If you are a recent graduate, you've probably noticed the many ads on your Facebook feed from new student loan lenders urging you to refinance your loans with them. These lenders are mostly targeting early career professionals with stable income and good credit, which explains why the ads are showing up on your feed. As an employee of a bank offering a national student loan refinance and consolidation program, I often speak with recent graduates looking for guidance on questions regarding their student loans. So, for those of you who still don't fully understand how student loan refinancing works, let me help you out.

What Factors Should I Think About When Considering Refinancing My Student Loans?

The first question to consider is whether you should keep your federal loans (for almost all of you, federal loans constitute a majority of your student loans) or refinance them to private loans. Federal loans come with a variety or protections and benefits. For example, federal loans give you the ability to defer payments or go on forbearance when you are experiencing financial hardship. Federal loans also allow many borrowers to adjust payments down based on income. Finally, some borrowers can have their federal loans forgiven in certain circumstances. You can find out about these programs on the Federal Loan website. Why would someone give up these federal loan benefits? The simple answer is that refinancing to a private loan could save you a lot of money. If that tradeoff sounds compelling to you, keep reading.

The most important factors to consider in private loan refinancing are interest rate, repayment term (length of the loan), and type of loan (fixed rate or variable rate). These factors will impact how much you can save by refinancing and how much you have to pay each month. All things being equal, you want the interest rate to be as low as possible. However, the lowest rates are typically only available for the shorter repayment terms, and shorter repayment terms lead to higher monthly payments, since you are paying your loan back over a shorter period of time. As such, you will sometimes need to balance lower rates with shorter terms and higher monthly payments.

After you decide on a term, the other major factor is whether a loan is fixed or variable. While a fixed rate stays constant over the life of a loan, the variable rate option offers lower initial rates. However, these rates can fluctuate as interest rates change, which are hard to predict. Variable rate loans are good for people who believe they will make enough money in the future to cover potentially higher payments if rates go up, but may not be good for people whose future income is not as predictable.

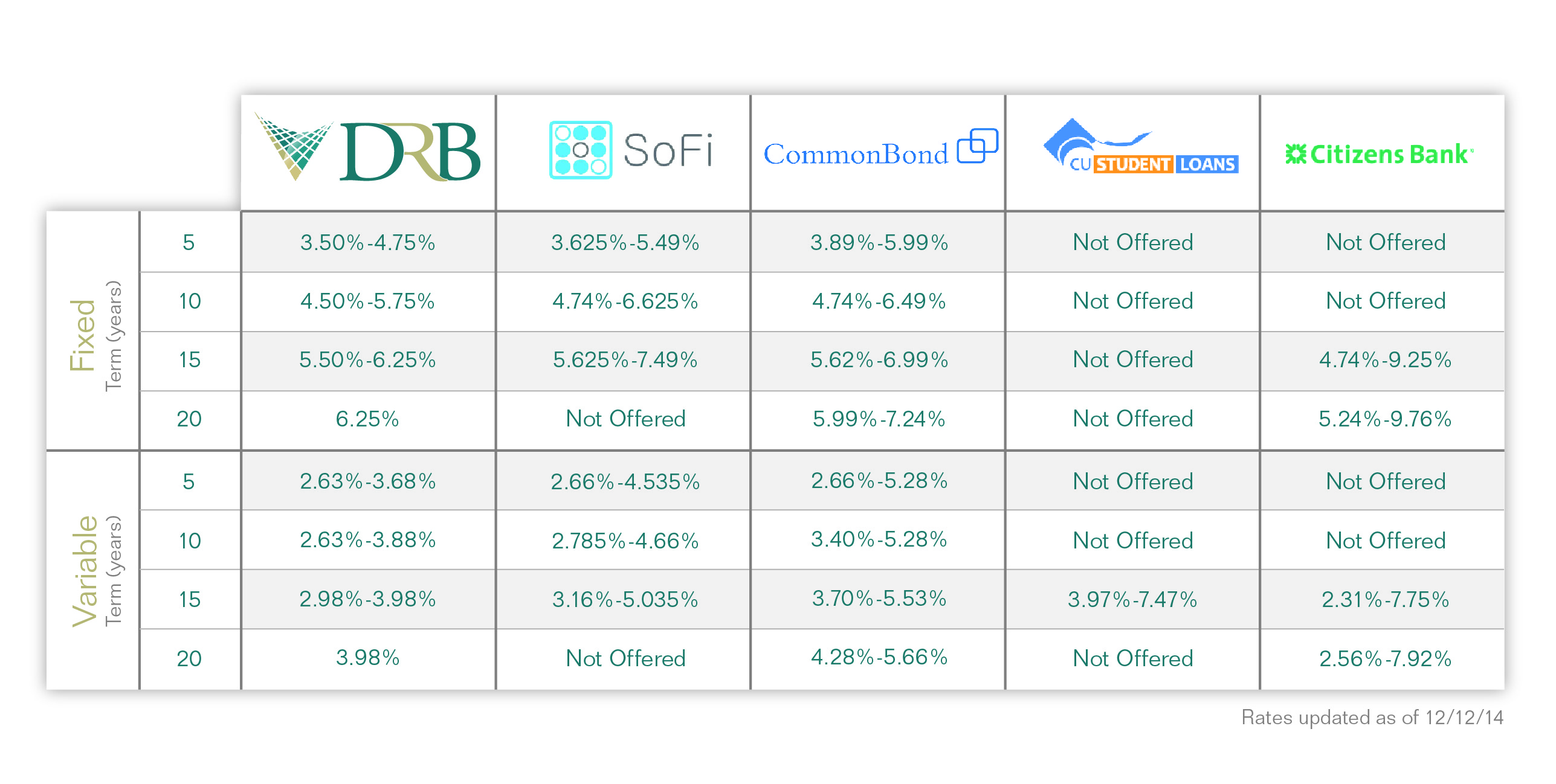

Below, we have broken down how some of the top student loan refinance lenders compare across these metrics. One note of warning, there are a lot of numbers on this chart. It may seem intimidating at first, but it is studying closely, as picking the right loan can help you save a lot of money.

You may be curious how banks decide what rate to give you. (I know you are, since I get this question about 500 times a day). Although it varies, lenders typically look at a borrower's credit history, income and debt to arrive at the rate they will offer a specific borrower (lenders stopped using Magic 8 Balls in the 1990's). The best way to ensure you are getting the lowest rate is to 1) Make sure there are no mistakes on your credit report (e.g., if you have any false late student loan payments on your report, make sure those are removed by calling the top Credit Bureaus), 2) Include all forms of income in your application, and 3) Pay down your revolving debt as much as possible. For some lenders, applying with a cosigner can also help.

If this is so simple, why is it so complicated?

While the chart above breaks out the key factors for you to consider, it does not tell the whole story. For example, did you know that some of these lenders are banks and some are not? A couple of these lenders are peer-to-peer lenders. Peer-to-peer lending means exactly what it sounds like: borrowers receive funding from peer lenders, or actual people who provide capital. These peer-to-peer lenders will often match alumni with borrowers from the same school. Another non-bank lender has formed a network of credit unions to make loans to borrowers on one platform. Depending on the person, the evolution of these student lending platforms is either completely fascinating or deathly boring. My recommendation to people looking to refinance is to focus on rate and term and less on these lending models, since at the end of the day, rate and term is what will affect your bottom line the most.

Some of these lenders also offer other programs such as community building and job placement help. I am a bit skeptical of these offerings. Most of our borrowers come from schools that have made considerable investments in building vibrant alumni communities. It's difficult to believe that lenders will be able to build school-based communities in a better way than the schools have. Regarding job placement, we recommend that any borrower who is concerned about losing their job not refinance with a private lender and keep their federal loans and the protections that come with them. These protections are much more valuable than any job coaching that a lender could provide in the event you lose your job.

Quick Summary

In short, here is what we recommend to graduates with high rate student loans: Decide if it makes sense for you to give up the benefits of federal loans in exchange for lower rates. If it does, take a look at the lenders in the chart above and see what rates they will offer you. Pick the lender with the lowest rate and with a term and monthly payment that makes sense for your situation. There is potential to save thousands of dollars by making the right decision, so we suggest you do your homework and research these lenders.

Aryea Aranoff and Jessica Kahkoska work on the marketing and strategy team at Darien Rowayton Bank, an FDIC insured bank offering a low rate student refinancing loan to working professionals who recently completed their education. DRB is a market leader in this space, offering some of the lowest rates in the country on its student loans.