Update below.

This just in: AUSTERITY DOESN'T WORK!

It doesn't work here, it doesn't work in Europe, it doesn't work for state and local governments. I'm tempted to ask how many data points we need to recognize this crucial economic truth, but I'm afraid data points don't have much to do with it.

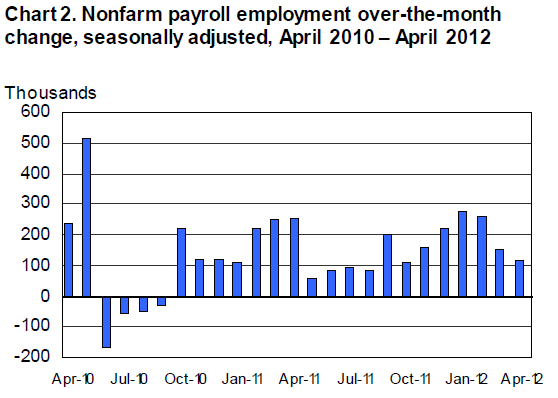

Another weak jobs report for April, with only 115,000 jobs added -- 130,000 in the private sector -- and a lower-labor-force-induced tick down in unemployment, from 8.2% to 8.1%.

You can see the trend in payrolls in the figure below, with acceleration toward the end of last year morphing to deceleration over the past few months. After last month's disappointing report, I was careful to point out that "one month does not a trend make" and there are some technical reasons -- mostly seasonal adjustments that haven't caught up with unusually warm weather -- to consider as well.

Source: BLS

Well, two months doesn't quite a trend make either, but it's getting closer. Average out some of the monthly noise, payrolls are up 176,000 per month over the past three months, compared to 218,000 over the prior three months. So, somewhat of a deceleration on a more reliable quarterly basis. But remember, the 200k trend was just okay -- typically coming out of such a deep trough as was the Great Recession, you'd like to see much bigger monthly numbers than that.

Key points for now with more to come later:

- State and local governments continue to shed jobs. They would be my first target for stimulus in a sane world. Last month, local education jobs were down 11,000 and they're down about 100,000 over the last year. Next time your friendly politician is jawboning about a) the benefits of austerity and spending cuts, and b) the importance of education, please point out the hypocrisy.

That's the punchline, I'm afraid. Weak labor demand is upon the land, and no one in power seems willing to do anything about it.

Update: A few more observations:

- One of CBPP's Unemployment Insurance experts, Hannah Shaw, tells me the following: since the beginning of the year 17 states with unemployment rates above 6.5% have triggered off of EB (extended benefits: extra weeks of UI in high unemployment states -- learn about it here), 8 of those states have unemployment rates of 8% or higher. It's possible that some of these folks leave the job market after their benefits run out and that could be playing a role in the low and stagnant participation rate.

This post originally appeared at Jared Bernstein's On The Economy blog.