This post was co-authored with Anne Price, Director of the Insight Center for Community Economic Development's Closing the Racial Wealth Gap Initiative.

The financial lifecycle allows wealth to flow between generations in the form of gifts and inheritance. At birth, we receive the wealth and social standing of our family and, at passing, flow our contribution to wealth -- or a portion of it -- to our descendants in order to give them what we imagine will be a more financially stable life than we had.

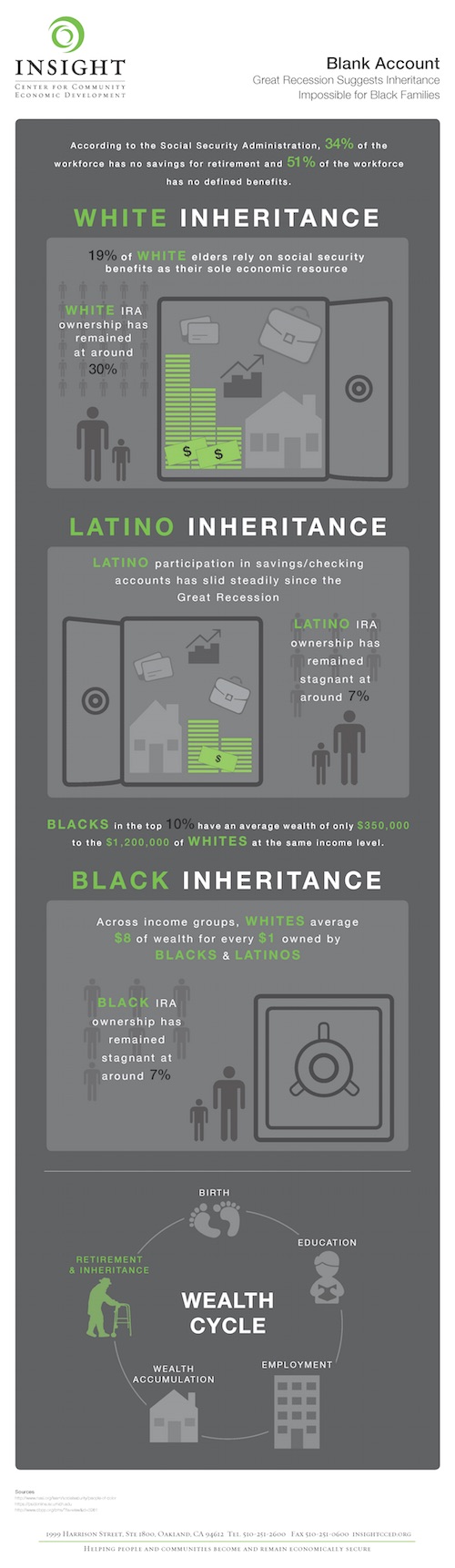

Contrary to this notion, an evaluation of the University of Michigan's Panel Study on Income Dynamics data by the Insight Center for Community Economic Development and social policy researchers Trina R. Shanks and Sharon Simonton tells a more complicated story for families of color. The evidence reveals that, for these families, that current levels of savings and asset building provide only a short-term safety net in dire times, especially for Blacks. Since the Great Recession, the number of Blacks and Latinos who hold savings or checking accounts fell steadily and IRA ownership for both groups has remained stagnant at only around 7 percent. During the same period, whites saw much more moderate decreases in the same wealth indicators.

Even among top income earners, structural and historical inequality has left Blacks with fewer assets than whites. Blacks in the top 10 percent have an average wealth of only $350,000 to the $1,200,000 of whites at the same income level. Across income groups, whites average $8 of wealth for every $1 owned by Blacks and Latinos.

History plays a major role in this lingering difference in savings volatility. Blacks have fewer safety nets to call upon in times of need or calamity -- and less access to wealth for opportunities like college and entrepreneurship. As the economy cycles through bull and bear markets, Blacks have been forced more often to make savings liquid for the bills of today at the expense of savings for tomorrow.

Americans across the board are less likely than ever to have accumulated enough wealth to retire and support the next generation. According to the Social Security Administration, 34 percent of the workforce has no savings for retirement and 51 percent of the workforce has no defined benefits. Programs like the Obama Administration's "myRA" retirement accounts are coming into effect, at least in pilot form, this year. These government-backed retirement accounts are aimed at providing millions of low- and middle-income Americans who don't have access to employer-sponsored retirement plans with accessible savings mechanisms that could begin to narrow the savings gap. But we need more.

Our economy boomed when the wealthiest Americans bore a significantly higher income and estate tax burden than they do today. During the 1950s our laws and policies ensured a broader sharing of our national wealth for individual and public investments. Surely, we would do well to heed the lessons of this history. The present hyper-concentration of wealth is creating dysfunctions in our economy that are strikingly unfair and ultimately unproductive, not only for society's most vulnerable, but also to our overall societal productivity and well-being.

Creighton University Scholar Palma Joy Strand suggests changes in tax law to treat inheritance as windfall wealth. This could immediately begin to shift our system away from the unfettered inheritances that next generation beneficiaries currently receive without ever having made any meaningful contribution to building the assets that pass down to them.

Economists William Darity, Jr., of Duke University and Darrick Hamilton of the New School for Social Science Research have proposed an interesting possible solution to address wealth disparities with "baby bonds". These would be like trust funds for every American child endowed at birth. Baby bonds would mature in federally managed investment accounts--with a guaranteed annual growth of between 1.5-2 percent -- until the beneficiary is 18. Under such a program, our youth would leave home for college, the work force, or entrepreneurship with up to $60,000 to jumpstart their lifelong financial stability. Such creative measures sound costly on their face, but imagine the growth and innovation our culture could see should our talented youth be freed from cycles of debt repayment and wealth disparities that increasingly plague our communities.

Going forward, we need to devise wholly new approaches to wealth distribution that at once honor private property and family rights, while also putting to better use our collective national assets. We need inheritance law reform and new taxes on larger estates that can enable reinvestment in emerging new talent. In an age where wealth is amassing atop an increasingly unattainable peak, it is our democratic duty to invest in equal opportunity and equal access. To do anything less would radically compromise our historical traditions as a nation, as well as our long-term economic self-interests.

--

Anne Price is the Director of the Insight Center for Community Economic Development's Closing the Racial Wealth Gap Initiative.

Henry A. J. Ramos is CEO of the Insight Center for Community Economic Development.