Suppose you were a policy maker who wanted to pivot away from emphasizing the need to reduce the budget deficit and towards the need to reduce the jobs deficit.

You'd get out there on TV and stress the 20+ million un- and underemployed, including the 45% of the unemployed who have been jobless for at least half a year (about as high as it's ever been). You'd stress the recent slowing of any already slow-growth recovery, and you'd stress the low cost of borrowing, which significantly boosts your bang-for-buck in terms of spending on jobs right now. And you'd remind anyone listening that you haven't forsaken the truly necessary work of getting the budget on a sustainable path. It's just that with unemployment at 9.1%, deficit reduction simply isn't the country's most important mandate right now. That would be jobs.

So far, so good. But what do you say to the follow up question: OK, you want to target jobs -- what's your plan?

I'd suggest starting with the Hippocratic Oath: First, do no harm.

Fading stimulus and state fiscal contractions could shave 1-2 percentage points off of GDP growth this year and next. If we let the payroll tax holiday and extended unemployment insurance benefits expire on schedule at the end of this year, look for the upper end of that range at least. So we start by avoiding that air pocket.

In the ongoing budget debates, both sides are in the process of agreeing on spending cuts (one side, importantly, is insisting on revenue increases too -- very important to seek balance here). OK, but again, from the "do no harm" part of the agenda: avoid starting those cuts too soon... I don't see what good comes from cuts this year or next.

Next, turn to infrastructure. Yes, it takes some time to roll out, but unfortunately, we've got time. It will be years before we see full employment again.

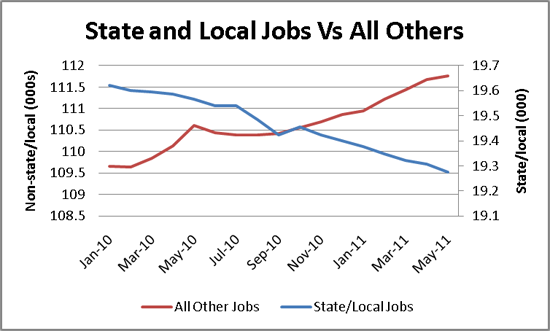

Then, I'd get back to the very tough conditions in some of the states. They have to balance their budgets, and that's leading to aggressive layoffs. Check out this slide showing payrolls of state and local government versus all other sectors. The latter is growing, the former, crashing. States and cities have laid off about 350,000 workers over the past year and a half.

Source: Bureau of Labor Statistics

I'd say, "I know public sector workers are taking it on the chin in cities around the country right now, but does this make sense? Do we really want fewer teachers in the classroom right now? Do we really want to have to cut back health coverage for the low income folks in what's still such a tough economy?" Another round of state fiscal relief is needed.

Finally, I'd close out with a couple of ideas for helping boost our manufactured exports, a key channel of growth at a time like this. In fact, one corrective mechanism in a weak economy with low interest rates is the weaker value of the dollar in international markets, which makes our exports cheaper and their imports more expensive. But if other counties, like China, manage their currency (keeping it cheap relative to the dollar) they prevent this important adjustment.

The White House has pushed back pretty hard on this, but I'd go further. There are a couple of bills in the Congress that ratchet up the pressure on currency managers and they've gotten some bipartisan support. I'd put them on the agenda.

The other idea is a great manufacturing tax credit -- the 48C Advanced Energy Manufacturing Tax Credit (man, we really got work on these names!) -- that was really effective during the Recovery Act -- and it's green!

So if you want to pivot, that my suggested agenda. There's more one could think of -- nothing on housing here, and that's a clear problem as well (I'll post some ideas on that space in the next few days).

You might not get too far in today's climate, but if you want to pivot, this feels like a pretty clean set of ideas worth fighting for right now.

Lemme know how it works out for you.

This post originally appeared at Jared Bernstein's On The Economy blog.