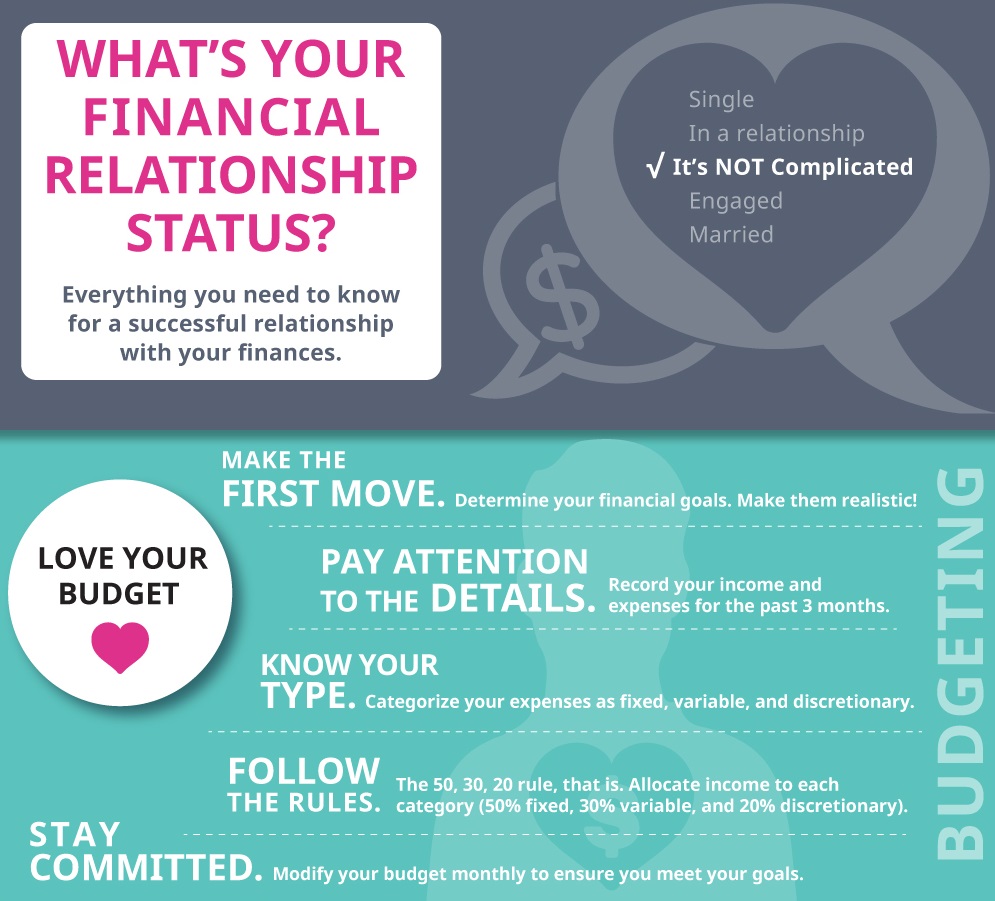

One of the most important steps in taking control of your finances is designing a personal budget -- whatever your age or financial know-how. When you take a close look at your income and expenses, you can easily determine whether you're living within your means. Once you've tailored a plan to your life, you'll be able to both spend your money wisely and build up your savings.

Examine Your Spending

The first step in creating your budget is to take a look at your income and expenses. It helps to create a spreadsheet or use our budget worksheet to track these figures and use for future reference.

First, record the monthly expenses that you always have to pay: your rent or mortgage, your utility bills, your phone bills, and so on. These "fixed expenses" are generally regular costs that you want to cover before anything else.

If you have credit card debt or student loans, you'll then want to factor in the amount you're paying off every month. This is a good chance to catch up if you're behind, as you can align how much you're able to pay with how much you want to pay.

Next, figure out how much you spend on "flexible expenses," like groceries and transportation. Even though you can't know for sure how much you'll spend on these categories, you should be able to come up with a general figure by looking at your recent spending. Remember, it's a good idea to round these figures up; that way, you're less likely to come up short -- even if you spend more than usual.

Finally, remember that a responsible budget doesn't mean you can't spend money on yourself. Think about how much you normally spend on "discretionary expenses" like clothing, movie tickets, and eating out -- and allocate some of your income to them. By working these costs into your spending plan, you won't have to worry (or feel guilty) about buying a new sweater or having a night out.

Factor in Your Income

Once you've come up with your total monthly expenses, you'll need to determine your monthly income. If you receive a fixed paycheck, regular installments of financial aid, or regular contributions from family members, you'll be able to simply use these figures.

However, some people will have to use an approximate figure, like those who work freelance or part-time jobs. Those working in the service industry, who probably rely on tips for a portion of their income, will have to do the same. In all of these situations, it's better to round down -- an inflated number that represents a "good" month won't help you create a budget that works year-round. You might also want to reevaluate your budget as the amount changes.

Give Yourself a Goal

Subtract your total expenses from your monthly income. If you have money left over, you can put it toward one of your expense categories or put it in a savings account. If you have no money left over -- or spend more than you earn -- it's time to reevaluate. You'll need to either earn more money or cut some expenses.

If you have enough money to save, it's a good idea to have a goal in mind -- for instance, a big purchase like a car. A good general goal is to put 6 months' worth of living expenses in the bank. That way, should you ever find yourself out of work, you'll have enough money to maintain your lifestyle for half a year as you look for a new job.

And once you've reached your savings goal, additional savings can go toward something a bit more indulgent. That's when you can upgrade your laptop or take that trip to Thailand you've always dreamed of. Check out our cash flow lesson to see how you can reach your goal as soon as possible.

Make It Work

Remember, because your budget was based on informed estimations of your expenses, you will need to work out some wrinkles when you put it into practice. This is especially true if your financial situation is about to change -- you get a new job, get married or divorced, or are expecting a child, for example.

Part of developing a working budget means revising the system as you go along. So you'll want to keep track of what you're spending and make sure you're not straying from the amounts you set out for yourself. If you are, you'll have to either change the budget or change your habits.

Just having a budget may not help you control your financial life -- you have to put in the effort to stick to it and make changes to your lifestyle that you feel are necessary. But as a systematic way of evaluating your income and spending, your budget can make it much easier to be aware of your money and use it effectively to reach your financial goals.

What's your financial relationship status? It doesn't have to be complicated! Use this infographic for tips on managing your personal finance.

SALT® is a free and unbiased nonprofit-backed financial education program dedicated to giving students, alumni and families the money knowledge they need for college and beyond.