Robert Shiller, the co-creator of the S&P Case-Shiller Index, which tracks national housing prices, is a man that has earned a great deal of respect for his knowledge of the real estate market. Yet he is still guilty of saying the silliest of things.

For instance, the other day he said, "There could be another bubble...people have gotten very speculative in their attitudes toward housing."

To be fair, Shiller qualified his statement by saying he doesn't think another housing bubble is likely, or will happen soon. Nevertheless, that isn't how bubbles work.

The old saying on Wall Street goes "no one rings the bell at the bottom of a bear market." The idea is that a down market finally ends only when everyone has given up on that market. This is especially true in the aftermath of a bursting bubble. If people are still "speculative in housing" then we aren't anywhere close to a bottom.

Karl Case, the other co-creator of the Case-Shiller Home Price Index, was calling a bottom in housing last summer, right around the same time that the homebuilders were calling a bottom.

In fact, Treasury Secretary Paulson was calling a bottom in housing more than two years ago.

If you want an accurate prediction of when the housing market will bottom: it will be when people have stopped calling a bottom in housing.

Recent Bubble Experiences

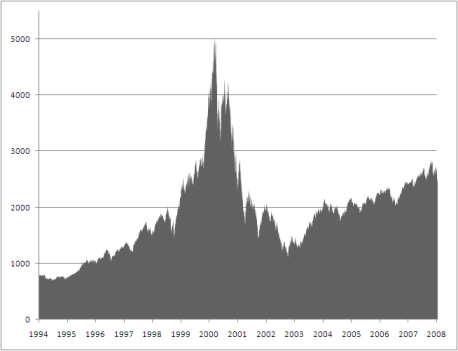

If you want a quick and dirty comparison, look at the recent Dot-Com Bubble. Remember when the Nasdaq peaked at 5048 on March 10, 2000? By late 2002 the Nasdaq had lost 80% of its value and had bottomed at 1114. Do you remember anyone calling a bottom in the Nasdaq on that day? Do you remember anyone rushing out to buy tech stocks in the months following it? Speculators had lost so much of their investment that they no longer even cared about tech stocks.

Even when the DOW and S&P 500 pushed to new all-time highs five years later the Nasdaq never reached even 60% of its 2000 highs.

"Once stocks fell, real estate became the primary outlet for the speculative frenzy that the stock market had unleashed. Where else could plungers apply their newly acquired trading talents? The materialistic display of the big house also has become a salve to bruised egos of disappointed stock investors. These days, the only thing that comes close to real estate as a national obsession is poker."

- Robert Shiller, 2005

Some will point out that real estate isn't like tech stocks, and they do have a small point - bubbles in real estate are always much larger, and deflate much more slowly, than bubbles in stock markets. Nevertheless, a bubble is a bubble, and the rules of a bubble are the same everywhere in the world.

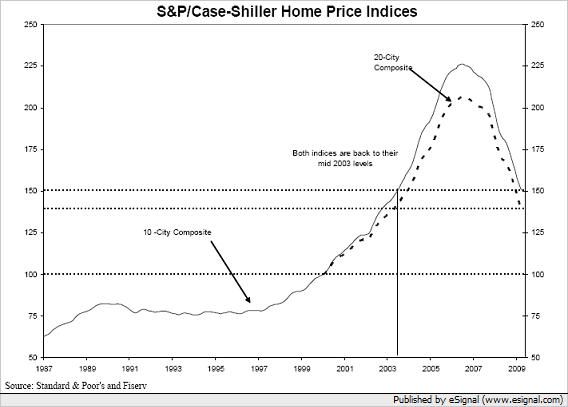

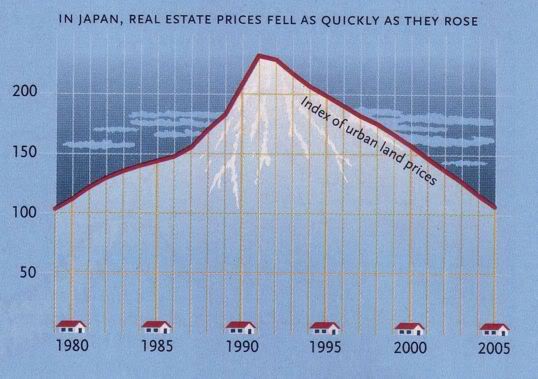

For example, look at Japan's real estate bubble experience. Notice how the comparative price levels of Japanese real estate almost mirror the Case-Shiller Index in our recent housing bubble. In the bubble areas of Japan housing prices dropped to 10% of their peak bubble levels.

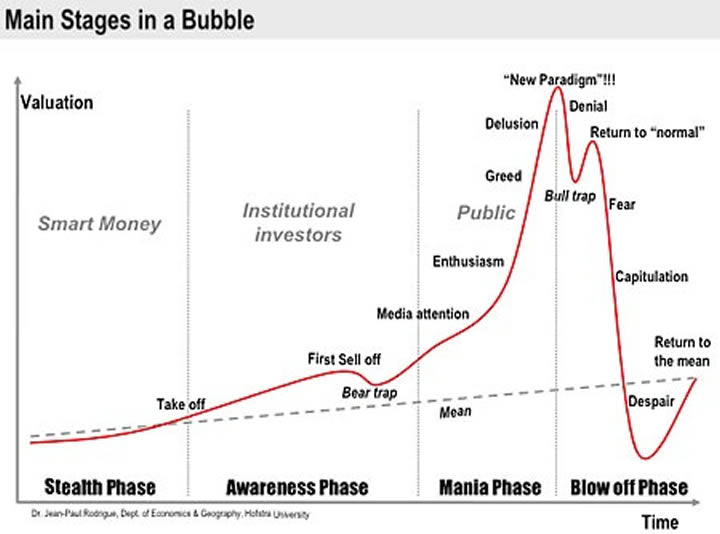

All throughout history there have been speculative bubbles, and they all have the same basic characteristics. The price charts may vary somewhat, but the overall pattern remains the same. In the end the price of the bubble asset returns to its historic norm.

For instance, notice how this chart looks suspiciously like the Nasdaq chart.

Some of you might be thinking that this chart was created just to copy the Nasdaq experience. That assumption would be wrong. Bubbles all look the same and are driven by the same emotions of fear and greed. It doesn't matter what the bubble involves. It could be stocks, government debt, or tulip bulbs.

Historic Bubbles

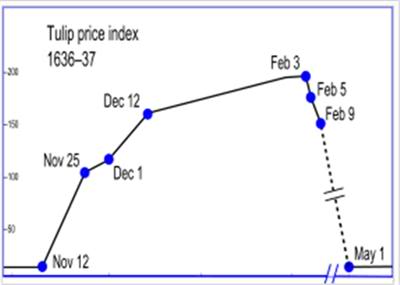

The Dutch Tulip Mania is probably the most colorful of bubbles, although the hardest to document.

The height of the bubble was reached in the winter of 1636-37. Tulip traders were making (and losing) fortunes regularly. A good trader could earn up to 60,000 florins in a month- approximately $61,710 adjusted to current U.S. dollars. With profits like those to be had, nothing local governments could do stopped the frenzy of trading. Then one day in Haarlem a buyer failed to show up and pay for his bulb purchase. The ensuing panic spread across Holland, and within days tulip bulbs were worth only a hundredth of their former prices. The tulip bubble had burst.

The Tulip Mania is only worth noting because it shows that any asset can be bid up to ridiculous levels. It may seem funny now, but is it really any more stupid than $100 Dot-Com stock without a business plan? Or $600,000 McMansions in the middle of the desert that were bought sight unseen?

The bubbles that are more worthy of examining, and are more applicable to today, are a pair of bubbles that occurred in 1720. These bubbles hold visions not just of today, but possibly of our future.

"Reckless, and unbalanced, but most fascinating"

John Law was the son of a Scottish banker. He went to school in London and became an economist, but not before losing most of his the inheritance from his father's death in gambling. It was to be a reoccurring theme of his life.

In the summer of 1694 he fought a duel over the affections of a young lady and killed the man. He was tried and convicted for murder and sentenced to death. But on appeal he managed to flee to Amsterdam.

Law's financial speculations eventually led him to Paris in 1714. France at the time was financially exhausted and nearly bankrupt from Louis XIV's wars of empire. So much gold and silver had spent on his wars that there was a shortage of currency that was crushing the economy. The atmosphere was ripe for a con-man with new economic theories.

Law had become friends with the Duke of Orleans, and the Duke became Regent when the King died in 1715.

In 1716 Law convinced the French government to let him open a bank, the Bank Generale, that could issue paper money, or bank notes. The paper notes would be supported by the bank's assets of gold and silver and would circulate as a medium of exchange. Paper money was a new concept for the French; money to them was silver and gold. Law believed that paper notes would increase the money in circulation, which, in turn, would increase commerce. These conditions would help revitalize and rehabilitate the finances of the French government.

Law believed that money was only a means of exchange that did not constitute wealth in itself, and that national wealth depended on trade. Law's idea was to replace gold with paper credit, then increase the supply of credit, then reduce the national debt by replacing it with shares in economic ventures. It's a concept that isn't very far from current economic thinking, and thus should be taken as a warning.

At this point Law hadn't gone too far from established economic doctrine. So far his plans met with minor success (interest rates had fallen to 4.5%), and this encouraged both him and the French government. But Law had his eyes on the Louisiana colony. Not much was known about the area in 1717, but there were rumors of gold and silver mines.

In August 1717, he organized the Compagnie d'Occident (Company of the West) to which the French government gave the control of trade between France and its Louisiana and Canadian colonies. In Canada, the French would trade in beaver skins. In the Louisiana colony they would trade in precious metals.

What wasn't noticed was that just a few months earlier Law had managed to get a government decree that Law's notes could be accepted in payment of taxes. This was to be a very important step. The following year Law purchased the tobacco monopoly in this region, as well as in Africa.

Things were going so well that the French government couldn't keep their hands off of Law's legal monopolies.

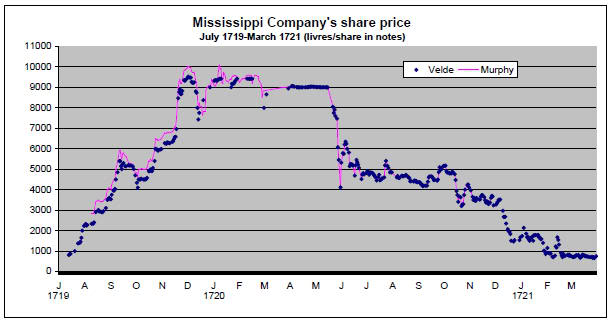

Law's Bank Generale was taken over by the French government in January 1719 and was renamed the Bank Royale. Law remained in charge, however, and the crown further guaranteed the bank's note issue. In May he obtained control of the companies trading with China and the East Indies. He renamed his entire business interest the Compagnie des Indes, but most people still called it the Mississippi Company. In effect, Law now controlled all trade with France and the rest of the world outside of Europe.

By this time, Law's reputation was truly in the ascendant. When he undertook to repay the national debt, in return for control of national revenues, and of the French mint, for a period of nine years, the share price of the Companie rose dramatically in a frenzy of speculation. People lined up in front of the Compagnie headquarters in Paris to speculate. Huge profits were being made. Europe had never seen anything like it before (except for maybe the Dutch Tulip Mania). The financial district in Paris became so agitated at times with investors that soldiers would be sent in at night to maintain order. The term "millionaire" was being used for the first time.

French investors, 1720

Law exaggerated the wealth of Louisiana. Shares rose from 500 livres in 1719 to as much as 15,000 livres in the first half of 1720. But then in January 1720 some investors began selling shares to get gold and silver bullion. Despite Law's notes being legal tender and supposedly backed by gold, the gold simply wasn't there to back even a small percentage of Law's paper. Law restricted the amount of gold he would exchange for his notes.

This attempt to turn stock shares into money resulted in a sudden doubling of the money supply in France. It is not surprising then that inflation started to take off. Inflation reached a monthly rate of 23 percent in January 1720.

Law began devaluing his stock shares, and those who bought their shares on credit, rather than with assets, had their shares confiscated. There was a scramble to sell the falling notes and exchange them for gold and silver. Law had the ownership of gold and silver outlawed in France, but this only made things worse. There was panic selling and Law's company saw a 97 per cent decline in market capitalization by 1721.

Law was dismissed by the French King late in 1720 and had to flee the country. Law died broke in Venice in 1729.

"A company for carrying on an undertaking of great advantage."

Meanwhile, on the other side of the English Channel, the idea of swapping sovereign debt for equity was also being attempted, with a similar outcome.

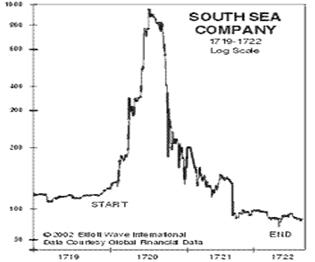

The South Sea Company wasn't nearly as am ambitious as Law's Mississippi Company, but it had the same premise. The government convinced the holders of 10 million pounds of short-term debt, to swap it for shares of a new company that was to be given a monopoly on trade with South America - mostly slave trade. In exchange, the government would subsidize the company, and would recoup the money from tariffs on the trade.

There was only one problem with this plan - Spain didn't allow more than a token amount of English trade with South America.

"I can calculate the movement of the stars, but not the madness of men." - Isaac Newton, after losing money on the South Sea Company

It didn't take long before shares were being "sold" to politicians, who "sold" them back to the company for handsome profits. This ensured political backing of the venture, and the list of high-profile investors helped bring about a speculative frenzy. On top of that, the Company had come up with the brilliant idea of loaning people money so that they could buy shares. Of course once the share price began to fall people needed to sell the shares to pay back the debt.

The bursting of the bubble in Paris forced some investors from the Continent to sell their shares in the South Sea Company. This popped the bubble in London. Many who had bought South Sea shares on credit were wiped out. Even Isaac Newton claims to have lost 20,000 pounds. A government investigation afterward revealed a great deal of corruption in both the government and the company. Many were jailed.