Release Date: March 10, 2015 (satire)

For release at 10:00 a.m. ET

The Federal Reserve Board We-Hate-Math Committee announced the true purpose behind QE.

Do derivatives confuse you? Do you hate bond math? We feel the same way! So we simplified your life with headache free QE math. Compound rates, equivalent rates, production functions: who needs old math?

You want to invest $100,000 for one year. A too-big-to-fail bank offers an interest rate of 10% per annum with quarterly compounding which reflects the bank's credit risk without taxpayer support for the financial system.

What is the equivalent rate with continuous compounding? What is the value of your investment after one year rounded to the nearest dollar?

The equivalent rate with continuous compounding = 4 x ln(1 + 0.10/4) = 9.877%. The future value factor is e^0.09877 = 1.103812

The future value of your investment is $110,381.

You may be annoyed that we simplified the calculation by rounding to the nearest dollar; we agree, that was oversimplification, but we love simplicity! (And that's chump change compared to how much you are getting ripped off in our new system.) So with our new math system, there is no need for rounding! In fact, there is no need to ever calculate equivalent yields or compound rates again!

You want to invest $100,000 for one year. A too-big-to-fail bank quotes the taxpayer subsidized interest rate of zero percent per annum with quarterly compounding. Notice that zero rates make compounding irrelevant!

What is the equivalent rate with continuous compounding? What is the value of your investment after one year?

Your equivalent rate is zero, and e^0 = 1, so your future value factor is 1. What could be easier?

The future value of your investment is $100,000. Unadjusted for inflation, of course!

We did away with inflation calculations, too. It is easy if you do not count food, energy, or healthcare.

Old Math for Economists

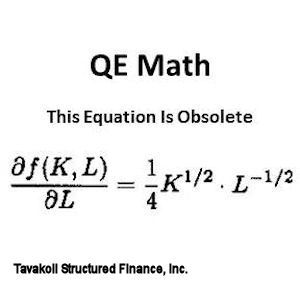

You remember the production function:

This represents factory output as a function of capital (K) and labor (L). Let's solve for the partial derivative of ƒ(K,L) with respect to L.

This equation tells us how much production (in the form of factory output) will change when we increase labor and keep capital fixed.

By keeping interest rates at zero, we encourage companies to buy back their own stock and engage in acquisitions instead of using that money for capital spending. The stock market loves it!

We know that with no net increase in capital spending, you can add more labor, but on the margin, it will be less productive, so we've eliminated creation of net new full time production jobs!

We know that with no net increase in capital spending, you can add more labor, but on the margin, it will be less productive, so we've eliminated creation of net new full time production jobs!

Also, by keeping interest rates zero, investors in "safe" investments get zero interest, so they are reluctant to spend. There is no need for increased production!

We can eliminate this old math production function entirely!

We keep production, capital, and labor constant and eliminate real growth!

The Genius of the New Math

You may ask when we will raise rates? With real productivity low, why would we raise rates? That's our story, anyway. Besides, European sovereign debt now trades at negative yields, so in comparison, zero is a windfall for investors! We don't need to take a step forward when everyone else is willing to take a step back. The new math is safe for the time being.

Bankers and financiers will continue to siphon cash from the productive economy; they will be able to buy more goods and services than savers, taxpayers and voters who could not be bothered to do the math.

Endnote: This is a work of satire, and this is not a press release from the Federal Reserve Bank Board We-Hate-Math Committee. Originally published at The Financial Report.

Our 2024 Coverage Needs You

It's Another Trump-Biden Showdown — And We Need Your Help

The Future Of Democracy Is At Stake

Our 2024 Coverage Needs You

Your Loyalty Means The World To Us

As Americans head to the polls in 2024, the very future of our country is at stake. At HuffPost, we believe that a free press is critical to creating well-informed voters. That's why our journalism is free for everyone, even though other newsrooms retreat behind expensive paywalls.

Our journalists will continue to cover the twists and turns during this historic presidential election. With your help, we'll bring you hard-hitting investigations, well-researched analysis and timely takes you can't find elsewhere. Reporting in this current political climate is a responsibility we do not take lightly, and we thank you for your support.

Contribute as little as $2 to keep our news free for all.

Can't afford to donate? Support HuffPost by creating a free account and log in while you read.

The 2024 election is heating up, and women's rights, health care, voting rights, and the very future of democracy are all at stake. Donald Trump will face Joe Biden in the most consequential vote of our time. And HuffPost will be there, covering every twist and turn. America's future hangs in the balance. Would you consider contributing to support our journalism and keep it free for all during this critical season?

HuffPost believes news should be accessible to everyone, regardless of their ability to pay for it. We rely on readers like you to help fund our work. Any contribution you can make — even as little as $2 — goes directly toward supporting the impactful journalism that we will continue to produce this year. Thank you for being part of our story.

Can't afford to donate? Support HuffPost by creating a free account and log in while you read.

It's official: Donald Trump will face Joe Biden this fall in the presidential election. As we face the most consequential presidential election of our time, HuffPost is committed to bringing you up-to-date, accurate news about the 2024 race. While other outlets have retreated behind paywalls, you can trust our news will stay free.

But we can't do it without your help. Reader funding is one of the key ways we support our newsroom. Would you consider making a donation to help fund our news during this critical time? Your contributions are vital to supporting a free press.

Contribute as little as $2 to keep our journalism free and accessible to all.

Can't afford to donate? Support HuffPost by creating a free account and log in while you read.

As Americans head to the polls in 2024, the very future of our country is at stake. At HuffPost, we believe that a free press is critical to creating well-informed voters. That's why our journalism is free for everyone, even though other newsrooms retreat behind expensive paywalls.

Our journalists will continue to cover the twists and turns during this historic presidential election. With your help, we'll bring you hard-hitting investigations, well-researched analysis and timely takes you can't find elsewhere. Reporting in this current political climate is a responsibility we do not take lightly, and we thank you for your support.

Contribute as little as $2 to keep our news free for all.

Can't afford to donate? Support HuffPost by creating a free account and log in while you read.

Dear HuffPost Reader

Thank you for your past contribution to HuffPost. We are sincerely grateful for readers like you who help us ensure that we can keep our journalism free for everyone.

The stakes are high this year, and our 2024 coverage could use continued support. Would you consider becoming a regular HuffPost contributor?

Dear HuffPost Reader

Thank you for your past contribution to HuffPost. We are sincerely grateful for readers like you who help us ensure that we can keep our journalism free for everyone.

The stakes are high this year, and our 2024 coverage could use continued support. If circumstances have changed since you last contributed, we hope you'll consider contributing to HuffPost once more.

Already contributed? Log in to hide these messages.