A number of economists, myself included, have been talking for awhile about the underlying strength of the recovery in terms of "escape velocity." The idea we're trying to convey -- or at least the one I'm contemplating -- is a virtuous cycle of growth begetting jobs, which in turn generates incomes, which supports more growth, etc.

Others talk about it in terms of "taking the training wheels off" of the economy, which I also kind of like in the sense that an economy that's growing too slow is like a wobbly bike ride, where there's not enough speed to ensure stability. The training wheels analogy also implies that the bike has enough momentum to take off fiscal and monetary stimulus... we're already taking off fiscal stimulus, by the way -- and too soon.

Well, someone asked me a good question the other day: how would we know if we've achieved escape velocity?

The best answer is, of course, multiple quarters of real GDP growth above trend, which right now is generally thought to be in the 2-2.5% range (perhaps a bit lower given slower labor force growth, but that could accelerate as the improving job market pulls more folks back in from the sidelines), followed by consistent quarters of robust job growth.

We started kinda, sorta, maybe, seeing something like that in recent months, with GDP averaging north of 2% and employment above 200K. But both of these trends are still too shaky for many economists' comfort (last Friday's jobs report didn't help), and while forecasts disagree, some predict slower growth ahead, jobs settling in around 150-200K, and unemployment staying about where it is, in the low 8's. That's about what I expect in the near term. It's not bad -- it's progress, moving steadily in the right direction --, but neither is it fast enough to ensure the bike doesn't wobble, especially if it hits a bump.

But there's another, related version of self-sustaining growth that also warrants a close look.* I don't have time to do it justice right now (Monday night basketball beckons!), but I can get things started, and I encourage others to join in.

In this version, you assume that absent a flock of albatrosses around its neck, the economy can pretty much be expected to grow at trend. I admit, there are many important nuances of great import that this theory brushes over (is not the underlying trend insufficient from the perspective of truly full employment; what about the structure of jobs? Too much finance? Too little job growth among startups? Accelerated labor-saving technology? A structural gap between pay and productivity?)

I worry intensely about all of those questions -- but it's also true that absent the weights around its neck, the economy is a lot more likely to be on track toward self-sustaining growth. Trend growth may not be sufficient for solving our structural problems. But it's surely necessary.

So, how do you gauge our economic progress in this regard? One good way is to think about the corrections that need to take place and see how far along they are. Once they're complete, we're more likely to hit escape velocity.

Like I said, I'll get the party started and will add more in days to come.

The first and one of most important corrections is housing. True, it was a home price bubble that got us into this uniquely deep mess, but it's also the case that housing, goosed by low interest rates, is a traditional escape route from recession.

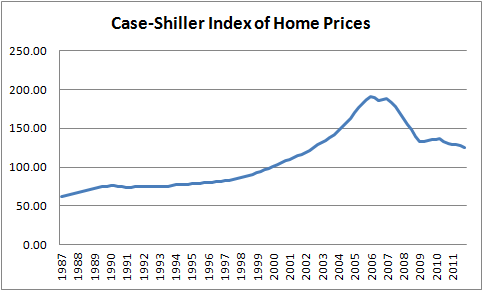

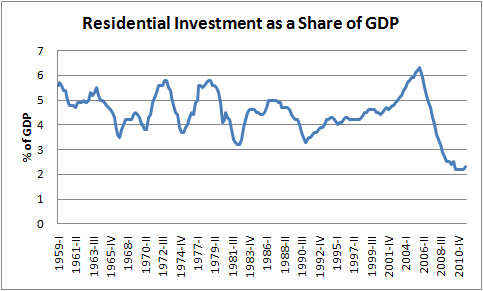

Here, two slides suggest the correction is largely, but not wholly over. First, the Case-Shiller price index doesn't appear to have bottomed and similarly, the residential investment contribution to GDP has yet to show any life.

Sources: 1, S&P's Case-Shiller Index, 2, NIPA

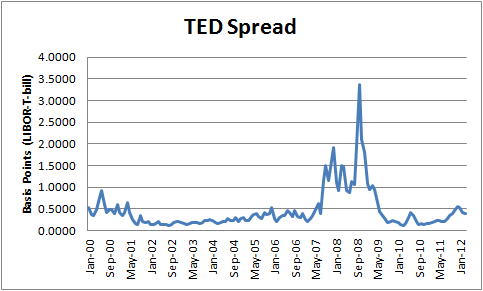

Next, the TED spread. This is a measure of riskiness in credit markets, and back in the heart of the GR, we talked about targeting the TED, recognizing that if it remained high, there was little hope of credit markets coming back on line. Think of the TED spread as a measure of blood pressure in the veins of credit. It's picked up a bit lately, but clearly credit default risk is way down from its heights. It's fair to say that this correction is and no longer weighing on the economy.

Source: FRED, 3mos LIBOR minus 3mos T-bill (that's right, I got the TED from FRED, like I SAID)

What else? There's household indebtedness -- very important, and well-analyzed here, related to housing, of course, and not yet fully corrected. But that's where I'll start when I can get back to this.

*I thank the great econometrician Jim Stock for helping me to crystallize these thoughts, but any mistakes in logic or measurement are mine, not his.

This post originally appeared at Jared Bernstein's On The Economy blog.