The IMF has sharply marked down its forecast for world growth and it now expects a mild recession in the euro area. Naturally, weaker world growth will affect economic activity in Latin America and the Caribbean.

Concretely, the Fund expects the world economy to grow by just 3.25 percent in 2012, three-quarter percentage points lower than our September forecasts.

In contrast, our forecast for the U.S. economy for 2012 is unchanged, as incoming data signal a stronger -- but still sluggish -- domestic recovery that will offset a weaker global environment. Commodity prices will be affected by ebbing global demand, with oil projected to fall about five percent and non-oil commodities about 14 percent.

Softer growth

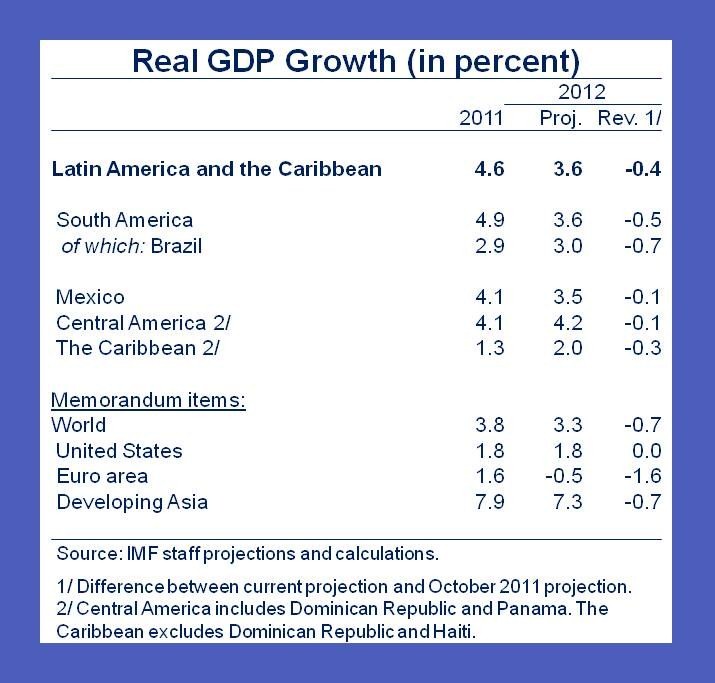

As for Latin America and the Caribbean, as I foreshadowed in my recent blog, a weaker world economy and softer commodity prices translate into a gloomier outlook (see table). We've marked down our growth forecasts for the region as a whole by about 0.5 percent for this year. The overall markdown for Latin America is a bit smaller than for the globe, because much of the region's economies still enjoy good domestic momentum and stable financial systems.

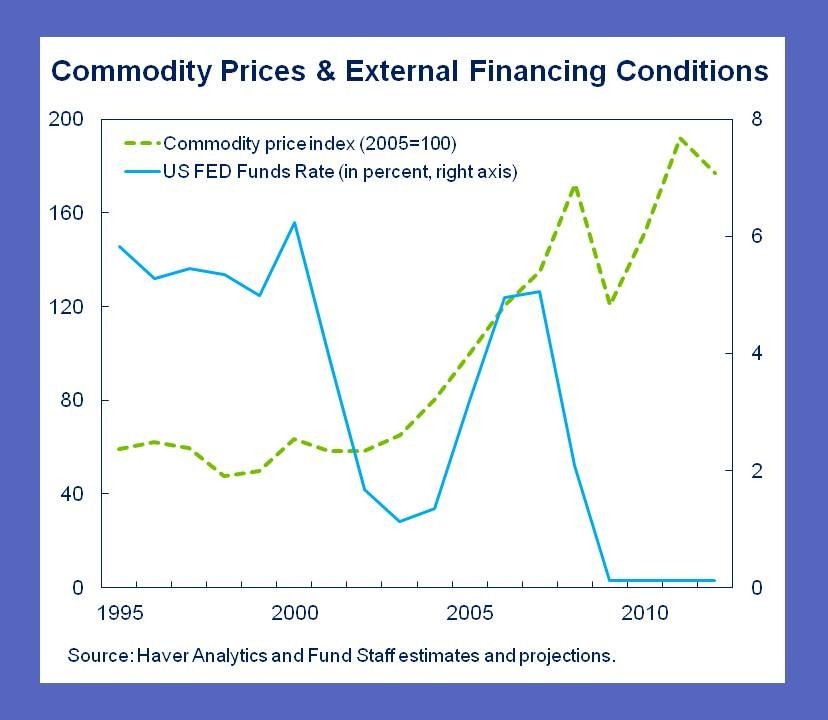

Moreover, commodity prices remain well above their long-term trend, despite the recent decline, and external financing remains relatively cheap and readily available (see chart). While global uncertainties have sparked volatility in capital inflows, we have yet to observe a reversal.

Moreover, commodity prices remain well above their long-term trend, despite the recent decline, and external financing remains relatively cheap and readily available (see chart). While global uncertainties have sparked volatility in capital inflows, we have yet to observe a reversal.

But to be sure, there is a lot of variation in our forecast revisions within the region.

- In South America, which until recently was growing well above trend, less favorable external conditions are expected to crimp output growth, dampening brewing overheating pressures.

- The outlook for Mexico and Central America is broadly the same as in October, as we've left our U.S. outlook unchanged.

- Meanwhile, growth in the Caribbean will continue to lag, held back by weak tourism flows from advanced countries and high public debt.

Take precautions

But let me emphasize, the outlook for the region hinges on policy action in Europe. Policymakers there need to intensify their efforts to contain the crisis, and put an end to the rise in sovereign spreads and the cutback in bank lending that threaten the global economy in 2012. These efforts should be supported by appropriate policy actions elsewhere in the advanced and emerging world. Otherwise, as the downside scenario in the IMF's recent global outlook suggests, world growth in 2012 could be some 2 percentage points lower, dragging down commodity prices and heightening financial strains. For our region, this would mean more sluggish exports, worse terms of trade, and tighter borrowing conditions.

To add this all up: how should policymakers in our region react? It's always good practice -- as the expression goes -- to hope for the best (or at least better times), but to prepare for the worst. More specifically, they should take action on three fronts:

- Rebuild fiscal buffers, to maintain fiscal credibility -- the euro crisis vividly illustrates the costs of losing it -- and prepare for a further deterioration in global conditions.

- Be ready to ease monetary policy, where strong institutions and low inflation would permit it. Watch financial systems closely for signs of stress.

- Maintain flexible exchange rates -- our research shows that these buffer shocks, particularly from commodity prices.

From iMFdirect blog and Diálogo a Fondo