For our third dispatch this month (see previous posts here and here), I spoke with David McDowell, a senior organizer at the Southwest Organizing Project (SWOP) in Chicago, IL. David, who has more than 20 years of community organizing experience, works with SWOP's members to build a broad movement among churches, mosques, synagogues, schools, and other institutions in Southwest Chicago on a issues including housing and immigration.

For those of us who do not live in the neighborhoods where David and other SWOP members fight to keep people in their homes, it may be difficult to fully fathom the poisonous effect of foreclosure on entire communities. Without homeowners raising legal defenses that could halt the foreclosure, too many homes end up as abandoned, bank-owned properties. Even before a foreclosure notice arrives in the mail, fear of losing a home can drive families, such as those featured in the Fighting Foreclosure video series, to give away the last of their dwindling resources to fraudulent "rescue" companies that promise to repair credit or refinance mortgages. Community-based organizations such as SWOP not only educate homeowners about how they can respond to foreclosure and avoid these predatory schemes, but they also advance the interests of embattled communities in negotiations with banks and mortgage servicers.

How have SWOP and its members been implicated in Chicago's foreclosure crisis?

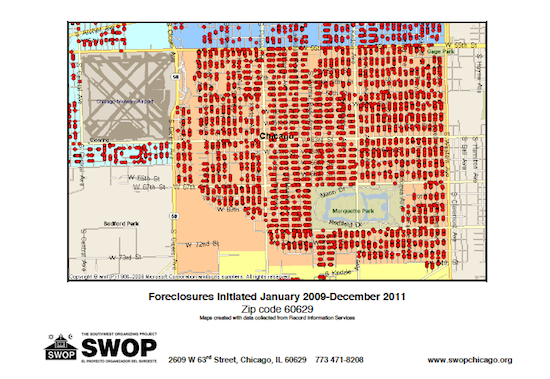

The Southwest Organizing Project (SWOP) and our resident leaders have been fighting foreclosures in our southwest Chicago neighborhood for more than a decade. Initially the fight was over predatory lending practices. Since the 2007 economic meltdown, our leaders have also been fighting to keep families who have lost jobs from losing their homes. In the period between January 2008 and December 2011, our neighborhood has seen more than 12,000 residential foreclosures initiated. With numbers this high, foreclosures cease to be merely a problem for the homeowner and their neighbor -- they become a crisis that threatens the very fabric of our community, putting our faith institutions and our schools, our businesses and our tax base at huge risk.

From where you're sitting, what, in your view, is one of the main challenges facing homeowners in foreclosure?

The greatest challenge facing homeowners in foreclosure in our neighborhood has not changed since 2007. It continues to be the banks' and servicers' failure to make meaningful permanent loan modifications, including a reduction in the mortgage principal, on the homes in our neighborhood.

We have believed from the beginning of the crisis that the banks are the one entity that could turn around the foreclosure crisis, but they have been unwilling to do what is necessary to help keep the housing market viable. Over the last three years, SWOP has been in negotiation with local and national bank officials from Bank of American, JP Morgan Chase and Citibank, all of whom have refused to reduce principle for homeowners in our area. Instead they, as well as Fannie Mae, continue to stick with an outdated paradigm -- the failed Net Present Value (NPV) model -- that they claim tells them it makes better business sense to foreclose on a home than offer a reduction in principal.

However, 94.3 percent of the properties that complete foreclosure auction in our neighborhood do not get the minimum bid, which means that the banks take them over. They become vacant buildings subject to dramatic deterioration and further devaluation, ultimately being sold at a small fraction of the value of the original mortgage as nearly empty, stripped shells. According to United States Postal Service data, more than 12 percent of the homes in our neighborhood are currently vacant and they remain vacant on average for 533 days.

What is one aspect of the foreclosure crisis that has been overlooked by the media?

The media has focused almost exclusively on what the banks did, like the robo-signing controversy, rather than exploring what the banking industry needs to do to fix the mess they caused. There has also been little conversation around the larger responsibility of banks in their role as key financial institutions in creating healthy communities. Rather, banks are portrayed as an entity whose sole responsibility is toward their short-term shareholder accountability.

What is the biggest change we need to make in addressing foreclosure going forward?

Everyone involved in the foreclosure crisis -- banks and servicers, investors holding troubled mortgages, government regulators and local and national legislative bodies -- need to see low and middle-income families in neighborhoods like ours as a critical part of the larger economic system. They need to see -- and act accordingly -- that saving the housing market by keeping families in their homes on the southwest side of Chicago is critical for the long-term prosperity of the city, the region and ultimately, the country. What matters in the long run is not what was done in the past but rather how much is left standing when it is all over.