Some press accounts and various advocates have labeled the Regional Greenhouse Gas Initiative (RGGI) as near "the brink of failure" because of the recent trend of very low auction prices. Likewise, commentators have recently characterized the European Union Emission Trading Scheme (EU ETS) as possibly "sinking into oblivion" because of low allowance prices. Since when are low prices (which in this case reflect low marginal abatement costs) considered to be a problem? To understand what's going on, we need to remind ourselves of the purpose (and promise) of a cap-and-trade regime, and then look at what's been happening in the respective markets.

The Purpose and Promise of Cap-and-Trade

A cap-and-trade system -- if well-designed, implemented, and enforced -- will limit total emissions of the regulated pollutant to the desired level (the cap), and will do this (if the cap is binding) in a cost-effective manner, by leading regulated sources to each make reductions until they are all experiencing the same marginal abatement cost (the allowance price). Thus, the sources that initially face the highest abatement costs, reduce less, and those sources that face the lowest abatement costs, reduce more, achieving system-wide minimum costs, that is, cost effectiveness. So, the purpose and promise, in a nutshell, is to achieve the targeted level of aggregate pollution control, and -- if the cap is binding -- do this at the lowest possible cost.

RGGI Allowance Prices

The Regional Greenhouse Gas Initiative (RGGI) -- a downstream cap-and-trade system for CO emissions from the power sector in 10 northeast states (Connecticut, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Rhode Island, and Vermont, with New Jersey now in the process of withdrawing from the coalition), was launched with relatively unambitious targets, principally in order to keep prices down to prevent severe leakage of electricity demand and hence leakage of CO emissions from the RGGI region to states and provinces outside of the region (mainly from New York to Pennsylvania).

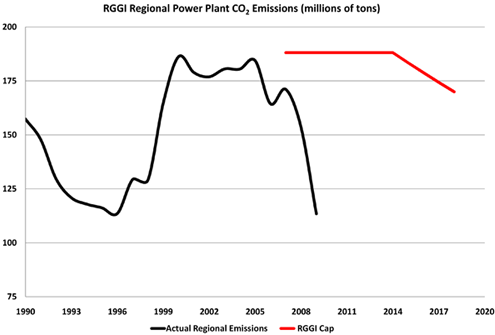

Emissions are capped from 2012 to 2014, and then, starting in 2015, the cap decreases 2.5 percent per year until it is down by 10 percent in 2019. This would represent a level of emissions 13 percent below the 1990 level of emissions. It was originally thought that this would be some 35 percent below the Business-as-Usual (BAU) level in 2019. Sounds good. What happened is not that the system performed other than designed, but that "business was not as usual." That is, what happened is that unregulated power-sector (BAU) emissions in the northeast fell significantly. (See the graph below of the RGGI cap and historical emissions.)

So, Why Did Emissions Fall in the RGGI States?

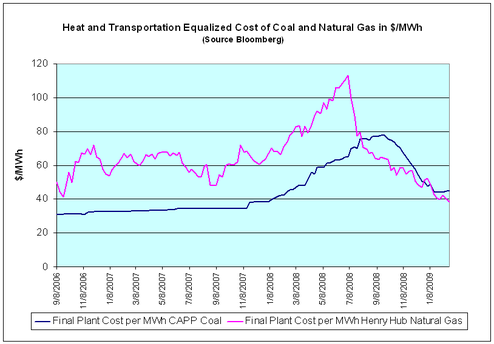

This happened for three reasons. First, because of increasing supplies in the United States of low-cost, unconventional sources of natural gas, prices for this fuel have fallen dramatically since 2008. (See the graph below of natural gas and coal prices.) That has meant greater dispatch of electricity from gas-fueled power plants (relative to coal-fired plants), more investment in new gas-fired generating plants, less investment in coal-fired generating capacity, and retirement of existing coal-fired capacity, all of which has contributed to lower CO emissions.

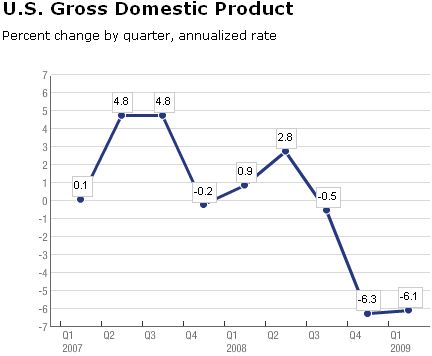

Second, the worst economic recession since the Great Depression hit the United States in 2008, causing dramatic reductions in electricity demand in the industrial and commercial sectors, reducing emissions. (See the graph below of quarterly percentage change in U.S. GDP, 2007–2009.)

Third and finally, moderate northeast temperatures have kept down CO emissions linked with both heating and cooling.

Low Emissions, Low Allowance Demand, Low Allowance Prices

So, for the three reasons above, BAU CO emissions from the power sector in the RGGI states are dramatically below what was originally (and quite reasonably) anticipated. The supply of RGGI CO allowances made available at auction is -- by law -- unchanged, but demand for these allowances has fallen dramatically, hence the fall in RGGI allowance prices. (See the graph below of RGGI allowance prices, 2008–2010.)

Given that emissions are below the RGGI cap and -- due to expectations regarding future natural gas prices -- are likely to remain below the cap, there is no scarcity of allowances. Shouldn't the price fall to zero? In theory, yes, except that the system has an auction reservation price of $1.86 per ton built in, thereby creating a price floor of precisely this amount.

Is RGGI a Failure?

So, the cap put in place by the RGGI system is being achieved, but it is not binding. RGGI may not be particularly relevant, but it is not thereby a flawed system; surely it is not a failure. Rather, a great environmental success has been achieved by the "fortunate coincidence" of low natural gas prices, economic recession, and mild weather. This is hardly something to be lamented.

True enough, the RGGI system does have flaws (such as its narrow scope limited to electricity generation, and its lack of a simple safety valve, as I have written about in the past). But the low allowance prices are evidence of a success outside of the RGGI market, not evidence of failure within the RGGI market.

If the RGGI states have the desire and the political will to tighten the cap in the future, then the system can again become binding, environmentally relevant, and cost-effective. That's an ongoing political debate.

To be fair, I should note that the same outcome I have described here can be spun -- perhaps for political purposes -- quite differently. Recently, a self-described "free-market energy blog" commentator claimed -- not without some justification -- that RGGI is irrelevant or worse: "Bottom line, the program has raised electricity prices, created a slush fund for each of the member states, and has had virtually no impact on emissions or on global climate change."

Phrased differently, due to exogenous circumstances (I've described above), the RGGI program is non-binding, and so has no direct effect on emissions, but its relatively low auction reservation price does lead to very small impacts on electricity prices, and produces revenues for participating states, revenues which those states would surely claim are of value for state-level energy-efficiency and other programs that indirectly do affect CO emissions. So, the real bottom line is that low RGGI allowance prices are not a consequence of poor system design or a fatal flaw of cap-and-trade systems in general, but rather a consequence of what are in reality some exogenous coincidences that have turned out to be good news for the environment.

Now, let's turn to the European Union Emissions Trading Scheme (EU ETS).

EU ETS Allowance Prices

Unlike RGGI, the EU ETS has not been irrelevant. It has successfully capped European CO emissions, achieved significant emissions reductions, and it has done so -- more or less -- cost-effectively. (More about this hedging on cost-effectiveness below). Not surprisingly, like RGGI, the EU ETS has some design flaws (principally, its limited scope -- electricity generation and large-scale manufacturing -- and lack of a safety-valve), but as with RGGI, its low allowance prices should not be taken as bad news, but to some degree as good news, and certainly not as a sign of failure of the EU ETS.

Hand-wringing in Europe Over Low Allowance Prices

There has been much hand-wringing in Europe over the "failure of the system" because of low allowance prices. Indeed, Danish Energy Minister Martin Lidegaard said earlier this month that low carbon prices threaten the EU ETS.

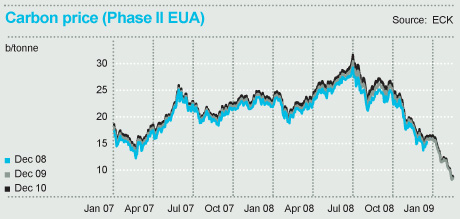

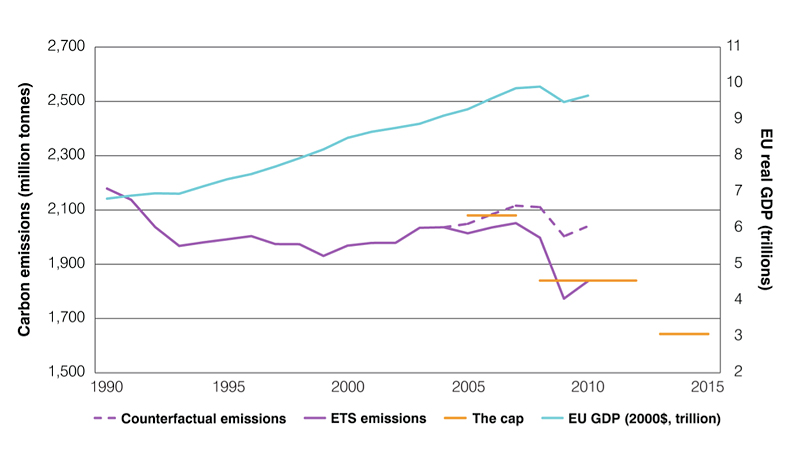

Of course, he's correct that EU ETS allowance prices are "low." They are down from their historic average of about $20 per ton of CO to about $9 per ton currently (having reached an all-time low of $7.88 in early April). Here's a graph of EU ETS allowance prices (EUAs) over the crucial period of change, January 2007 to January 2009.

At this point in this essay, I probably don't need to say that this pattern is partly explained by the global recession, which has hit Europe particularly hard (and now threatens a double-dip recession in a number of European nations). Lower European -- and global -- demand has meant decreased economic activity in Europe, hence lower energy demand, lower CO emissions, and therefore lower demand and lower prices for EU ETS allowances.

Even if we assume a growth rate of European CO emissions 1 percent less than the growth rate of GDP (represented by the dotted "counterfactual" BAU line in the graph below, which estimates what emissions would have been from 2005 to 2010 without the introduction of the EU's Emissions Trading System), the evidence makes clear that the EU ETS has succeeded in reducing emissions significantly below what would be expected from the recession alone.

This is where an important caveat needs to be introduced. Also feeding into this allowance price depression has been a set of national and regional energy policies, such as those promoting use of renewables, which have served to reduce emissions, demand for allowances, and hence allowance prices (while rendering the overall CO program less cost-effective by ensuring that marginal abatement costs remain heterogeneous). So, to the degree that the low allowance prices are due to so-called complimentary policies, the low prices are bad news about public policy (in cost-effectiveness terms), not good news. But this refers to misguided complimentary policies (which fail to bring about any incremental emissions reductions -- under the cap-and-trade umbrella -- and drive up aggregate cost), not to any design flaw in the EU ETS itself.

Multiple Goals Typically Require Multiple Policy Instruments

No doubt, Minister Lidegaard is aware of the allowance price impacts of the recession, and I hope he's aware of the allowance price consequences of these other energy and environmental policies. The problem arises, however, because he sees the fundamental purpose of the EU ETS as somewhat broader than what I described at the beginning of this essay (namely, achieving emissions consistent with some cap, and doing so cost-effectively -- if the cap is binding). For him -- and many other European observers -- "the purpose of the ETS was to cap CO emissions in the E.U. and ensure clear economic incentives for investment in renewables." So, the hand-wringing is not about a failure to achieve emissions reductions cost-effectively, but to have prices high enough to achieve other goals -- in this case, greater use of renewable sources of energy. For others, the "other goals" have involved allowance prices high enough to bring about some targeted amount of technology innovation.

As I have written at this blog in the past, having multiple policy goals typically necessitates multiple policy instruments. For example, if the goal is a combination of reducing emissions cost-effectively and having prices maintained at some minimum (whether to bring about greater use of renewable energy sources or to inspire more technology innovation), then two policy instruments are needed to do the job: a cap-and-trade system for the first goal in combination with a carbon tax in the form of a price floor (as in RGGI) for the second goal.

Don't Throw Out the Baby With the Bath Water

In other words, the EU ETS has not failed, but the design was inadequate (that is, incomplete) for what politicians now seem to want. If the Europeans want a price floor in their system (or better yet, a price collar, which would combine a price floor with a safety valve, i.e., price ceiling), then this is certainly feasible technically and economically. Likewise, if the EU member states have the desire and the political will to tighten the cap in the future, there are a variety of ways in which they can accomplish this, rendering the program more stringent and increasing allowances prices. But, in any event, the European Commission's Energy division, Environment division, and Climate division should sort out the real effects of the "complimentary policies" that have contaminated the EU ETS, and which fail to bring about additional emissions reductions but drive up costs. Whether any of this is feasible politically is a question that my European colleagues and friends can best address.