WASHINGTON -- When banks were caught improperly signing off on foreclosure documents last fall, consumer advocates and property rights experts hoped the public outcry would force the companies to change their foreclosure processing systems to ensure that meaningful document reviews were conducted and wrongful foreclosures were prevented.

But in at least one county in North Carolina, banks have responded by exploiting a filing loophole that has allowed them to continue signing off on key documents en masse, according to a local official.

Jeff Thigpen serves as Register of Deeds for Guilford County, N.C.; his office is where local land records are filed. Each time a homeowner refinances a mortgage or sells a home, banks have to file a "Certificate of Satisfaction" with Thigpen's office. Thigpen recently reviewed 6,100 documents from Guilford County and found that 4,500 of them were signed with widely varying signatures -- evidence that multiple people were forging signatures on behalf of a key signer. Several of the signatures in question appear on foreclosure documents filed in court cases around the county. Those documents are now being scrutinized by state and federal courts.

But in November of last year, after several major banks announced brief foreclosure moratoriums over documentation problems, the trend shifted. Instead of seeing multiple signatures for the same person, Thigpen noticed that documents were pouring in with perfectly identical signatures, with no variation whatsoever. These identical signatures, he says, are likely the result of banks using electronic signatures.

While forging signatures on key documentation is against the law, electronic signatures are perfectly legal in Guilford County, where there are many different ways to file land records with the Register of Deeds. One method requires simply a "verified" electronic signature, allowing banks to stamp the same scanned signature on thousands of documents.

Thigpen says that this system never really bothered him before last year's mass forgery scandal. But after seeing the forgeries, he's no longer comfortable with the electronic system. For him, the increase in electronic signatures raises concerns that an actual person did not carefully review each document.

"It's kind of hard to figure out whether they're telling the truth or not," Thigpen told HuffPost, referring to electronic bank signatures. "[Banks] submit this stuff in a way that can comply with the state law, [but] it's just a real big question of credibility."

It would seem robo-signing has not stopped in Guilford County. Only the state legislature or the Secretary of State have the power to close the legal loophole for electronic filing that allows the practice to continue.

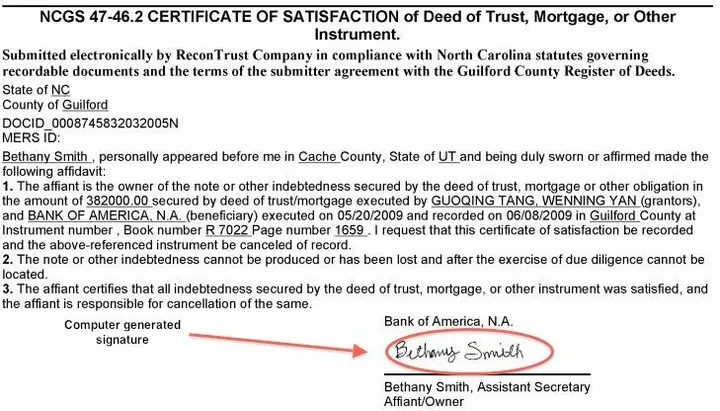

Since the forgeries were uncovered, Bank of America's filing activity has shifted more than that of any other bank. According to records compiled by Thigpen, a woman named Bethany Smith signed off on 97 land records for Bank of America in Guilford County between May 1, 2010 and October 30, 2010.

Over the next six months -- from November 1, 2010 to April 30, 2011 -- Smith approved 1187 documents filed with Thigpen's office -- more than 12 times as many documents as she signed in the six preceding months. Each document appears to have been signed electronically, Thigpen says.

"If you've got someone who has gone out and forged a bunch of signatures on checks, and then they turn around and come back and say they're just signing for themselves now, are you going to accept an electronic signature from them on thousands of checks?" he asked.

Bank of America acknowledged that it was using electronic signatures in a written statement and indicated that it makes use of them in other counties as well. But the bank denied that it was turning to electronic signatures as a result of the foreclosure documentation scandal.

"When available, e-recordings and e-signatures allow the bank to better satisfy our customers with efficient and prompt satisfaction of lien on properties," BofA spokesperson Juman Bauwens wrote HuffPost in an email. "E-recording is an acceptable practice established by the Guilford County recorder’s office. Bethany Smith is authorized to sign on behalf of the bank. The use of e-recordings pre-dates and has nothing to do with the foreclosure documentation issues."

Robo-signing challenges the integrity of the county's land records, Thigpen says, and that could have major repercussions for the local housing market. The paperwork serves as official notice that a home is now clear of previous loans and can be sold to other homeowners. But with the validity or accuracy of these documents in doubt, buyers and sellers may not be able to know for certain who owns which properties. The result could be a slowdown in the market, or chaos if existing sales begin to be challenged.

"Our entire real property system is based on a human being reviewing a document, signing a document and marching it down to the courthouse," said Matt Weidner, a foreclosure defense attorney. "At some point there's going to be an acknowledgement that the entire real estate and mortgage finance system is broken across the country."

Of the 4,500 forgeries that Thigpen's office uncovered last year, Bank of America was responsible for 15 percent, second to Wells Fargo, which accounted for 54 percent. Wells Fargo, too, has seen a bump up in electronic filings, with a woman named Sylvia Kohut signing off on 842 documents between Nov. 1, 2010 and April 30, 2011, up from 690 in the preceding six months. Wells Fargo says the increase in electronic signatures is due solely to an uptick in mortgage refinancings.