Excerpted from Robert D. Auerbach, Deception and Abuse at the Fed: Henry B. Gonzalez Battles Alan Greenspan's Bank, 2008. Courtesy the University of Texas Press.

Getting Pressed during Pre-Wash

The first-floor lobby of the Fed Bank in Kansas City has the cavernous, cold appearance of a classic, old-time bank lobby. In the mid-1970s, a ceremony was held there to honor the retiring president of the Kansas City Fed Bank. Most of the bank's employees gathered behind the bank's officers. The officers included vice presidents and assistant vice presidents, all smiling proudly in front of a larger, more restrained crowd of Fed employees, who were thankful for this entertaining break from work.

The incoming and outgoing presidents of the Fed Bank faced the group. At the end of a laudatory speech about the contributions of the retiring president, a high school chorus broke into hallelujahs as the new president pulled the sheet off of a statue. On top of a large cutout of Superman's body was a picture of the head of the retiring president. There were applause and laughter.

The retiring president was a very amiable man with long executive experience at a large private-sector company. He had looked and acted quite lost when it came to officiating at the "pre-Wash meeting," which was held on the Thursday or Friday before the Federal Open Market Committee (FOMC) meeting, on Tuesday, at the Board of Governors in Washington, D.C. At the pre-Wash meeting, the president, his chief economist (the senior vice president in charge of the research department), and the staff of economists would file into a conference room. There was heightened interest and intensity because the president had been rotated into his one-year voting membership on the FOMC. (Four FOMC seats are rotated among eleven Fed Bank presidents; the New York Fed Bank president is a permanent member of the committee.)

At the pre-Wash meeting, the president might tell a story about the experience of a relative in a store with high prices. Mostly, he would say nothing. At one of these meetings he read a poem that he had written and then delivered at the last FOMC meeting. He bragged that Fed chairman Arthur Burns had specifically complimented him on his fine poem. Those in attendance at the pre-Wash meeting assumed frozen smiles as he eagerly recited something like "The money supply went up the staircase so fast that we all knew it would not last. Down, down it came back to run just where it started from." Then the awkward silence was interrupted by the chief economist, who asked the staff for their selection of policies.

Before the pre-Wash meeting, the Board of Governors would send out the menu, which consisted of three choices for money growth and an associated band of short-term interest-rate targets.1 Each economist could say a, b, or c and offer supporting comments. Nearly all economists selected option b because that looked like the one most agreeable to management and would not cause a fuss in Washington by appearing to support "extreme" views. As a staff economist at the Kansas City Fed Bank, I decided not to play the game at one pre-Wash meeting in the mid-1970s, and suggested a different policy, which I called d. I presented reasons for this policy. An officer of the bank immediately asked me to accompany him out of the room. We had a very friendly discussion about my wife and young child. The officer advised me that if I wanted to continue to be able to pay the mortgage on our newly purchased house, I should be a team player.2

Who Determines Monetary Policy?

Many of the 500-plus economists at the Fed perform similarly as advisers on domestic monetary policy. Their role is to enter mahogany-paneled conference rooms en masse and chime in during serious discussions of monetary policy with Fed Bank officials a day or two before FOMC meetings.

On the following Tuesday, the FOMC convenes in Washington. FOMC members gather around a large conference table. They enter through one set of doors, and the Fed chairman enters through a door from his adjoining office. They speak into microphones with voice-activated green lights that indicate the recording of their utterances. As described in Chapter 6, some members claimed not to know what the green light indicated. If true, it was not a good sign, given the skill level desired in FOMC members. In other seats, away from the conference table, sit employees of the Board of Governors and the twelve district banks.

Greenspan's dominance over the Fed governors appears to have been nearly complete, according to the description given by former governor Laurence Meyer. Meyer reports that Greenspan "would meet individually with the other governors during the week before FOMC meetings."3 He "would sit down and explain his views on the outlook and his 'leaning' with respect to policy decisions that would be considered by the Committee at the upcoming meeting. . . . Some governors found this rather off-putting." Given Meyer's view that the "Chairman is expected to resign if the Committee rejects his policy recommendation," "off-putting" would be an understatement for describing the process imposed by Greenspan. "After a while," Meyer reports, Greenspan "abandoned the private talks" and instead gave his views one day before the FOMC meetings to the governors at a Board meeting. Meyer also reports that during his term as governor, no governor dissented from Greenspan's views, and there was "an implicit commitment to support the Chairman." Meyer also describes FOMC meetings as being "more about structured presentations than discussions and exchanges."4 In this picture, Greenspan's dominance of the process reduced the other governors' contributions to Fed policy to a triviality. Meyer draws a very different picture from what occurred at the Volcker Fed with the "gang of four" (described in Chapter 10).

The Board staff also sets the tone at FOMC meetings with their analyses. Their reports serve as the vehicle for much of the discussion about monetary policy. The staff reports generally support the chairman's views, for obvious reasons.

Members' opposing views could potentially change policy. If such views come from the subservient Fed Bank presidents, pressure from the Board of Governors can affect their peace of mind as well as their salaries and tenure, since at their next yearly review the Fed chairman can lower the hammer. Unlike governors, who can be removed only by congressional impeachment, Fed Bank presidents can be fired or their contracts not renewed for another five-year term. Fed Bank presidents have left in the middle of their five-year terms with an official announcement of voluntary departure.

All but the occasional recalcitrant official will vote in conformity with the chairman; Meyer reports three dissents by Fed Bank presidents during his term. A few principled presidents withstood the substantial pressure to conform, most notably the late Darryl R. Francis, the former president of the St. Louis Fed Bank. He may have lasted for two terms--ten years--because he had well-known outside support and had assembled a skilled and renowned research department.5

The chairman heads the large staff at the Board of Governors. He is in close contact with the president of the United States. He meets frequently with the secretary of the treasury, and the Fed staff is in contact with Treasury staff. Many members of Congress seek the Fed chairman's advice and try to be seen on television with him at hearings, since he is the face of the Fed and sometimes, as in the cases of Burns and Greenspan, the country's enshrined economic sage.

How Much Should Central Bankers Know about Central Banking?

Many FOMC members have been either trained economists or people who became very knowledgeable about central banking through their work experience. The economic welfare of hundreds of millions of people can be threatened when some of the voting members of the FOMC are completely or nearly ignorant about central-bank functions and their effects on the economy. They may be unable to determine which staff suggestions or media stories have merit. Even worse, economic analysis produced by the Fed's huge staff of economists--full of "aggregates," "indexes," and "high order filters"--could be impenetrably confusing. Untrained members can become rubber stamps for the chairman's views. An FOMC member can maintain this neutered stance at meetings and still participate for the record by reciting anecdotal events and imprecise descriptions of the economy, and then vote for whatever the chairman wants.

FOMC transcripts show that the staff reports presented to the committee are often primitive, lacking an analytical framework as well as even modestly sophisticated statistical evidence. The top staff of the Board of Governors delivers policy in a form suitable to the chairman.

This description does not automatically mean that only well-credentialed economists should be appointed to the Board. Many well-credentialed economists, in think tanks and on academic faculties, would be ill suited for these decision-making positions. Many are partially or completely tone deaf with respect to politics, a desirable trait when conducting research projects that seek answers in a world without political constraints. But an apolitical sensibility can be a shortcoming for public service, especially in anyone who will have a hand in setting Federal Reserve policy. Congress can involve a Fed official in days of painful testimony in front of committee members who are often delighted to play to the television cameras by toying with a politically inept foil.

Milton Friedman, the Nobel laureate who devoted much of his research to studying monetary policy, emphasized the quandary about expert knowledge when he compared former Fed chairman William McChesney Martin, Jr., who served in that position for nineteen years (1951-1970), with former Fed chairman Arthur Burns, who served eight years (1970-1978). Burns was an economics professor from Columbia University. Friedman had been his student at Rutgers University, and they were friends, although Burns's advocacy of faster money growth and price controls put a strain on their relations.

Martin became the first paid president of the New York Stock Exchange, the "boy wonder of Wall Street." According to his obituary in the New York Times, he was well aware of his limited knowledge of central banking: "When he took office, Mr. Martin said he had told himself: 'My gracious, here I am the new Chairman of the Fed, and I'm not the brightest fellow in the world but I'm working hard on this--and I haven't the faintest idea of how you figure the money supply. Yet everybody thinks I have it at my fingertips.'"6

Friedman wrote to me: "It is not clear to me that competence about monetary policy will necessarily lead to better monetary policy. I offer you the example of the contrast between Martin and Burns. I am sure that both you and I would agree that in any academic sense Burns was far more competent, understood the operation of monetary policy far better than Martin. Yet I suspect that you and I will both agree that monetary policy was better under Martin than it was under Burns."7

This assessment is consistent with the lower average rate of inflation during the Martin years (2.1 percent) and the much more rapid average rate of inflation during the 1970s (6.5 percent) when Burns was Fed chairman. 8 Nevertheless, dismissing the need to know what you are doing is alarming, given the powers that are placed in the hands of Fed officials.9 A serious mistake in managing the money supply can cause an explosion of inflation, which would wipe out much of the purchasing power of millions of people. Likewise, a rapid sustained contraction of the money supply can cause a recession, leading to millions of people losing their jobs.

Does It Matter If Fed Officials Are Unable to Explain Their Jobs?

To illustrate the problem of Fed officials' inability to explain what they are doing, consider the example of an esteemed former manager of the New York Fed Bank's open-market desk. He had the important task of overseeing the daily auctions that are central to the Fed's management of the nation's money supply. He came to a seminar held by Milton Friedman at the University of Chicago in the 1960s. This famous weekly seminar was called "The Money and Banking Workshop." The small group of attendees consisted of scholars from around the world and PhD students whom Friedman had admitted to the workshop. The procedure required each invited speaker to submit a paper in advance. The speaker was not to read the paper to the group, since that would be redundant. Friedman would begin by calling out: "Page one." That was the signal for any member of the workshop to ask the speaker a question about something on page one of the paper. The questioning was intense but very productive--that is, until Friedman invited this retiring manager of the New York Fed Bank's open-market desk.

This speaker broke precedent by not submitting a paper in advance. Friedman began by asking him how he conducted open-market operations: What precisely did he use as signals? How precisely did he use various variables in determining his actions? He could not answer any of these questions except with generalities that produced frowns on workshop members. Friedman continued to search for some kind of specific answer. He asked the Fed official what he would tell his successor to do in handling various situations. The Fed official said there were no specifics about that; each situation was different. Friedman did not end the workshop as he had a previous meeting: when someone complained that the paper being presented was so poor as to be a waste of time, Friedman adjourned the meeting. Since the Fed official was obviously not an academic researcher or a scholar, the seminar ended courteously.

The Fed's open-market manager was an able official and had had a successful career. Like many successful private-sector traders, he could not present a clear description or analysis of his methods. Despite his successes or failures at the Fed, his inability to describe what he had done meant that his experience and knowledge were not passed on to future open-market managers.

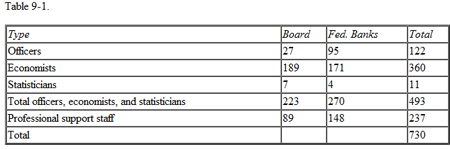

Source: This table is from an attachment to a letter dated September 15, 1993, from Fed chairman Greenspan to Rep. Gonzalez. The note on the table reads: "This table covers all formal positions involved in economic research/management activities. For Reserve Bank only filled positions are counted, but vacancies are included in the Board count." Author's collection.

When More Than 500 Economists Are Not Enough

Although many of the excellent economists at the Fed appear to have little effect on monetary policy, they produce some good papers. They write articles for the Fed's extensive publications, many of which have been moved onto Fed Bank Web sites. Many are useful summaries of economic topics. Other economists are officials in management positions at Fed Banks. How many economists are employed at the Fed? A reasonable estimate is that more than 500 economists were employed at the Fed in 1993. Greenspan responded to an inquiry from House Banking chairman Gonzalez by verifying that the Fed employed 360 economists in its research departments, as shown in Table 9-1.10 In addition, 122 officers in research departments were presumably economists, making a total of 482. This figure did not take into account the economists employed in other parts of the Fed. This makes the Fed one of the largest U.S. employers of economists. In 2000, the Department of Labor employed 1,076 economists, and the Department of Agriculture had 525.11

The Fed also extends contracts to economists in academia. A Gonzalez-led investigation collected information on the Fed's use of outside contracts for academics. During the thirty-six months ending October 1994, the Board and the twelve Fed Banks awarded 305 contracts to 209 professors, virtually all of whom were economists. The total payments on contracts in this period amounted to nearly $3 million, an average of $81,091.14 a month.12 Thirty-eight economists had contracts that paid more than $20,000. Many of the economists had multiple contracts, generally from different Fed Banks or the Board. One economist had six contracts, three had five, four had four, and fifteen had three.13

These payments were not extravagant, and probably attractive to professors who were not well paid compared to their business-world counterparts. There was no evidence that these outside consultants failed to provide useful advice or research efforts for the Fed. Questions may be asked about the multiple Fed Bank contracts.

According to an article by Stephen Davies: "The New York Fed, which has the largest staff of economists outside of the Federal Reserve Board because of its role in executing monetary policy and watching financial markets, listed only a handful of outside economists. By contrast, the Federal Reserve Bank of Minneapolis has what is by far the most ambitious program of hiring outside researchers. Records show that the bank signed 105 contracts [from January 1, 1991 to June 30, 1993] with academics, including a number from universities outside the United States. Many were one-time deals to write papers for the bank."14

There are problems associated with the Fed's employing or contracting with large numbers of economists. The problems arise when these economists testify as witnesses at legislative hearings or as experts at judicial proceedings, and when they publish their research and views on Fed policies, including in Fed publications.

In 1992, roughly 968 members of the American Economic Association (the largest association for economists in the United States) designated "domestic monetary and financial theory and institutions" as their primary field, and 717 designated it as their secondary field. If a significant percentage of these people either work directly for the Fed or contract with the Fed, there can be consequences, as Milton Friedman described in 1993, first in a letter to me and then to Reuters: "I cannot disagree with you that having something like 500 economists is extremely unhealthy. As you say, it is not conducive to independent, objective research. You and I know there has been censorship of the material published. Equally important, the location of the economists in the Federal Reserve has had a significant influence on the kind of research they do, biasing that research toward noncontroversial technical papers on method as opposed to substantive papers on policy and results."15 Reuters reported Friedman's statements in an interview: "The Fed's relatively enhanced standing among the public has been aided 'by the fact that the Fed has always paid a great deal of attention to soothing the people in the media and buying up its most likely critics.' Recognizing that the Fed employs 'probably half of the monetary economists in the U.S. and has visiting appointments for two-thirds of the rest,' he [Friedman] saw few among the academic community who were prepared to criticize the Fed policy."16

Some Personal Experience with Censorship and Nondisclosure Agreements

The working conditions for some economists at the Fed are excellent. When I was hired at the Kansas City Fed Bank in the mid-1970s, I doubled the salary I had made as an assistant professor. I was shown a spacious, mahogany-paneled office with a large, impressive desk, situated along a corridor of other economists' offices. I was told that I would have access to several programmers for statistical research and that all the newspapers and journals that I wanted would be delivered to me. Best of all, I could spend 90 percent of my time on my own research and use the other 10 percent for developing reports for the bank.

Only one caution from the Fed Bank officer who headed this research-department group seemed a bit awkward, a sign of the bureaucratic rules that foster regimental conformity. I was told that security at the bank required me not to wander around. I was to stay in my office except to go to the men's room, to the cafeteria for lunch, or on official business, such as a meeting. It was the equivalent of being told to knock before coming out of my office. The cachet of the splendid office faded. I began to miss the freedom of the small bare-walled furniture-deprived office I had left in academia. Nevertheless, many first-rate well-trained economists are attracted to the Fed by the salary and the perks. Some who oppose the Fed's policies bear this burden with some pain. They learn how to mentally ignore or minimize the restrictions that this bureaucracy imposes.

For an economist who spent many years earning a PhD and believed in the production of unbiased contributions to knowledge, censorship could be difficult to ignore, a bureaucratic sliver under the fingernail. Articles intended for Fed publications had to be sent to the Board in Washington for editing and approval. Because of this, the publications should indicate that the material has been emended to comply with Fed policies--something along the lines of "EDITED BY THE FEDERAL RESERVE FOR GENERAL CONFORMITY WITH ITS VIEWS AND POLICIES ." Without this sort of label, Fed publications appear to be unbiased products of its huge think tank.

One type of censorship could have more immediate effects on the Fed's monetary policy. Each of the twelve Fed Banks prepares several reports designated by color: the Beige Book is about economic conditions, and the Red Book is about banking conditions, including any problems at banks in the district. Those books are available to the FOMC members at their meetings, and, presumably, the contents affect their decision making.

Assigned to help compile the Red Book, I began calling the CEOs of the banks in the 10th District (Wyoming, Colorado, Kansas, Nebraska, Oklahoma, and parts of Missouri and New Mexico). It became immediately apparent that there was trouble. A popular anchor on one of the heavily watched morning news programs had announced that the Fed Banks were selling Treasury securities in denominations as small as $1,000. This information by itself was correct, but $1,000 was not the market price at which these securities could be purchased; it was the final return in three months. The market price was determined by an auction. The interest on three-month Treasury bills was attractive to many savers because banks were then paying zero interest on checking accounts. The three-month Treasury-bill rate had averaged 6.23 percent in 1974, 1975, and 1976.

There was a stampede to some of the private-sector banks in the 10th District to buy these securities, as well as some chaos because of incorrect information about their market price. There were long lines of customers at many of the banks in the district. They did not have the personnel to explain the pricing policies of these government securities to the insistent customers who had "heard it on TV." The bankers issued almost frantic appeals for help in advising citizens about the mistake. That should have concerned the Fed, since its clients, the U.S. public and the private-sector banks, were having trouble.17

I dutifully summarized the problem and included it in a report for the next Red Book. The head of the research department called me into his office and told me to take the problem out of the report. He was told that everything was fine in the 10th District. I left, humming quietly "Everything's Up to Date in Kansas City" (from Oklahoma!). Unfortunately, it was no joke to realize that information sent to the Board was censored to avoid admitting any problems existed. This type of cover-up is expected in any large bureaucracy. However, the muddled organization of the Fed makes it much more difficult to enforce uniform rules across all twelve district facilities.

An insightful example of limitations for an economist doing unbiased research is the nondisclosure statement (officially labeled "Nondisclosure Clause") that contracted economists signed before obtaining consulting jobs with the Board of Governors. According to the story by Stephen Davies mentioned earlier, "in the case of the Federal Reserve Board all contractors are required to sign a non-disclosure statement promising to keep all information confidential. The statement is broadly worded to prohibit the release of any information 'relating to past, present, or future activities' that can be considered 'damaging to the Board.'"18 An economist who is doing research on monetary policy and wants to be critical of the Fed's policies should not be limited by such nondisclosure clauses; an economist testifying before Congress must not be. At the beginning of any testimony concerning Fed policies, congressional witnesses should provide information about any such limitations, especially nondisclosure agreements with the Fed, and any money they have received from the Fed for contracted services. Disclosure forms are required (as of 2003) for witnesses before the House Banking Committee. Nondisclosure clauses signed by academic economists who have been under contract at the Fed should also be revealed.

A number of economists interviewed by Steve Davies, including those with contracts with the Fed, applauded the contracts. They said that consulting was an opportunity for the best minds in academia to lend their expertise to the Fed and that it was mutually beneficial. They said they did not bias their research. Several economists reportedly told Davies that they talked to Fed staff members about statistical models and not about what they thought "interest rates are going to be"; some stated that they did not "comment on current policy" because they were not experts "on what's happening at the moment."19

Compare these answers with the call I received at Congress in the 1970s from the late Arthur Okun, an esteemed economist who was certainly very honest and who had been chairman of the Council of Economic Advisers in the Johnson administration (1968-1969). He said he would like to comply with the committee's request that he testify. However, he was receiving a check each year for $3,000 from the Federal Reserve, and he simply did not want to testify without stating this fact, which would be a potential conflict of interest. When asked what he did to receive this payment, he replied that the Fed probably wanted to call on him for his views, but no required work was involved. It was a small payment, and Okun evidently knew that it might not be considered payment for his advice, which he probably would have been happy to provide to the Fed free.

Of course, the Fed would reject these criticisms. It does, however, mention the existence of "bureaucratic restraints" in its Web site solicitation for economists (as it appeared in January 2003): "The Board offers a work environment that minimizes bureaucratic constraints, encourages creative thought, and stimulates the lively and free exchange of ideas." A "little" bureaucratic restraint never hurt anything, except possibly unbiased research about the operations and policies of this powerful governmental bureaucracy.

The above censorship warning should appear on any Fed material distributed to high school teachers and college professors. In 2005 the Fed began publishing its message on "economic and personal education" with the help of USA Today.

www.FederalReserveEducation.org

The Federal Reserve System is committed to economic and personal financial education.

USA TODAY and the Federal Reserve are working together to introduce students and educators to the wide variety of instructional resources available through the Federal Reserve Education website and especially the new FED 101 website.

The Federal Reserve Education website provides links to instructional materials and tools that can increase student understanding of the Federal Reserve, economics and financial education. All of the Fed websites, curriculum, newsletters, booklets and other resources are free.

As the Fed belatedly moved from relying on hard-copy mass mailings to exploiting the Internet, the New York Fed Bank advertised its new Web site in 2006: "The Research Group recently launched Course Readings for University Educators, a new website that highlights the value of the Bank's research publications as teaching tools. The site's key element is a directory of recommended readings organized by course title and level of mathematical complexity. Finance and economics professors can select a course and then link to articles from our principal research series that might be assigned to students in that course."20

Entertaining Potential Congressional Witnesses

The House Banking Committee received information about a three-day Fed conference on financial derivatives to be held in Coconut Grove, Florida, on February 24-26, 1994. It happened that the committee was planning to hold hearings on financial derivatives. Coincidence? The information received by the committee indicated that participants at the Fed conference were told to bring their golf clubs. The preliminary program showed the conference would adjourn at one thirty on the second day, after a noon speech by Greenspan, and except for a reception "with spouses" at seven that night, would not reconvene until a "continental breakfast" scheduled for nine the next morning, and it would then adjourn again at one thirty in the afternoon. Why was the Fed using taxpayers' money to entertain economists who might well be called as congressional witnesses? At least one economist understood what was happening. As Gonzalez later put it: "The purpose of the early adjournment is to allow time to examine and explore the local golf terrain, according to one prominent economist who was invited to attend and was advised to bring his golf clubs. . . . This may all look like small potatoes to individuals with good jobs. But to American taxpayers who are paying their bills and to the 2.3 million civilian governmental employees who fear that many of them will be shown the door in the name of efficiency and eliminating waste, the Federal Reserve is throwing a little Miami Beach sand in their faces."21

On behalf of House Banking, I called the Atlanta Fed Bank, which was sponsoring the conference, to ask why a conference was being held at a resort where the Fed would be paying $325 a day for each attendee's room, when the Atlanta Fed Bank had adequate meeting space. Displeased with the inquiry, the Fed Bank president informed me that even Fed chairman Greenspan would be in attendance. I said that made matters worse, since it would increase the cost of the conference. The Fed Bank president then complained in writing to me. Gonzalez thanked me for the work I was doing and said the letter was proof of the arrogance of the Fed and the need for oversight.22