In a post the other day about the Federal Reserve and inflation, I noted that a commonly used rule to gauge where the Fed should set the Federal Funds Rate (FFR) was pointing at around -2 percent right now. However, I noted that:

...if you tweak that calculation in a way that I think you should, i.e., by increasing the measured unemployment rate to reflect its downward bias due to people leaving the labor force because of weak labor demand, then you find that the FFR should be more like -4 percent. No wonder we're stuck in such a slog. (Later, I'll post something showing these calculations.)

It's now later.

There are various different rules and techniques for estimating the optimal FFR, but John Taylor's rule is probably the most common.* There are different versions of this rule and the one I favor is partly driven by the gap between the full employment unemployment rate and the actual rate. The larger that gap, the lower the FFR should be.

But one problem with applying that formula right now is that, as noted, the unemployment rate is biased down which in turn biases up the FFR that pops out of the Taylor rule. Economists have ginned up many estimates of that bias, but the great labor economist Heidi Shierholz of EPI does so each month and handily posts the data. (Her estimate uses the counterfactual derived by the BLS: their participation rate consistent with full-employment.)

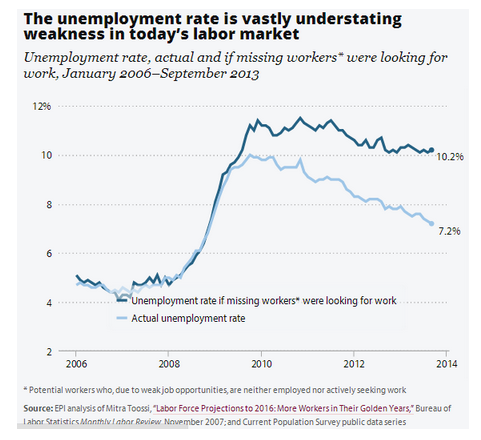

Here's Heidi's graph of actual vs. simulated unemployment, the latter being the jobless rate if all the "missing workers" were unsuccessfully seeking work. The difference between the two rates is three percentage points, or about 4.5 million jobs given today's (depressed) labor force. As Heidi herself has noted, this is an upper bound on the jobless rate since presumably some of the missing workers would find jobs were they looking and others would still be out of the job market.

Source: Heidi Shierholz, EPI.

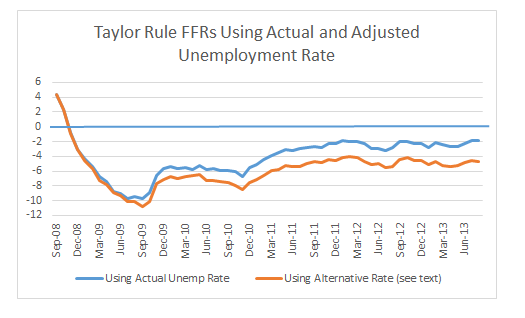

So in plugging this adjusted rate into a Taylor rule, I arbitrarily cut the difference in half, which actually gets you closer to other estimates of the current downward bias in the jobless rate, which range from 1-2 percentage points.** Plotting both Taylor-rule-generated FFRs in the figure below, you see that the actual rate returns an FFR of about -2 percent, while adjusting for the downward bias in the jobless rate return an FFR of about -4 percent.

Source: My calculations, see text.

All's I'm sayin' here is that we still have a lot of slack in the job market, highly elevated unemployment (any way you want to measure it), and a strong rationale for aggressive monetary stimulus, not to mention fiscal stimulus, but that is blocked by government dysfunction. The message here is thus: good for the politically independent Fed for keeping the monetary pedal to the metal. That's certainly the direction in which the data are pointing.

*Janet Yellen's recent "optimal control" work is also gaining prominence in this space. By simulating a path toward a goal like full employment, optimal control techniques return both a path for the FFR and inflation (other variables could easily be included but these are the key ones).

See the figures on pages 28-30 from this Yellen paper. Relative to various Taylor rules, the technique allows inflation to temporarily exceed the target rate (2 percent) as the unemployment rate falls (I should note that optimal control assumes inflation expectations remain well-anchored, an assumption that will produce agita for some price hawks).

**I used this version: 2+p+(0.5(p-2))+y where p is year-over-year percent change in the PCE inflation index and y is the output gap: 2*(5-unemp) where 2 is the Okun coefficient and 5 is my NAIRU (the first "2" in the formula is the neutral FFR, though that too may be biased up these days). I used a similar Taylor formula here, though no less than Taylor himself was not loving that earlier post

This post originally appeared at Jared Bernstein's On The Economy blog.