sacrificing some of their own retirement plans.

The task may be difficult for family reasons as well. There may be several children that need help, and there may be issues of fairness. Family traditions or beliefs may prompt parents to ask adult children to earn this additional support, which may create considerable tension within the family.

Yet for those families interested in helping their adult children, one of the best ideas may be to let the children deal with their immediate problems as best they can while parents set money aside for their children's retirements.