New York Lieutenant Governor Richard Ravitch made a statement last week that should have gotten headlines, but didn't.

"I believe that the states across the United States will face deficits a year after stimulus ends of $300 billion to $500 billion a year," Ravitch told about 200 people gathered at New York University's Robert F. Wagner Graduate School of Public Service. "You're going to begin to see cracks in the municipal bond market well before then, because that's an inexorable casualty of unfundable state deficits."

To put this into perspective, the total state budgets for 2010 was about $1.4 Trillion. If his predictions are anywhere close to being true then the budget problems of the states are essentially unfixable.

"These are numbers that are unprecedented," Ravitch said, adding that the current recession is unlike any in the nation's history, with unemployment continuing to rise, "banks are falling like autumn leaves, and nobody is projecting any significant growth in 2010."

The condition of state and local budgets are in their worst shape since the Great Depression, and if the economy doesn't turn around quicker than the mainstream believes, we are going to see defaults that will shake the economy to its foundation. The states are suffering "unbelievable" revenue shortages that are blowing out all previous budget estimates.

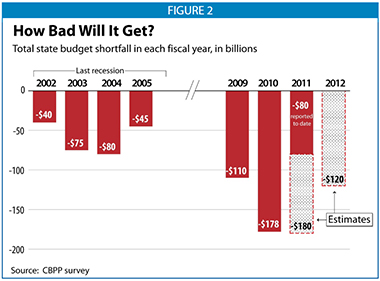

Only four months into the 2010 fiscal year, 26 states already have deficit problems totaling $16 Billion. This is after the states had to close $178 Billion of budget gaps this past summer. Only 22 states had budgets deficits of less than 20% of their total budgets. At least 9 states are projecting deficits for 2011 of at least 20%, and those are often optimistic projections.

All the easy cuts have been made. Any new cuts will mean sawing into bone.

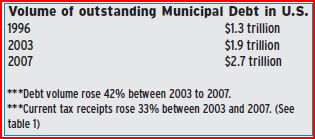

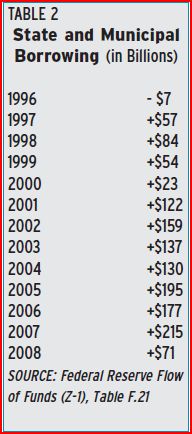

The states have mostly closed the budget gaps through borrowing, and for now the market has responded well with strong demand. However, lately the sheer volume of supply in the three trillion dollar market is starting to drive up yields.

State and local government bonds have dropped almost 2 percent since Sept. 30, based on Merrill Lynch & Co.'s Municipal Master Index, which lost a record 5.1 percent in September 2008. At least four states -- Washington, Hawaii, Maryland and Minnesota -- have postponed or scaled back refinancing plans this month as benchmark borrowing costs rose the most since January as measured by the weekly Bond Buyer 20 index.

It used to be that the state and local governments didn't have to worry too much about yields. Just a few years ago they sold through the monolines. These insurance companies would back the municipal bonds with their AAA ratings for a small fee. The monolines got their cut. The local governments sold their debt at low interest rates. Everyone was happy.

So what happened? The monolines got greedy. They weren't satisfied with their steady profits from the current business model. They wanted a piece of the sub-prime action. They started backing sub-prime mortgage-backed securities. When the mortgages blew up, the monolines were forced to pay out larger and larger amounts on those losses. Eventually the monolines lost their AAA ratings, and now they no longer have a sustainable business model.

Since the insured municipal bond model has blown up the muni bond market has gotten much more volatile. In February the muni auction-rate bond market completely collapsed. This happened less than a month after monoline insurer Ambac was downgraded, along with all the bonds it insured.

From 1984 through 2006, only 13 auctions failed, typically because of changes in the credit of the borrower, according to Moody's Investors Service. There were 31 failures in the second half of 2007, and 32 during a two-week period beginning in January. That compares with more than 480 failures yesterday alone, according to figures compiled by Deutsche Bank AG, Wilmington Trust Corp. and Bank of New York Mellon Corp.

Economist and author Frederick J. Sheehan recently wrote an article about the municipal bond market, and he didn't mince words.

The municipal market will probably repeat the pattern of the sub-prime collapse.

...

Some reasons for municipal collapse:First, losses on investments will require much higher pension contributions. Estimates vary but some states and towns will need to increase their contribution by 50% or even 100% start ing in 2010 or 2011.

Second, spending has exploded. In New York City, the average compensation for full-time worker rose from $65,401 in 2000 to $106,743 - a 63% increase...

Third, accounting gimmicks are near an end. To meet booming expenses, many municipalities have engaged in questionable practices, such as selling property to meet current expenses...

Fourth, disclosure to municipal bondholders has been poor. Financial disclosure for municipal financing is not well enforced...

Even during the relatively good bubble years of pre-2007 the states and local governments spent more than they took in with taxes.

Most people assume that muni bonds are safe from default. That's not true. Between 1970 and 2000 there were only 18 defaults on rated muni bonds. For instance, Cleveland in 1978 and New York a few years earlier. However, there were over 1,300 defaults on un-rated muni bonds during the same period.

Since the Great Depression is the comparison here, let's look at an example.

In 1933, the Iowa Supreme Court ruled the City of Dubuque was

required to meet its bond commitments. Kevin A. Kordana, a University of Virginia Law School professor, has written: "[T]axpayers promptly replaced the Iowa Supreme Court justices with 'judges already committed to their anti-bond- holder viewpoint.'"24 A tangle in the federal courts followed which would require more explanation than it is worth, but a headline from the New York Times probably says all one needs to know about human tendencies in time of woe: "Iowa Farmers Abduct Judge From Court; Beat Him and Put Rope Around His Neck."

In 1935 there were at least 3,252 municipal issues in default. It's worth noting that the bottom of the Great Depression was in 1933.