Larry Mishel, president of the Economic Policy Institute, has an extremely useful piece up collecting all the reasons -- with evidence -- why the conservatives' "uncertainty" talking point is shovel-ready nonsense.

First, "uncertainty" in this context refers to the Republicans argument that it's government and central bank actions -- taxes, regulation, fiscal/monetary policy, health care/financial regulation reforms -- that are holding back the economy, not any of that ill-begotten Keynesian stuff, like lack of customers, orders, investors.

So how might you test for something like that?

Well, what about actual investment?

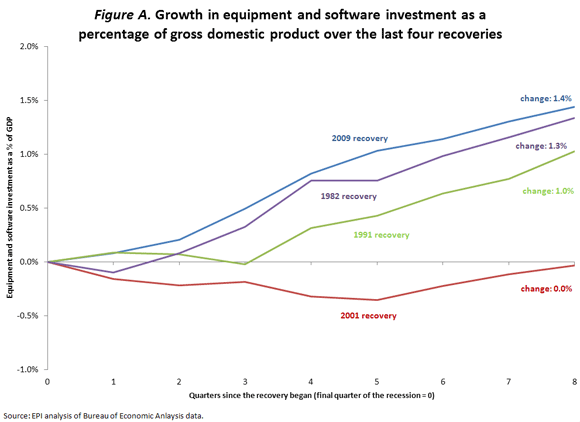

Investment in the current recovery has increased more than in it had at the same time period in the prior two recoveries and roughly the same as it did during the 1980s recovery [see figure]. In other words, this recovery is far more investment-led than the recovery under the pro-deregulation George W. Bush administration.

Private sector jobs, you ask?

...private sector job growth in this recovery looks much like job growth in recent recoveries, suggesting that businesses are not reacting to a new threat of potential regulations and taxes (the difference with this recovery is actually the loss of public sector jobs.

And then, of course, there's what the business folks, as opposed to their DC reps, actually say about what's bugging them:

...the regular National Federation of Independent Business (NFIB) surveys of small businesses found that the most common answer to the question, "what is the single most important problem your business faces?" was "poor sales." And while a number of businesses also cited regulation, the numbers were not substantially higher than under Presidents George W. Bush or Ronald Reagan and were lower than under Presidents Bill Clinton and George H.W. Bush.

None of this is to say "uncertainty" is not a problem. But while conservative politicians are busy jamming their perennial tax cut/deregulate agenda into the current context, the thing that businesses are truly uncertain about is when they're going to start seeing some customers again.

This post originally appeared at Jared Bernstein's On The Economy blog.