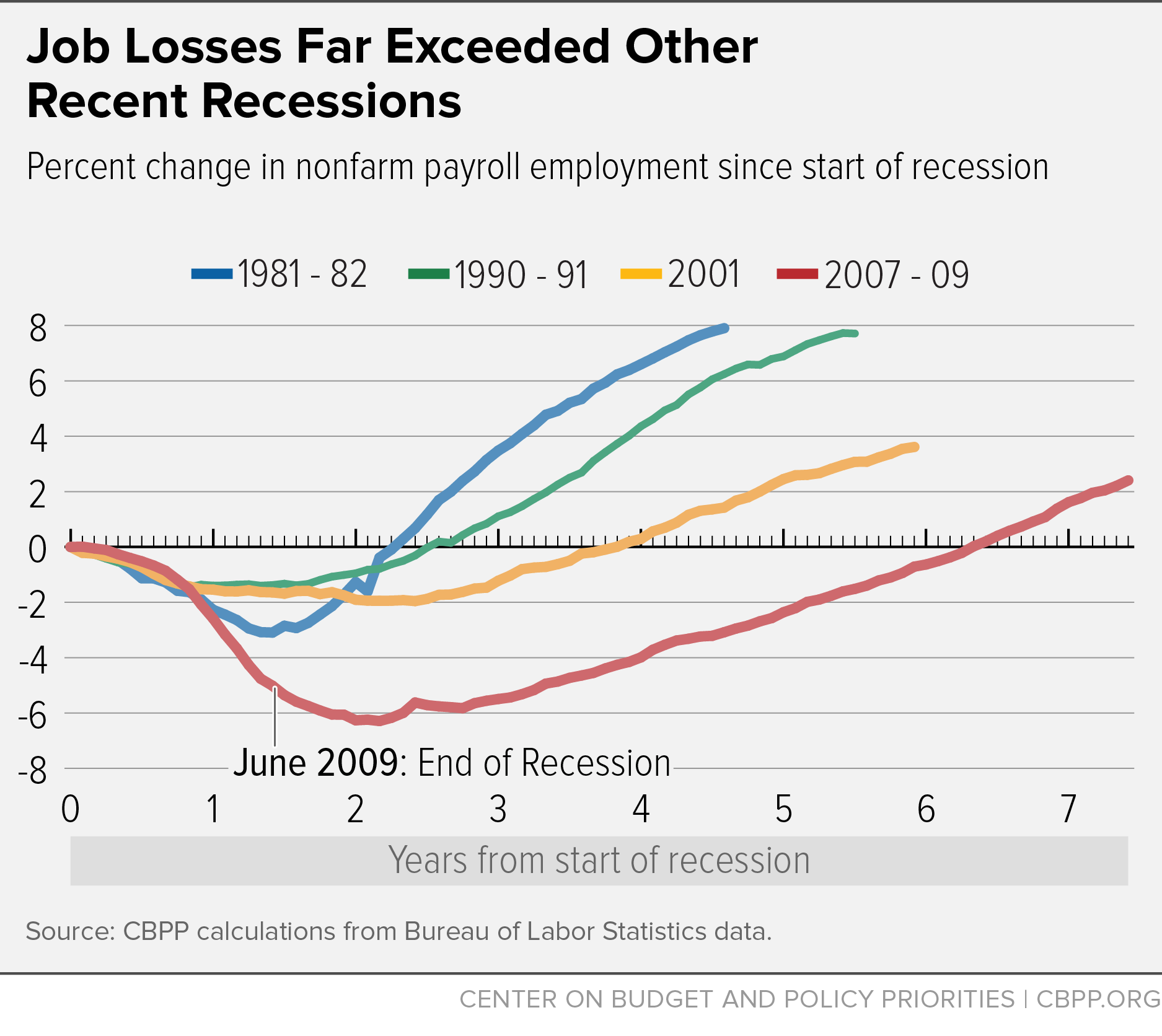

Today's strong jobs report shows continued solid growth in payroll employment (see chart), and many other labor market indicators have recovered substantially since the Great Recession. Nevertheless, the Federal Reserve should not rush to raise interest rates. By testing whether it can push unemployment lower -- rather than play it safe to avoid any risk of inflation -- the Fed could bring more workers back into the labor force, help more long-term unemployed find work, and begin to generate solid wage gains for most workers.

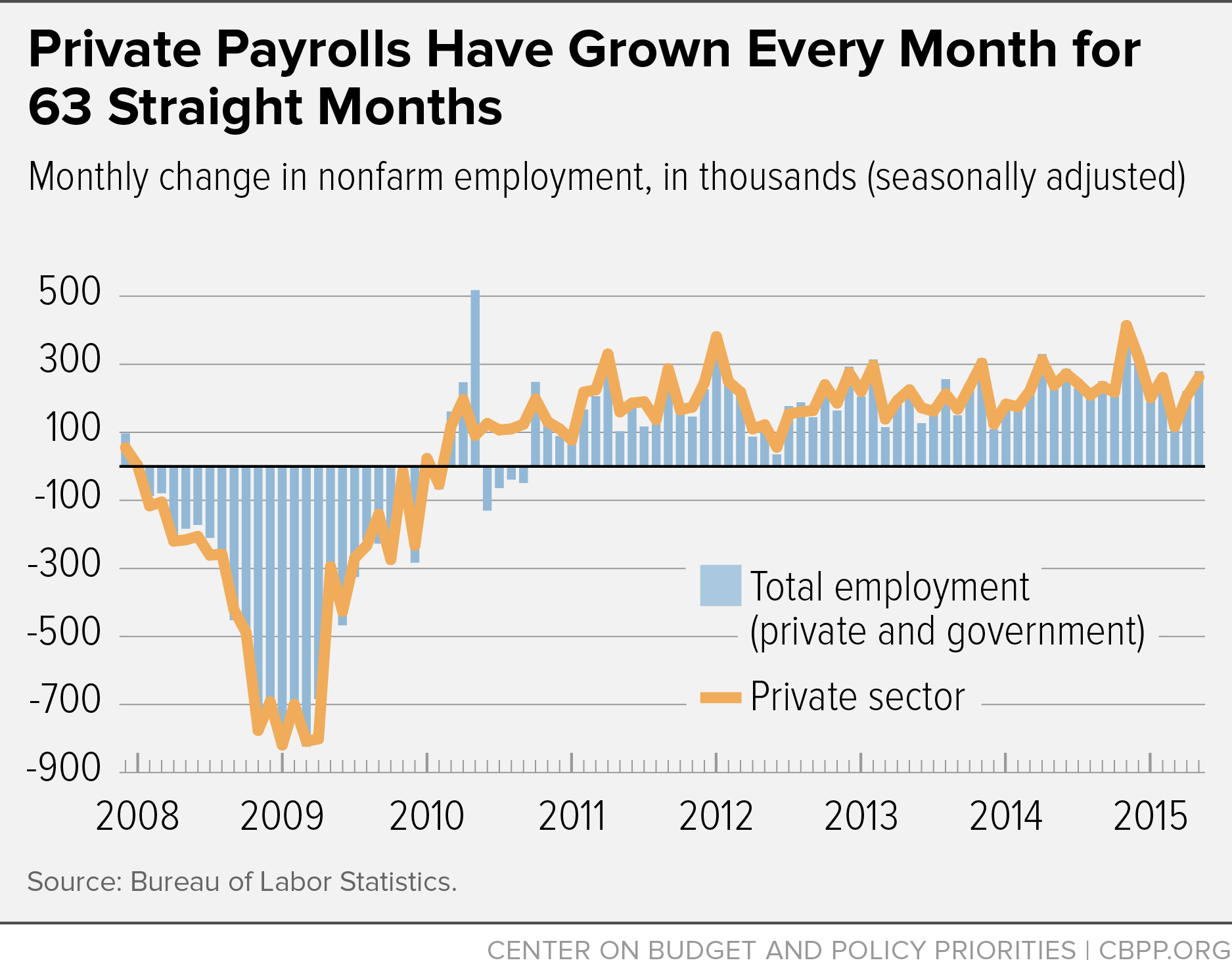

Payroll job growth has been among the best-performing labor market indicators during the recovery. Private-sector firms began expanding their payrolls in March 2010, and private payroll employment has grown every month since. Overall (private plus government) payroll job growth was distorted by the hiring and subsequent letting go of temporary workers for the 2010 Census, but total payrolls have expanded every month starting in October 2010. The dark cloud in this picture is government employment, which is still nearly half a million jobs lower than at the December 2007 start of the recession, dominated by a net loss of 361,000 local government jobs.

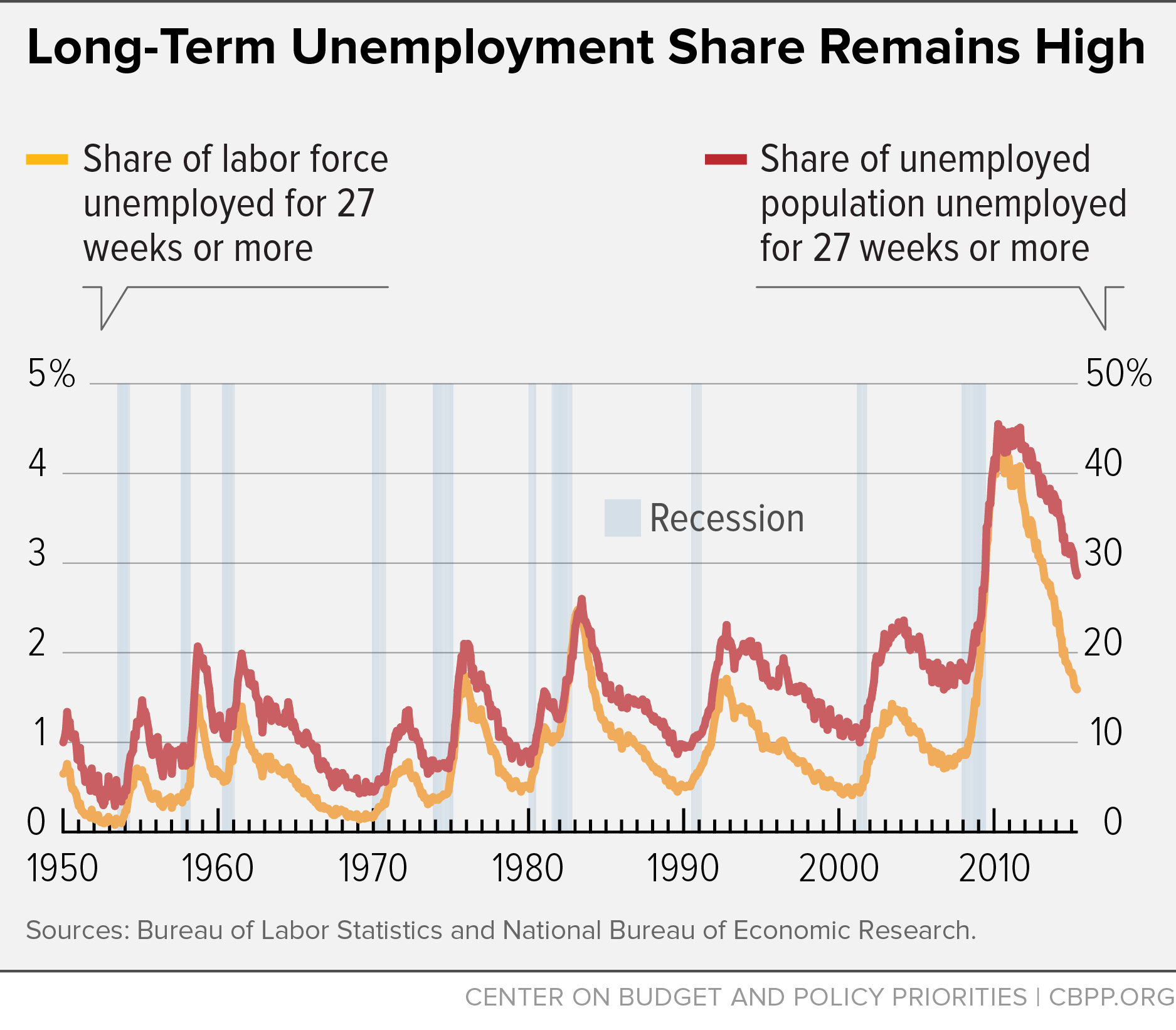

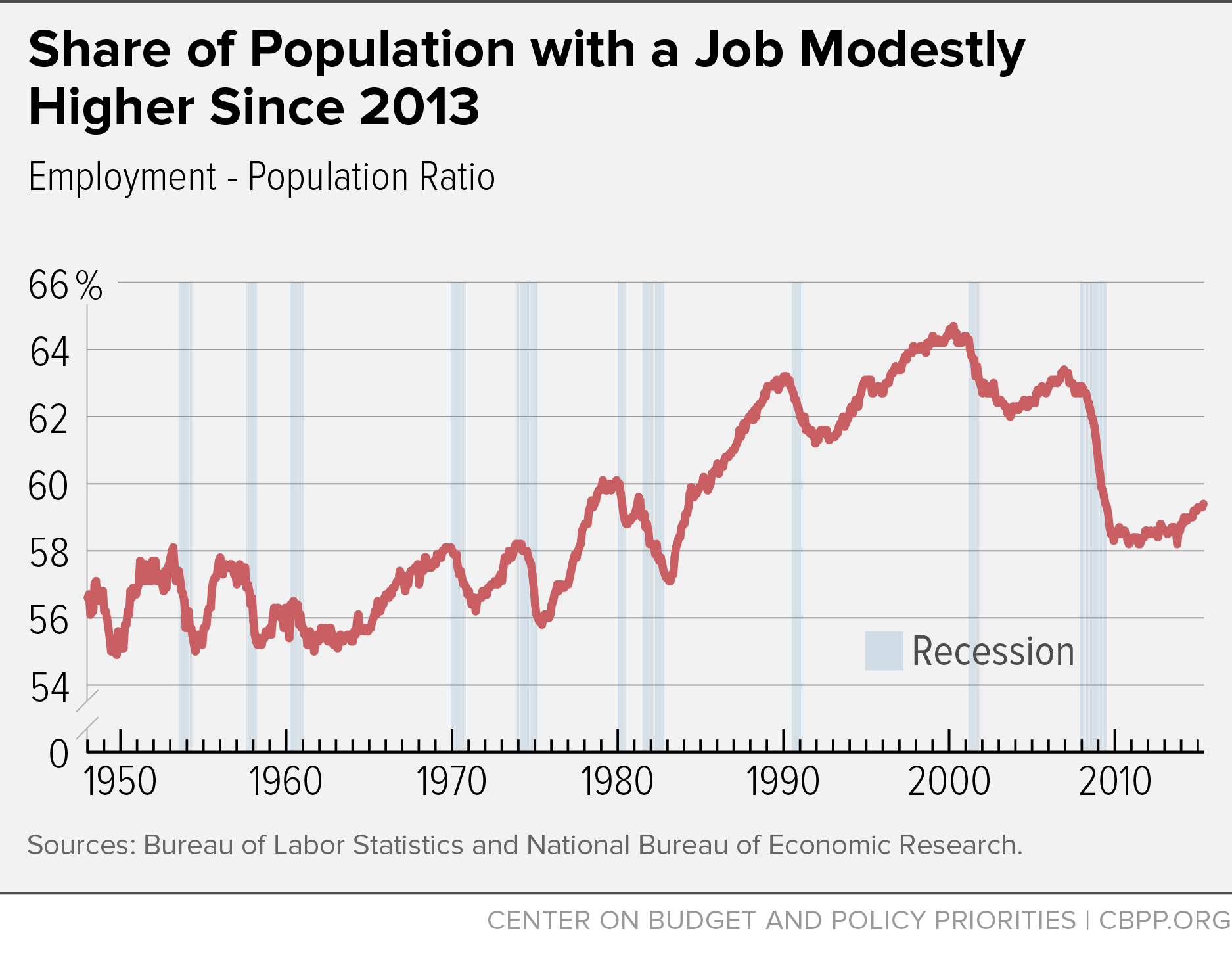

To be sure, unemployment has fallen substantially -- from 10 percent in October 2009 to 5.5 percent in May -- though it took much too long to get there. Moreover, many people dropped out of the labor force along the way or never entered it due to poor job prospects, and a historically high share of the unemployed have been looking for work for at least half a year. We need overall unemployment to fall further in order to bring more people back into the labor force and reduce long-term unemployment.

Meanwhile, wage gains during the recovery have been modest while profits have soared. We need tighter labor markets with more plentiful job opportunities and hence more competition for workers to redress that imbalance.

Throughout the long labor market recovery, inflation has remained low, and the Fed has taken a number of steps to keep interest rates low and enable the labor market to improve. Inflation is still low, and there's still room for further labor market improvements -- if the Fed remains cautious about raising interest rates.

About the May Jobs Report

Employers reported strong payroll job growth in May. In the separate household survey, the unemployment rate edged up to 5.5 percent, but this was due to strong growth in labor force participation, not weaker demand for labor.

- Private and government payrolls combined rose by 280,000 jobs in May, and job growth in the previous two months was revised up by 32,000. Private employers added 262,000 jobs in May, while overall government employment rose by 18,000. Federal government employment rose by 3,000, state government was unchanged, and local government rose by 15,000, two thirds of that in education.

The original statement can be viewed here.