On July 11, 2013, I predicted that the Dow Jones Industrial Average would hit 5,000 before it hit 20,000. Here is some of what I wrote a year ago:

The Fed has been keeping interest rates at rock bottom lows to supposedly stimulate the economy... The idea that the Fed can save the economy is simply ridiculous... What about fiscal policy? Can we deficit spend our way to prosperity? This is also ridiculous. Our problem is that we have overspent. If you had a problem of drinking 50 cups of coffee a day, would the solution be to drink 80 cups a day for a while? ...

Stocks will decline. I'm not predicting what will happen today, or in the next week or month. I don't pretend to know the timing. I only think that I see the inevitable.

One year later, we revisit the macroeconomic policies, the impact on jobs and profits, and check in on the Dow Jones Industrial Average. In addition, we develop a scorecard to revisit periodically as the government attempts to end the unusual macroeconomic policy environment.

Summary

In the last year, the Federal Reserve has continued an extremely loose monetary policy, and the U.S. federal government has added large amounts of debt. The stated goal of these policies is to stimulate the economy.

While macroeconomic policy remains extremely loose, any positive impact on the real economy has been modest. Over the last year, U.S. corporate profits and average real wages have declined. The good news is that there has been an increase in the total number of jobs and, consequently, in total wages.

While wages and profits have responded modestly, or not at all, to the extreme macroeconomic policy environment, the stock market has continued its powerful rise.

In short, Wall Street parties while Main Street struggles.

Macroeconomic Policy: Monetary and Fiscal throttles wide open.

We continue to live in an historic macroeconomic environment. All three of the main "stimulative" policies continue at near all-time high rates.

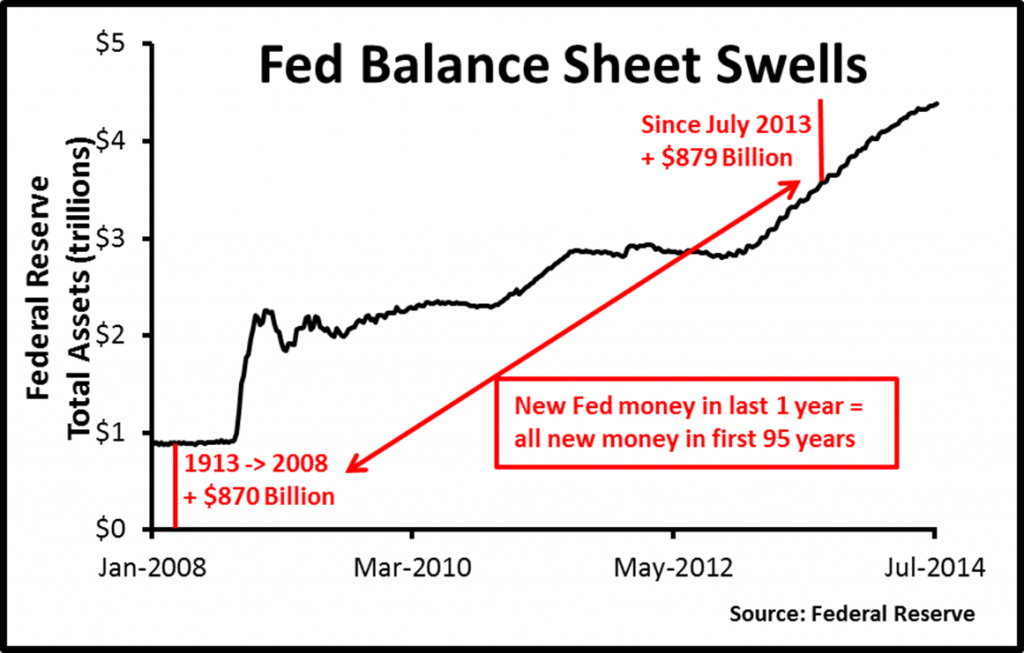

1. Quantitative Easing (QE). Under QE, the Federal Reserve buys bonds to stimulate the economy. If bond prices go up because of the Fed's purchases, mortgage rates go down, and more people might, for example, buy new homes. Since 2007, the Fed has purchased almost $4 trillion in new bonds. Over the past 12 months, the Fed has increased its balance sheet by 24.9 percent, by purchasing an additional $879 billion dollars of Treasury and mortgage bonds.

The increase of $879 billion in the last year is larger than the size of the Fed's balance sheet in 2007. In other words, it took the Fed almost a century to create as much money as it has in the last year.

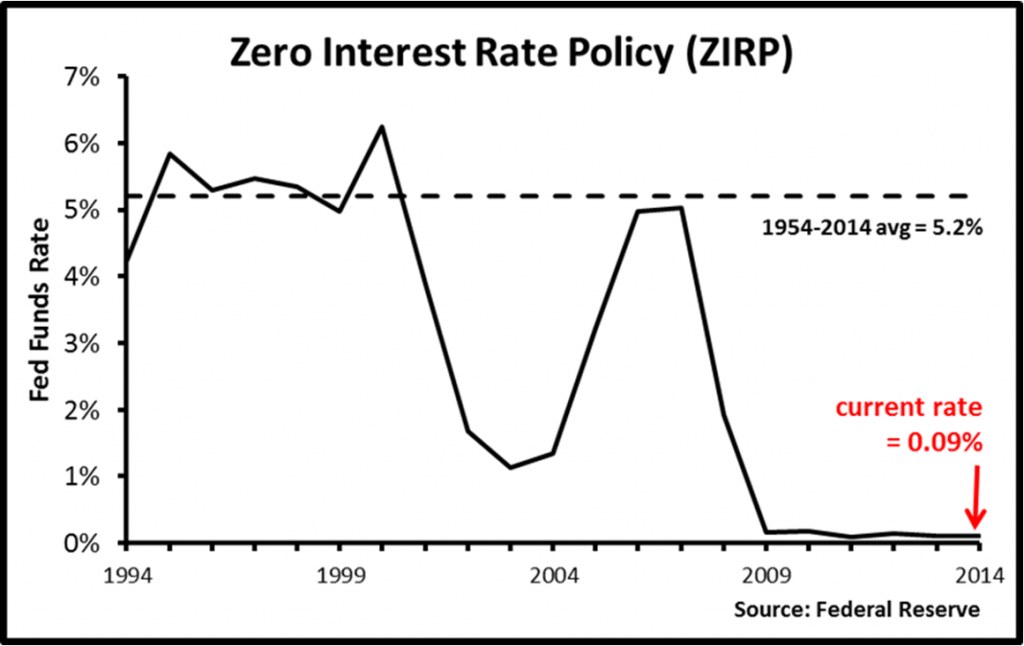

2. The Federal Reserve sets short-term interest rates. Since 2009, the Federal Reserve has followed a zero interest rate policy (ZIRP) by keeping rates at almost exactly zero (see chart). The Fed Funds rate today of 0.09 percent is exactly equal to the rate a year ago.

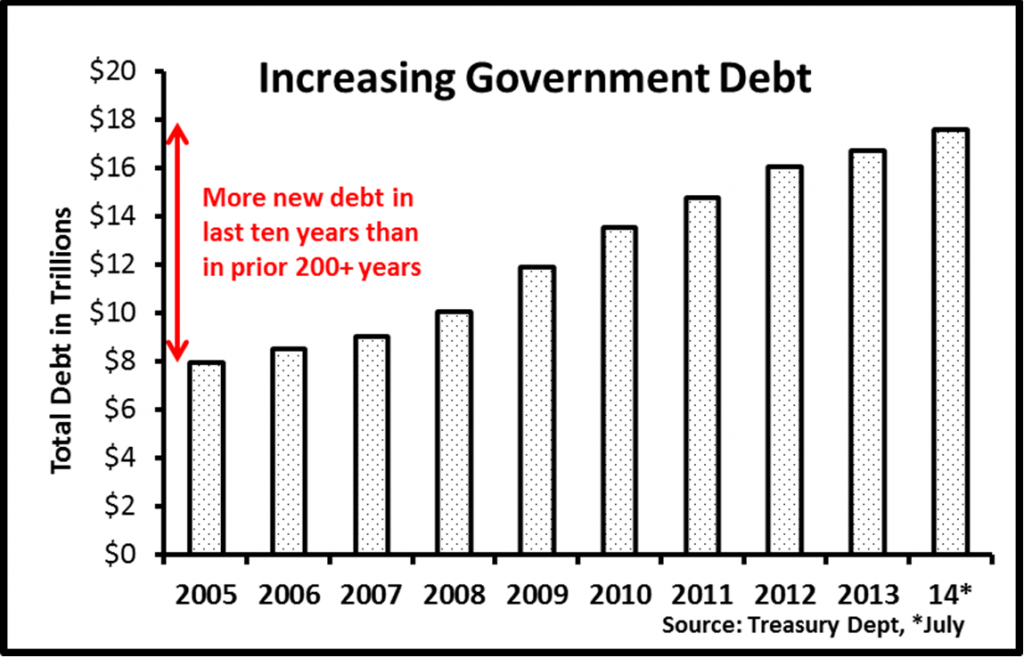

3. Federal Debt: In the last 12 months, total U.S. government debt has increased by $853 billion dollars. This increase in debt in the last year continues a government spending spree that has increased total government debt by almost $10 trillion in a decade; more in the last decade than in the entire prior history of the U.S.

The Federal Reserve and the U.S. government are continuing to run loose monetary and fiscal policy.

Sources are the Federal Reserve (Fed balance sheet); the Federal Reserve (Fed funds rate) and the Treasury Department (federal debt).

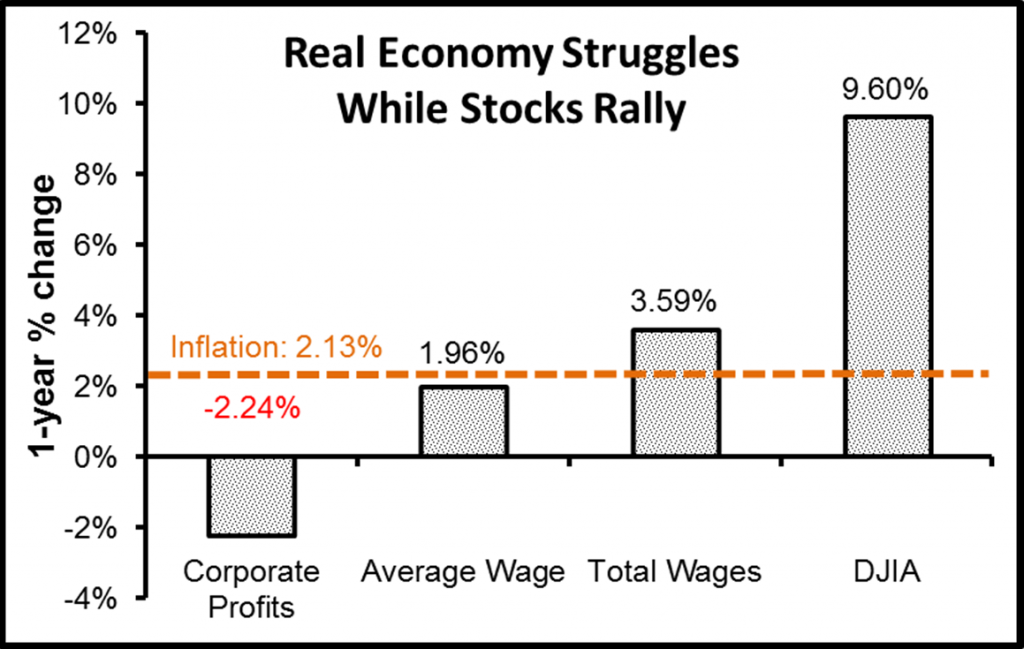

The Real Economy Struggles

While monetary and fiscal policy remain incredibly loose, the real economy sputters. Two of the most important measures of the real economy are corporate profits and wages. Profits are the return on invested capital, and wages are the payment for labor.

Over the last 12 months, total U.S. corporate profits declined by 2.2 percent. While this decline of 2.2 percent is the most comprehensive measure of all U.S. corporations, a different measure of profits is cited frequently. That is earnings per share for S&P 500 companies. The S&P 500 companies are among the largest companies, and they obtain about half their revenue from outside the U.S. Over the last year, the average earnings per share for the S&P 500 rose by 5.3 percent.

Total corporate profits and S&P 500 earnings per share diverged in the last year. The current economic environment favors powerful corporate entities such as Apple and Exxon over less powerful organizations such as a family-owned corporation. As a measure of the returns to work and investing, I favor using total corporate profits over narrower S&P 500-based-measures.

Wages

Over the past year, the average wage per hour rose from $23.98 to $24.45 per hour. However, this 1.96 percent rise in the average wage failed to keep up with the inflation rate of 2.13 percent over the same period. So the average real wage has fallen over the last year.

The good news is that there are now 2.5 million more jobs than a year ago. Even though real wages per hour have declined, total wages and salary increased by 3.59 percent.

We can estimate the cost of each of these new jobs. If all of the 2.5 million jobs were created by monetary and fiscal policy, then each job cost $690,000. If only some of the jobs were created by these macroeconomic policies, then the cost per job was higher. For example, if half the 2.5 million additional jobs were created by these macroeconomic policies, then the cost per job was $1.38 million.

The economy continues to struggle. Over the last year, the number of jobs increased, while average real wages and corporate profits declined.

Sources are the Bureau of Labor Statistics (non-farm payrolls); Bureau of Labor Statistics (hourly earnings); Bureau of Economic Analysis (wages and salaries); Bureau of Economic Analysis (corporate profits); Bureau of Labor Statistics (CPI).

The Stock Market Parties Like It's 1999

Over the last year, the Dow Jones Industrial Average has risen 9.6 percent.

The rise in the stock market has been relentless. There were 52 all-time closing highs for the Dow in 2013, and 13 new all-time closing highs so far in 2014. On July 3, 2014, the Dow Jones Industrial Average closed above 17,000 for the first time in history, up more than 10,000 points from its low of 6,547 in March 2009.

The stock market continues its historic bull market.

Looking Forward

We are living through the greatest macroeconomic experiment in the history of the U.S. Never was so much printed and spent by so few.

In future articles, I will use the same economic scorecard to assess the following:

- Macroeconomic Policy

Quantitative Easing: Change in the size of the Fed's balance sheet

Zero Interest Rate Policy: The fed funds rate

Deficit: Total U.S. government debt

Corporate profits

Average real wages

Total real wages

Over the past year, this scorecard shows a divergence with the real economy struggling while the stock market powers ahead. This divergence is not likely to persist indefinitely. I continue to believe that the Dow will see 5,000 before it sees 20,000.

Terry Burnham is a regular contributor to Making Sen$e with Paul Solman at the PBS NewsHour Online, where this post originally appeared.

Catch up on past articles by Terry: