In an unexpectedly downbeat jobs report, employers added only 38,000 jobs last month, the worst month for job gains since employment started recovering in 2010. Downward revisions trimmed the employment gains for the prior two months by 59,000, and the labor force participation rate fell again in May, as it had in April. That drove the unemployment rate down to a recovery low of 4.7 percent, but for the wrong reason: not because of people getting jobs but because of people leaving the job market.

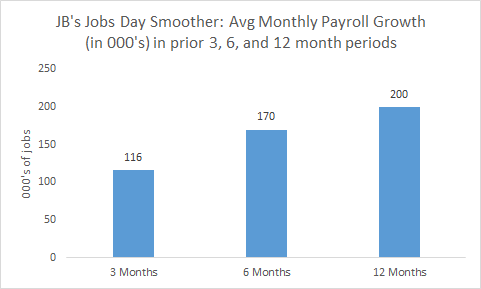

Given the volatility in these monthly reports, I have been appropriately cautious in suggesting that the U.S. job engine has truly downshifted. However, a look at JB's monthly smoother now at least tentatively supports that conclusion. Going from 12, to 6, to 3 month averages of monthly job gains shows a steady deceleration from 200,000 to 116,000.

Source: BLS, my calculations.

This new, slower trend could, of course, reverse if growth picks up and part of May's very low topline number is due to the strike at Verizon, a one-off event which, according to the Bureau, reduced the payroll count by about 35,000. But even adding those information workers back into May's tally, the three-month bar in the smoother would rise to 127,000, still well below the 200,000 trend over the last 12 months.

The negative report surely puts the nail in the coffin of a Fed rate hike at their meeting later this month. Prior to the report, the futures market probability of a June hike was about 20 percent. After the release, it quickly fell to 4 percent.

Weak job creation is weighing on the labor force participation rate, which is down 0.4 tenths of a percent over the last two months. At 62.6 percent, the LFPR is back to where it was last December. While retiring baby-boomers have been correctly cited as a structural--vs. cyclical--factor lowering participation, the recent decline has also occurred among "prime-age" workers, those 25-54. In other words, what we're seeing here is more than a benign, demographic trend; it's a trend that is also a function of weak labor demand failing to pull people into to the job market.

Most goods-producing industries shed jobs in May, including durable manufacturing, down 18,000. Over the past 12 months, this important manufacturing sub-sector has shed 80,000 jobs, a sharp reversal from the addition of 120,000 jobs in the prior 12 months. The stronger dollar, which makes our exports less price-competitive, is a major factor in this unfortunate turnaround.

Another sign of weak labor demand was the increase in involuntary part-timers -- i.e., those who would prefer full-time jobs -- by 470,000. Again, the monthly series is noisy, so we should discount the large jump, but the underemployment rate, which includes these workers, remains stuck at 9.7 percent, at least a point above where it would be in a full-employment job market.

There were some bright spots in the report. Job creation in health care continues to churn along, with employment up 46,000 last month and about 490,000 over the past year. As we've shown, this favorable trend coincided with the advent of health care reform's premium subsidies and Medicaid expansion; it's unlikely that's a coincidence. The unemployment rate for workers with at least some college attainment held at lower than average rates of about 4 percent for those with some college and 2.4 percent for those with college degrees, and their LFPRs did not fall in May.

Finally, wage growth rose a mild 0.2 percent over the month, but is up 2.5 percent over the past year. That's an acceleration over the 2 percent growth rate that prevailed last year at around this time.

The lower trend in job creation that appears to have taken hold could, as noted, reverse. Real GDP growth in the first quarter of the year was less than 1 percent, and current forecasts for the second quarter are tracking well above that. Then there's the strike, and weather issues could also be adding noise to the data.

But it would be a mistake to write off these dour numbers. Moreover, while the Fed can certainly do no harm by holding rates steady, that's not the same as helping. Fiscal policy is looking more and more like an essential, missing ingredient in labor demand, and with borrowing costs still as low as they are, a smart move by policy makers would be to quickly start up an infrastructure program, perhaps in areas of water safety or repairing our deteriorating stock of public schools.

Clearly, in the midst of both political dysfunction and a contentious election, this would be a heavy political lift. But it's still the right thing to do.

This post originally appeared at Jared Bernstein's On The Economy blog.