An innovative methodology to measure the positive environmental benefits, including a net reduction in carbon dioxide, for an investment strategy provides a meaningful new tool for investors.

Impact Investing Options

Investors choose funds for many different reasons. Some seek growth, others income. Some investors opt for low cost index tracking funds while many are looking for diversification strategies that demonstrate low correlation with other investments in their portfolios.

In recent years we have seen another significant driver emerge as many individuals, endowments and pension funds increasingly seek to align their investments with their values and mission. With concerns about climate change and related investment risks becoming better understood and more widespread among investors, managers and advisors are frequently asked about the environmental impact of investment strategies.

Many asset classes (such as infrastructure, venture capital and debt) now commonly use positive impact metrics. However, listed equity products have been slow to adopt a more sophisticated positive approach and typically look at only negative risks; often with overly simplistic or qualitative techniques including carbon foot-printing. So we set out to change this and to measure not just the negatives but to bring the language and quantitative evidence of positive impact metrics to a listed equity fund.

Maximizing Returns and Positive Impact

The primary objective of Impax's [small/mid cap] "Specialists" strategy is to maximize financial returns within a universe of pure play - or specialist - companies active in the resource optimization and environmental markets. These markets include energy efficiency, renewable energy, water, resource recovery, food, agriculture and forestry. While we own shares in these companies for their long term growth potential, we always assumed their commercial activities had a positive environmental impact.

However, reasonable assumptions need to be tested. Accordingly, we established a process, underpinned by a rigorous methodology that has been independently verified by EY, to assess the net environmental impact of each holding at the company level, and then attributed a portion to the portfolio based on our percentage equity ownership.

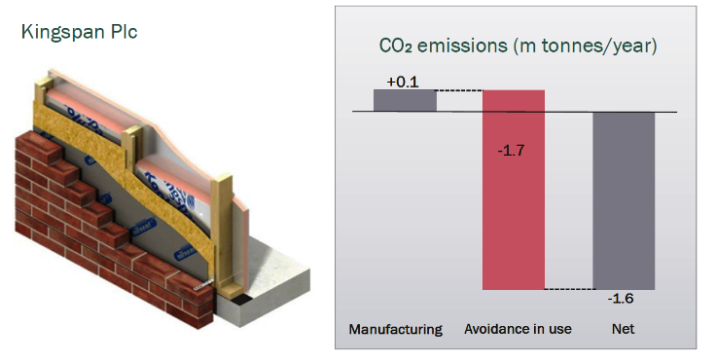

By way of example, let's consider the environmental impact of Kingspan, a global leader in high performance insulation and building fabrics delivering energy efficiency solutions across a broad range of sectors. The following data refers to the company's activities in 2013:

Kingspan's high efficiency building materials reduce energy consumption significantly. However, the manufacturing process produces emissions of 0.1m metric tonnes of CO2 per year. This carbon footprint would eliminate Kingspan from many 'Low Carbon' strategies. But the lifespan of the installed material is many years, and the energy saved over this period more than offsets the carbon emissions of the manufacturing process, resulting in 1.6m metric tonnes net avoided CO2 emissions.

At the end of 2013, Impax's strategy owned 1.4% of Kingspan's shares. In our portfolio calculation we attribute a corresponding amount of CO2 reductions to the strategy. (In this case 22,500 net metric tonnes; 1.4% of the 1.6 million net tonnes of CO2 emissions avoided through the use of Kingspan's products).

Applying that methodology to the entire portfolio reveals that over the last year its holdings have avoided 1,101,000 metric tonnes of CO2 - which is equivalent to taking 494,000 cars off the road.

In addition, we have been able to estimate that every $1 million invested in the strategy over the period has delivered:

-900 metric tonnes net negative carbon emissions, equivalent to taking ~400 cars off the road1

-700 MWh of renewable electricity generated, enough for over 100 average households

-79 million gallons of water treated, enough for over 1000 households

-650 metric tonnes of waste recycled and treated, approximately that of over 400 households.

Many strategies today have had a strong positive intention regarding environmental impacts built into their investment process. By adding quantitative metrics to the investment reporting process we can offer investors a much clearer understanding of the positive environmental outcomes of their allocation; a process that the larger industry would benefit from adopting.

Investment advisors and discretionary managers can use these additional reporting metrics to help clients seeking to decarbonise their portfolios, offset high emissions in alternative strategies, or simply to improve their understanding of the extent of the positive outcomes of their investment decision. We would encourage other managers to offer similar metrics so that investors are better able to evaluate the true impact of their equity investments.