Paul Krugman is no stranger to going on teevee and encountering, well, people of an addled aspect -- he's done "Squawk Box", after all! But there was something very special about one of his most recent appearances on MSNBC. You thought that Felix Baumgartner dude who fell to earth for Red Bull was extreme? Take a seat, balloon boy. Paul Krugman has become the first human I've ever witnessed escaping from the gravitational pull of something with black hole-like density: Joe Scarborough and his gang of deficit hacks.

Krugman has this interesting thesis about the way "thinking" congeals among media elites. He thinks that they are overly obsessed with a deficit crisis that is decades from happening, if it happens at all. He observes that in this time of widespread unemployment and grievous economic dislocation -- a continuing condition of the lightly tended to 2008 economic calamity -- and against all evidence, the media elites have become convinced that the long-term budget deficit is the actual crisis that's emerged in America, to claim its future. And then you get a cycle -- blather, wince, repeat -- in which all of these cosseted simps reinforce one another until this bizarre line of thinking is deeply entrenched and inalterable.

It's an old yarn, and Krugman's far from the first person to notice. Greg Sargent calls it the "Beltway Deficit Feedback Loop," and as the National Journal reported back in May of 2011, it's been unfolding within the media and distorting its coverage -- mostly to the expense of the more serious unemployment crisis. (There is no comparable feedback loop on the unemployment crisis. Aside from occasionally speculating on how high unemployment rates could affect the electoral hopes of prominent political celebrities seeking re-election, it's almost never discussed.)

But, as with any theory, it's always great to observe the Feedback Loop in nature, and that's what Krugman's journey to MSNBC's blasé kaffeeklatsch successfully revealed -- proof of this thesis.

The best part of the exchange comes after Ed Rendell attempts to invoke the talismanic power of the Simpson-Bowles Commission, which media elites believe is somehow magical, (and more often than not evince no awareness of what the Simpson-Bowles plan called for) but is better known as one of the links in a long-running failure chain that eventually resulted in our current regime of continual, self-engineered fiscal crises.

KRUGMAN: So two guys can write a report that calls for all kinds of good stuff and they can't even get their own commission to agree on the report. And you're saying this should be our policy? We need to focus on what is urgent right now, which is creating jobs and getting this economy back to full employment.

RENDELL: But the way you do that is to build a political coalition to do something about the long-term debt.

KRUGMAN: Have you been living in the same country as I have these past five years?

SCARBOROUGH: My message is, we've got a coming collapse if we don't take care of our entitlements.

KRUGMAN: It's a long way off, it's not necessarily even true.

What follows from there is a strained comparison between the deficit and climate change, and some concern trolling over the S&P downgrade, which affected the U.S. bond market nary a whit. Eventually Richard Haass levels this strange accusation at Krugman, "You're basically willing take enormous risks with the American economy."

KRUGMAN: People like me have been saying for five years, don't worry about these deficit things for the time being, they're a non-issue. Other people have been saying, 'Imminent crisis, imminent crisis!' How many times do they have to be wrong and do people like me have to be right before people start to believe this?

HAASS: You're right until the day you're wrong, and that's a bad day.

If pure bafflegab could power manned space flight vehicles, we'd be establishing the first colony on Mars this very week. The notion that the guy urging the mitigation of the unemployment crisis is the one taking enormous risks with the economy is simply astonishing. "You're right until the day you're wrong and that's a bad day," isn't even an argument. You could say the same thing to the gravitational constant, if it were a living thing that could walk onto a teevee set and get ridiculed by pedants. I'm quite sure that Nate Silver remembers the time that the Morning Joe crew predicted he'd be on the business end of a similar comeuppance.

Haass' position, that not fixing the debt will precipitate some epic crisis, is also way overstated. It's plausible that we could see rising interest rates or inflation at some point. And that would be bad for the economy (though the Federal Reserve could treat these conditions), it's not necessarily going to set off some sort of global run on the dollar or a big financial crash. Of course, even if we did, its major adverse effect on the real world would be mass unemployment, which we're facing right now. So what Haass is actually saying is that we cannot afford to fix the massive unemployment crisis now, because it could result in some future massive unemployment crisis. That's a decidedly oddball position to take.

But the most purely risible thing that was uttered was Ed Rendell's contention that the way you solve the unemployment problem is by first "building a political coalition to do something about the long-term debt." The need to do something about the long-term debt is a matter of concern, but it's not nearly as urgent as the unemployment crisis. What's more, this is wrong way to link these two concerns -- Rendell's prescription is the equivalent of a captain of a capsizing luxury liner calling for immediate swimming lessons on the Lido Deck.

But beyond that, if the current economic emergencies can only be solved by building a political coalition around solving the long-term budget trajectory, then that is basically like saying that there will be no relief for our current economic emergency, because if there's one thing Washington has not been able to do since the financial crisis is form any sort of coalition around the debt.

We've tracked this: the efforts began with a Senate Deficit Commission (which died after its GOP co-sponsores bailed), to President Barack Obama creating the Simpson-Bowles Commission (which failed to form a coalition), to the Super Committee (which failed in similar fashion), to the current budget sequester (which would make steep cuts in spending, but not the ones the fiscal hacks want). We've been trying to form this magical political coalition for years and the efforts have only made things worse.

The problem of long-term health care costs are real. The concerns that Medicare and Medicaid need significant attention to remain robust programs are not mislaid. But making steep cuts to those earned benefit programs don't actually fix health care costs, they merely get the government off the hook for health care spending, and put the pressure on the private sector (creating a drag on growth) or individuals (creating impoverishment and death). This tactic absolutely will reduce government spending, in the same way that you can reduce spending right now by not paying your rent.

It's time to table the notion that long-term deficits are cause for immediate alarm. The fact of the matter is that interest rates are low, U.S. Treasurys are strong, there's no reason why we can't spend productively, put people back to work, solve the crisis of aggregate demand that's crippling growth, and arrest the deepening hysteresis that's threatening our fragile recovery.

Moreover, we should probably take a break from all the breathless blather about impending bond meltdowns or America turning into the next Greece. As Neil Irwin points out, these fears stem from the weird crisis mythologizing of the pundit class, against the evidence in which economists are steeped:

A persistent fear is that investors will at some point decide that the U.S. government's finances are a mess and/or inflation is at risk of getting out of control, and shun U.S. treasury bonds. This could cause a spike in interest rates and, for the Treasury, trouble rolling over the debt. The thing is, there is not even a shadow of a hint of this risk priced into financial markets. Treasury borrowing costs are extraordinarily low, as are market expectations of inflation. In traditional economic models, inflation can only really take hold if and when the economy is getting back close to its full economic capacity -- and if that happens, it would also mean a rapidly falling budget deficit.

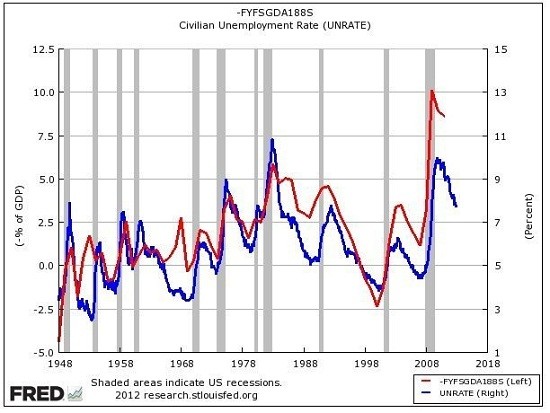

That last point is key, because the good news is that solving the unemployment crisis first is the proper way of arranging the cart and the horse. Over at Business Insider, Joe Wiesenthal presents the case for fixing the debt by first solving the unemployment crisis pretty effectively, noting that the "primary driver of deficits is a lack of growth" and getting people back to work would provide that growth, new revenues, and deficit reduction. And he points out that there is an observable 60-year trend in which deficits rise and fall according to the civilian employment rate:

Wiesenthal's meticulous argument deserves to be read in full, so go do that. I'll simply note here that he goes on to lay out how 'over the last few years, the deficit as a percent of GDP has been falling at its fastest pace since WWII, all thanks to people re-entering the workforce, and the pain of the economy being reduced," which means we're accomplishing something to shore up the deficit right now, and doing so without the European-style "belt-tightening" which is driving nations like the United Kingdom into deeper and deeper economic misery. He also has great advice to anyone who wants to take up this argument and drive it home like a boss:

In the debate over fiscal policy, you frequently hear liberals argue: "It's not time to deal with the deficit, we need to fix the economy first and then fix the deficit when the economy is stronger." While this has merit as a political concept, it's actually giving into a false frame that dealing with the deficit and dealing with unemployment are two separate things that you do at different times. Steps you take to improve unemployment are deficit reduction measures ... While the government has done, technically, nothing to address the deficit in the last few years, the deficit is shrinking (relative to GDP) merely because the economy has improved, and more people are going back to work. If unemployment drops to 7 percent, or 6.5 percent, or 6 percent, we'll get quite a bit of deficit reduction then.

None of this is some sort of otherworldly, out-of-the-mainstream thinking, and it dovetails pretty neatly with what Krugman has been arguing for years. But the deadweight Washington consensus on junk economics is powerful. Scarborough, after subjecting Krugman to a thorough helping of debt hack tautologies on his show, went back for a second helping in a slapdash Politico column (another feature of deficit hackery is the constant need to repeat the same arguments, as if they aren't getting a sufficient hearing), in which he reiterates that all the evidence he needs to support the claim is just the fact that he talks to a lot of people who agree with him, and that, in addition, he's been making the same claims over and over again, so -- ipso facto -- they must be true.

It's not clear that Scarborough is paying close attention to what Krugman was actually saying on his show, because right up at the top of his piece, he hilariously misrepresents Krugman's basic position, claiming that that Krugman believes "Americans would be better off if its government ran deeper deficits and ignored its longterm debt." Actually, Krugman said, right to Scarborough's face, "Give me something that looks like a normal employment situation and I'll become a deficit hawk."

There is further nonsense about Krugman taking a firm stand on ignoring "Medicare and Medicaid shortfalls," but he similarly said no such thing: "Yeah, there is [a long structural problem with Medicare and Medicaid]," Krugman says, "but you've got to ask, why is it urgent that we address that problem right now." He then went on to suggest that in the short-term, there are many ways to reduce health care costs so that the future isn't so bleak. None of this is "ignoring," it's simply about setting priorities, and -- once again -- favoring the amelioration of the unemployment crisis right away. (Scarborough himself framed the "structural Medicare" problem as something that was 20 years out, so why Krugman is suddenly not allowed to play by the same rules in his response is just an example of Beltway pundit Calvinball.)

But the most ignorant claim Scarborough makes is the one embedded in his headline, "Paul Krugman vs. the world," which advances the thesis that Krugman is all on his lonesome, with an off-planet explanation of how the economy works.

It's simply not true! For example, here's the decidedly non-obscure Alan Blinder, making the same argument, perhaps even more pointedly than Krugman. To his estimation, the proper way to solve the deficit problem is to tackle it in "three parts ... one for right now, one for the next decade, and the last for the very long run:"

RIGHT NOW: With the economy still so weak, the case for near-term fiscal contraction is weak as well. We shouldn't kick away the fiscal crutch until the patient is ready to walk. If I am allowed to indulge in wishful thinking, a two-pronged policy that combines modest fiscal stimulus up front with serious deficit reduction thereafter would be even better.

THE NEXT DECADE: Strange as it may seem with trillion-dollar-plus deficits for four years running, the U.S. government still has no short-run borrowing problem. On the contrary, investors all over the world are still clambering to lend us money at negative real interest rates. In purchasing power terms, they are willing -- nay, eager -- to pay our government to borrow from them!

According to Congressional Budget Office January 2012 projections, the federal deficit as a share of GDP will shrink from 9 percent of GDP in fiscal 2011 to roughly 5 percent of GDP in fiscal years 2015-2018, without any further policy actions. To be sure, 5 percent of GDP is still too high. But coming from the stunning 10 percent of GDP in 2009, it's a long way down. A reasonable target for deficit reduction over the next decade might be 2 percent to 3 percent of GDP, starting perhaps in fiscal 2014.

THE VERY LONG RUN: The truly horrendous budget problems come in the 2020s, 2030s, and beyond. But while the long-run budget problem is vastly larger, it is also far simpler, for two reasons. The first is that the projected deficits are so huge that filling most of the hole with higher revenue is simply out of the question. Spending cuts must bear most of the burden. The second is that there is only one overwhelmingly important factor pushing federal spending up and up and up: rising health care costs.

That's just one of the many people who echo the same remedy as Krugman. In a separate post, the aforementioned Wiesenthal collects a roster of similar-minded people, who range from liberal to conservative and economist to policymaker. That's important to note: this is not an issue of right-versus-left ideological conflicts. This is a right-versus-wrong conflict, pure and simple. It's a Beltway bubble versus real-world conflict. It's a data-tested versus magical-thinking conflict.

The good news is that the American people haven't bought into the nonsense, and in poll after poll favor solving the more pressing unemployment crisis over fixing the long-term budget trajectory. And even those who want action taken on the deficit do not favor major cuts to earned benefit programs like Social Security or Medicare. (Social Security, which can be provided with greater solvency simply by loosening or discarding the current income caps on contributions, needn't even be part of the larger long-term deficit discussion.)

These are understandable positions for anyone who actually knows an unemployed person, or who lives through the grind of our demand crisis on a daily basis, but media elites don't know or desire "access" to unemployed people and can't appreciate the day-to-day problems that millions of Americans face in getting their households through another week of survival. According to a new report from the Corporation for Enterprise Development, "almost half (43.9%) of U.S. households are living on the edge of financial collapse with almost no savings to fall back on in the event of a job loss, health crisis or other income-depleting emergency." This is not a populace that can currently power economic growth on its own, and until its members get help, deficits will persist. Further cuts in the short-term that extract further wealth from the economy will only deepen the risks that millions of Americans face.

It's popular to say things like, "Well, if we don't figure out how to right-size the budget, what are we going to do in 20 years when the next Hurricane Sandy hits?" Well, remember, we're still dealing with the first Hurricane Sandy, and our faltering efforts to bring relief to those affected has been hopelessly scrambled by the inane Beltway Deficit Feedback Loop. We just came very close -- too close! -- to simply not providing any Hurricane relief at all. At the very least, what would normally be an easy call became much more complicated as we debated whether we could authorize relief money.

I guess the thinking was, "Hey, it's too bad you are freezing to death in the Rockaways right now, but maybe you can comfort yourselves in the knowledge that the FY 2025 budget trajectory will be incrementally better!" That's the actual weirdo thinking in this debate. It's destructive and embarrassing, and the favor bestowed on the goofy little clique that espouses it, forsaking all logic, is a continual bafflement.

[Would you like to follow me on Twitter? Because why not?]

Before You Go