While most mid-lifers’ hands have been wringing about what menacing changes President-elect Donald Trump has in store for Medicare, Social Security, and their retirement funds, there is a fourth leg on the aging stool that few are talking about: Long-term care.

Truth is, whatever a Trump administration has in mind for long-term care, it probably can’t make things any worse.

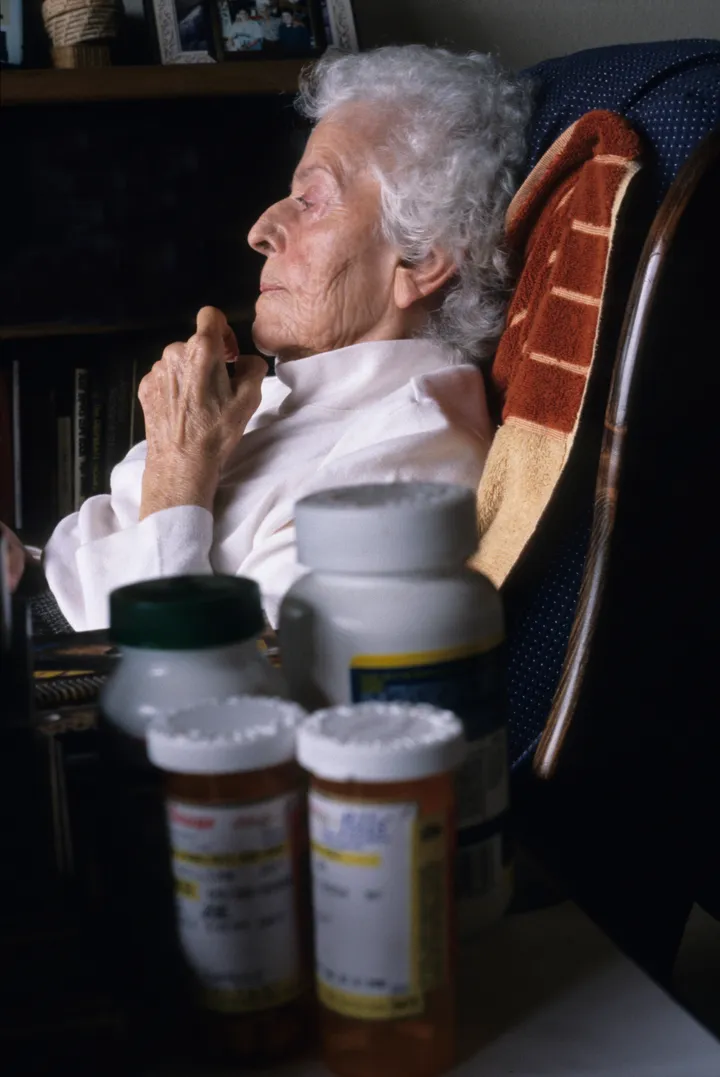

Long-term care is a euphemism for a skilled nursing home ― the place everyone says they want to avoid. The average annual cost of a nursing home is more than $92,000, according to Genworth. Make that $112,000 a year if you live in California or $136,000 if you live in New York.

Other than lottery winners, the 1 percent and the Trump kids, very few people can afford it. A few ― and we do mean a very few ― buy long-term care insurance policies with the idea of defraying the costs of a nursing home stay should one become necessary.

First a few facts: There is a 70 percent chance you will need some kind of long-term care after age 65 ― but know that 40 percent of those who receive long-term care are under 65. And eight percent of people between ages 40 and 50 have a disability that could require long-term care services.

We’re not talking about a week spent in a nursing home after a major surgery, either. The average need for long-term care is 1,040 days, according to the American Association for Long-Term Care Insurance. For the mathematically challenged, that’s almost three years.

And no, Medicare won’t cover it. Medicare, the subsidized health care program for those 65 and older, covers the kind of skilled short-term nursing care you might need after a hospitalization, but it won’t pay for permanent assistance. Medicaid ― the health care program for low-income people ― will cover nursing home care, but only for those with limited assets. Not all nursing homes accept Medicaid patients, and you won’t have much say about what facility dad will go to if Medicaid is paying the bills. To get Medicaid to pay, patients must spend down their assets according to guidelines set by their state. Think “spend down,” as in very down. Many people enter a nursing home or assisted living facility paying for their care out of their own pocket, and then apply for Medicaid when they basically go broke. Oh, you were hoping to leave the kids a little something? Good one.

So this leaves us with long-term care insurance. It is expensive, premiums go up, and it often provides only limited benefits with many restrictions and conditions that may end up with only a small percentage of your total long-term care costs covered. In some case, you may get nothing at all, says NOLO.

As far as insurances go, this one pretty much sucks ― which may be why 95 percent of the population doesn’t have it. Consumer and financial experts say LTC policies are a bad investment unless the monthly premium is 5 percent or less of your monthly income. When calculating that 5 percent figure for future years, bear in mind that the premiums will rise while your income will drop.

How many of us will be staring down the barrel of long-term care problems in the future? Many. The Congressional Budget Office estimates that by 2050, 20 percent of the U.S. population will be 65 or older, up from 12 percent in 2000. And if things are tough now, what will replace our current rickety system of Medicare, Medicaid and crappy private insurance that few have anyway? Wouldn’t a nice publicly financed insurance program be a lovely way to Make America Great Again?

Trump is silent and no one is holding their breath. But it’s good to have at least one thing he really can’t make worse.

Related

Before You Go