Rather than invest profits in building a strong economy, corporate executives invest in their own pay.

Occupy Wall Street is keeping our focus on the insatiable greed and undemocratic influence of those who run our major financial institutions. But the quest for personal wealth and political power by the top executives of U.S. business corporations goes well beyond the Wall Street banks. It pervades industrial as well as financial corporations.

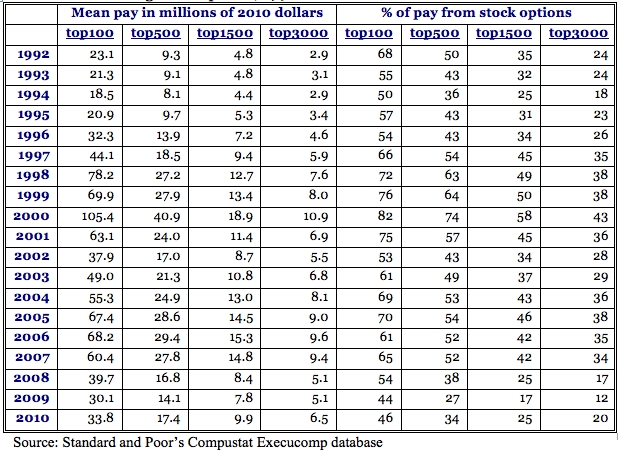

Even though, as Table 1 shows, the pay of top corporate executives is down from its pre-financial-crisis levels, it remains out of control. The average remuneration of the top 100 highest paid corporate executives (named in annual proxy statements) was $33.8 million in 2010, up 10 percent from a 2009 average of $30.1 million (in 2010 dollars). Since the financial meltdown, executive pay has remained far higher than it was in the early 1990s, when it was already viewed as extraordinarily excessive.

Table 1. Mean pay of the highest paid corporate executives and percent of pay from exercising stock options, 1992-2010

As can be seen in Table 1, much, and in many years most, of this exorbitant pay comes from the exercise of stock options. The gains from stock options depend on rising stock prices. What better way for corporate executives to give a manipulative boost to a company's stock price than to spend hundreds of millions, or even billions, of dollars buying back its stock.

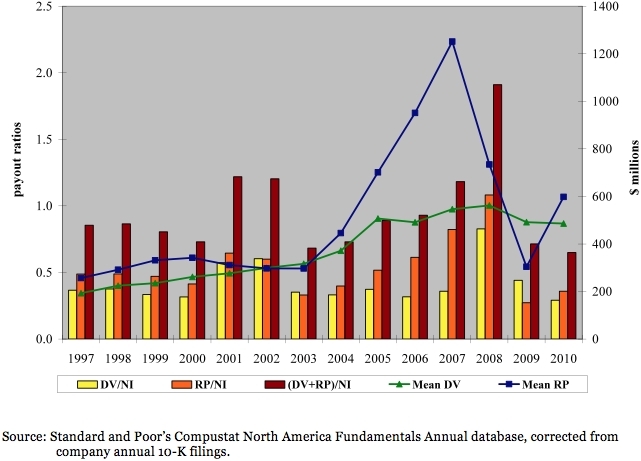

As Figure 1 shows, in 2003 buybacks were already substantial among S&P 500 companies, with an average of $300 million. But over the next four years, that amount quadrupled, so that on the eve of the financial crisis these companies averaged over $1.2 billion in buybacks. During the financial crisis, they dropped back down to about $300 million per company, but in 2010 doubled to around $600 million. In 2011, buybacks of S&P 500 companies are on pace to hit an average of $900 million, and there is every indication that they will continue to escalate in 2012 and beyond, as happened in 2003-2007. For overpaid U.S. corporate executives, this form of stock-price manipulation has become an addiction.

Figure 1. Repurchases (RP) and dividends (DV), 1997-2010, of 419 companies in the S&P 500 Index in January 2011 that were publicly listed back to 1997; mean distributions and proportions of net income (NI)

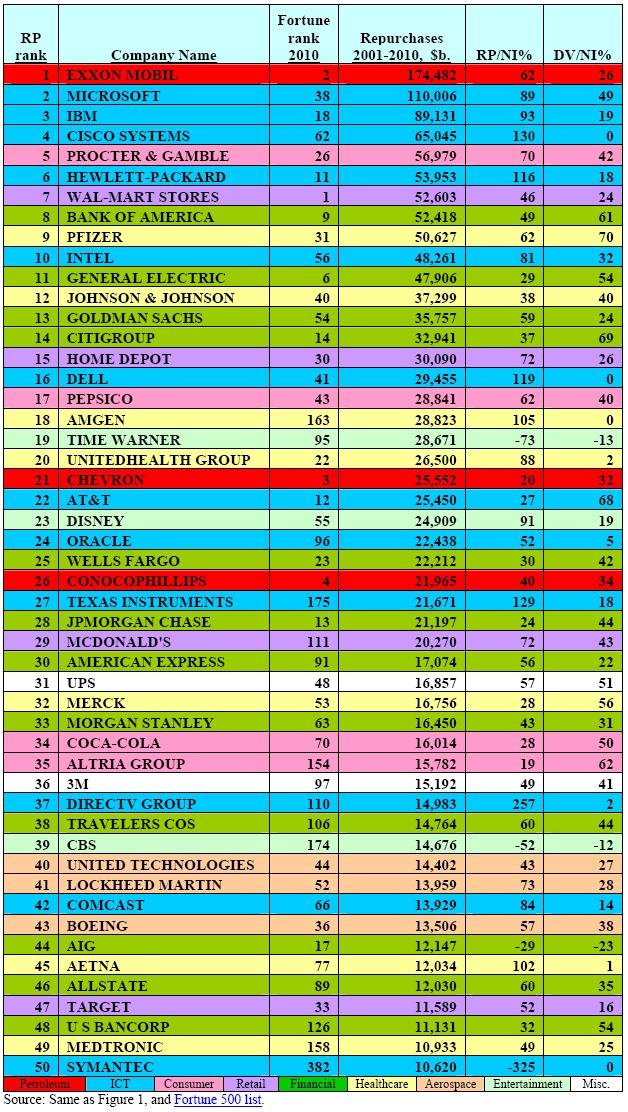

As shown in Table 2, the top 50 repurchasers for the decade 2001-2010 represent a range of industries. Combined, over the decade they spent more than $1.5 trillion repurchasing their own stock.

Of these 50 companies, 11 spent more than 100 percent of their net income over the decade on buybacks, 32 more than 50 percent, and 43 spent 30 percent or more. When dividends are added to buybacks, half of these 50 companies expended all of their profits and more in distributions to shareholders from 2001 through 2010.

Table 2. Top 50 stock repurchasers among U.S. corporations, 2001-2010

Research on these various industries and companies has revealed the deleterious impacts of stock repurchases on economic performance. For example, over the decade 11 of the 12 ICT companies on this list spent more on buybacks than on R&D, while for the twelfth, Intel, the proportion was 93 percent. Most of the financial services companies on the list had to be bailed out by the federal government in 2008-2009. Led by Exxon Mobil, the three petroleum refining companies in the top 50 wasted a combined $222 billion on buybacks while charging high oil prices and neglecting substantial investments in alternative energy. For the three aerospace companies, defense contracting generates much of the profits that they then use to manipulate their stock prices through buybacks. Pharmaceutical companies charge drug prices that are twice as high in the United States as in the rest of the world, yet use much or all of their profits for buybacks. Health insurers use their profits to jack up their stock prices, and executive pay, while giving us high cost, low quality health coverage.

Executives like to say that buybacks are financial investments that signal confidence in the future of their company as measured by its stock price performance. In fact, however, companies that do buybacks never sell the shares at higher prices to cash in on these investments. To do so would be to signal to the market that their stock prices have peaked, something that no executive would ever do. Executives often say that they do buybacks because of a lack of more attractive investment opportunities. Yet we live in a world of rapidly changing technology, burgeoning new product markets, and intense global competition. Any CEO of a major U.S. corporation who says that buybacks are the best investments that his or her company can make should take the next logical step: fire him or herself!

William Lazonick is director of the UMass Center for Industrial Competitiveness and president of The Academic-Industry Research Network. His book, Sustainable Prosperity in the New Economy? Business Organization and High-Tech Employment in the United States (Upjohn Institute 2009) was awarded the 2010 Schumpeter Prize.

Cross-posted from New Deal 2.0