When the trustees of the Social Security and Medicare programs release their annual reports, one of the first thing folks look for is whether the life of the trust funds that finance these retirement security programs have been extended or reduced.

Well, in Monday's release, the life of the Social Security trust fund was reduced by three years, from 2036 to 2033 (without changes to inflows or outflows, at that point Social Security would be able to pay about 75% of scheduled benefits). The date for the Medicare Hospital Insurance fund was unchanged.

My CBPP colleagues take you through the relevant conclusions here and here. The key takeaway from where I sit is that these remain critically important programs whose future can and should be ensured by policy actions designed to enable both programs to continue to provide retirement security for generations to come. Such actions should be careful not to hurt the security of middle and lower income retirees.

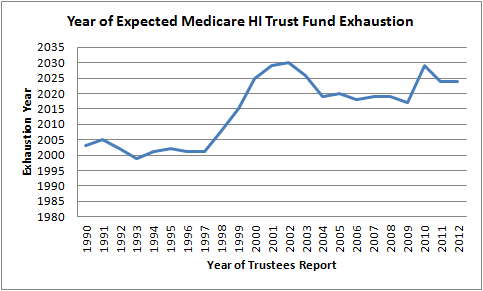

My point here, however, is a simple one regarding the exhaustion of the trust funds. The figures below show the exhaustion dates projected by the trustees over the last few decades. Note that they move around -- a lot. The Medicare hospital insurance trust fund has generally increased since the 1990s, as a function of legislative measures, like the Affordable Care Act, that extended its life (ACA added eight years to the HI fund).

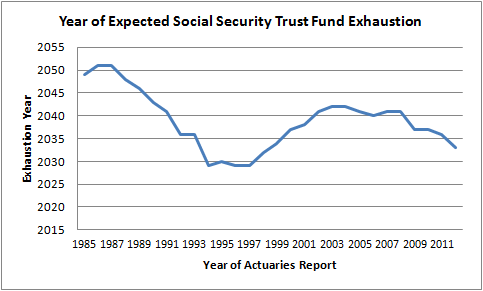

The movements in the Social Security trust fund have been more of function of the economic and demographic assumptions (e.g., increased life expectancy); they range from over sixty years -- in 1985, they didn't expect exhaustion until 2050 -- to around 20 years today.

The figures are not intended to lessen the urgency of meeting the fiscal needs of these programs. But it is important to remember that these are forecasts based on a lot of moving parts, and the Great Recession is very much in play here.

As with so much else in our fiscal and economic landscape these days, the best thing to do in the near term is everything we can to get the recession behind us and get back on a stronger growth path.

Source: Trustees Reports.

This post originally appeared at Jared Bernstein's On The Economy blog.