Back in August, we explained in our blog the mechanics of how the Fed can tighten policy in today's world of abundant bank reserves. Now that the first policy tightening under the new framework is behind us, we can review how the Fed did it, if there were any surprises, and what trials still lie ahead.

So far, the new process has been extraordinarily smooth - a tribute to planning by the Federal Open Market Committee (FOMC) and to years of testing by the Market Desk of the Federal Reserve Bank of New York (FRBNY). But it's still very early in the game, so uncertainties and challenges surely remain.

On December 16, the FOMC announced an increase in the target range for the federal funds rate (with effect on December 17) from the 0.00%--0 .25% range that prevailed since December 2008 to the new range of 0.25%--0.50%. In contrast to past instances of policy tightening (the most recent was June 2006), the FOMC did not instruct the FRBNY Market Desk to seek "conditions in reserve markets consistent with increasing the federal funds rate" to the new target. Quite the contrary: the Committee directed the Desk to "continue rolling over maturing Treasury securities at auction and to continue reinvesting principal payments on all agency debt and agency mortgage-backed securities in agency mortgage-backed securities."

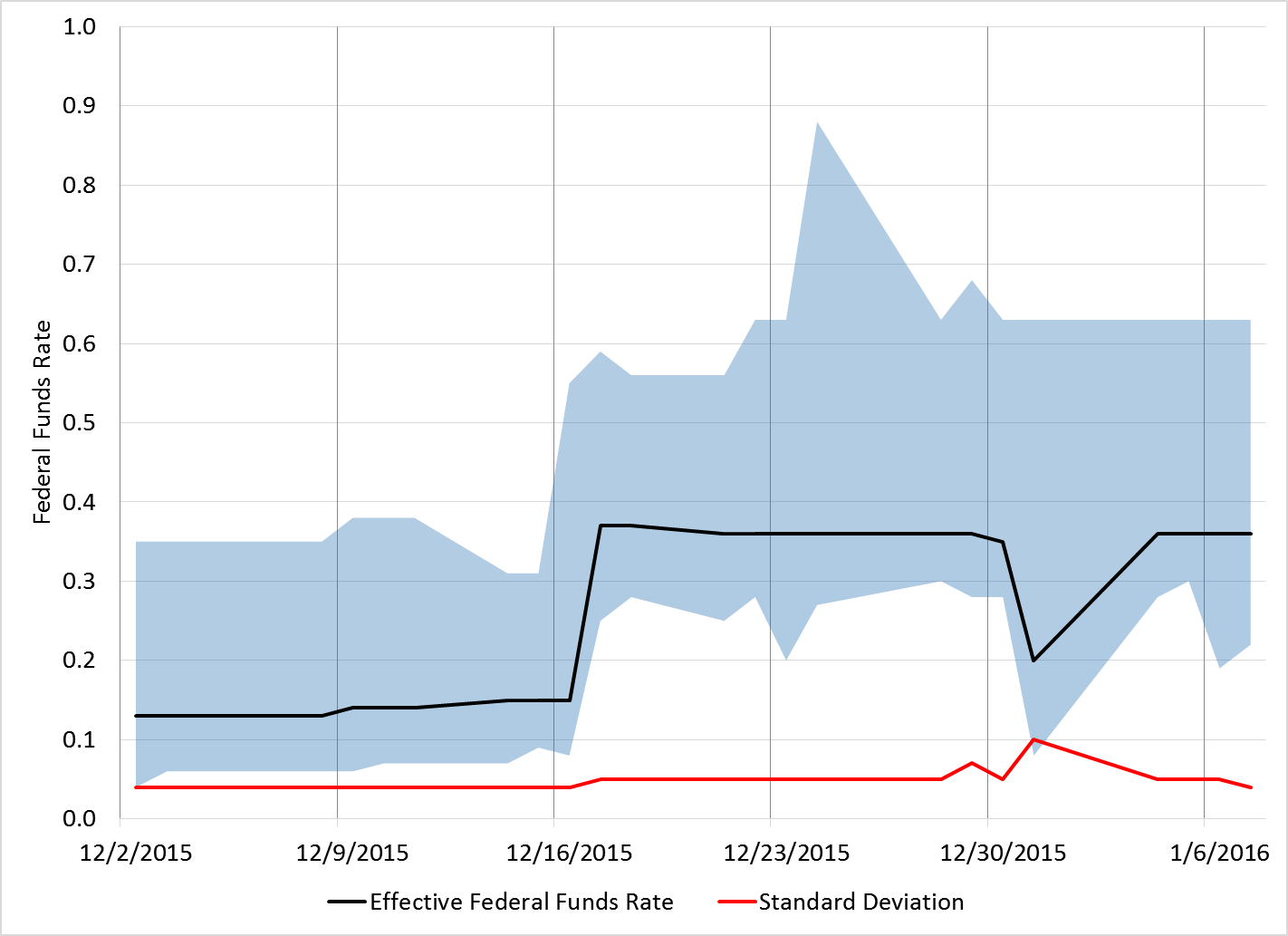

The new environment notwithstanding, the Desk hit the higher target range immediately and accurately. First, the effective federal funds rate--the volume-weighted rate on all transactions in the market for bank reserves (their deposits at the Fed)--rose from 0.15% on December 16 to 0.37% on December 17 and remained within 1 basis point of this rate for the following week (see the chart below). Second, the standard deviation of the rates on all transactions in the federal funds market remained at 0.05%. Consistent with this narrow dispersion and the target-consistent rise in the effective federal funds rate, the range between the minimum and maximum rates on transactions (depicted by the blue shaded area in the chart) rose by an amount comparable to the 25-basis-point increase in the target range (aside from temporary year-end effects).

Federal Funds Rate, daily effective rate, high, low and standard deviation

Notes: The blue shaded area represents the range between the lowest and highest interest rate on any transaction in the federal funds market each day. Temporary extreme observations of the federal funds rate are commonly associated with end-of-year effects and with the end of biweekly reserve maintenance periods. Source: FRBNY.

So, what precisely did the Fed do?

The primary tool for tightening financial conditions in the new policy framework is the interest rate paid on excess reserves (the IOER rate). The Fed (through a Board vote to implement the FOMC decision) raised the IOER rate from 0.25%, where it had remained since mid-December 2008, to 0.50%, the top of the new target range for the federal funds rate. Raising the IOER rate boosts the market federal funds rate for two reasons: first, because deposits at the Fed are free of both default and liquidity risk, banks will not lend to other banks in the overnight uncollateralized market at an interest rate below the IOER rate. Second, a higher IOER rate induces banks to bid more aggressively for overnight, uncollateralized funds from nonbanks, which cannot hold interest-bearing accounts at the Fed. Because banks can borrow these funds and deposit them without risk at the IOER rate, they are willing to bid for these funds up to the IOER rate less any cost of expanding their balance sheet. The observed gap between the IOER rate of 0.50% and the effective funds rate of 0.36% is a measure of these unobserved costs, which may include the FDIC insurance fee that some banks pay on borrowed funds as well as the marginal cost of holding more assets that might result from bank regulation (such as the leverage ratio).

In contrast to the world of scarce reserves that prevailed prior to the failure of Lehman Brothers in September 2008, today the typical lender in the federal funds market is not a bank. Instead, nonbanks, specifically the government-sponsored enterprises (GSEs) like Fannie Mae, Freddie Mac and the Federal Home Loan Banks (FHLBs), are the ones making most of the loans. The recipients also have changed. While all banks can bid for these funds and deposit them at the Fed to receive the IOER rate, some potential borrowers face lower costs than others, so they can afford to bid a higher rate for loans from nonbanks. For example, foreign bank offices are not required to pay the FDIC insurance assessment (which can range from 5 basis points to 35 basis points for large institutions), so--unsurprisingly--their balances at the Fed were $881 billion as of mid-2015 (the latest report available), or more than one third of both their total assets and of all banks' reserves.

Why might the maximum rate in the federal funds market exceed the IOER rate, as it did in the first week of tightening? Even in this world of abundant excess bank reserves--there are currently $2.42 trillion, or roughly 1,500 times the typical level prior to Lehman's failure--a particular bank may unexpectedly fall short of its required reserve holdings, compelling it to bid aggressively for overnight funds. The Fed's discount rate, the rate at which the central bank stands ready to lend elastically to banks with adequate collateral, normally caps the rate that banks bid for reserves. However, on December 16, accepting the requests of the Reserve Banks, the Federal Reserve Board raised the discount rate rose by 25 basis points, from 0.75% to 1.00%. This is well above the maximum transaction rate in the federal funds market of 0.63% in the week after the FOMC raised the target range.

Perhaps the most interesting aspect of the Fed's new policy mechanics is how they are seeking to control the bottom of the target range for the federal funds rate. Suppose, contrary to fact, that the regulatory and insurance costs of expanding banks' balance sheets were so high that banks were only willing to bid the IOER rate minus 30 basis points for funds from nonbanks. As a consequence, and in the absence of other policy tools, the effective federal funds rate would likely fall below the bottom end of the 25-basis-point range set by the FOMC, causing the Market Desk to miss the target.

However, over the past few years, the Fed tested a tool that allows it to absorb overnight funds directly from nonbanks--namely, the overnight reverse repurchase agreement (ON RRP). In addition to 22 primary dealers (listed here), the Fed has approved more than 140 nonbank counterparties (listed here) with whom it can conduct reverse repo. Since ON RRPs are a default-risk and liquidity-risk free loan to the Fed, offering to accept these funds in sufficient volume sets a floor below the rate at which this broad array of short-term market participants is willing to lend to a bank.

Accordingly, together with its December 16 statement, the FOMC issued an "Implementation Note" specifying that ON RRPs would be offered at 0.25%--the bottom end of the target range for the federal funds rate--"in amounts limited only by the value of Treasury securities held outright in the System Open Market Account (SOMA) and by a per-counterparty limit of $30 billion per day." As of December 16, SOMA holdings of Treasury instruments totaled $2.45 trillion--a bit less than one half of the limit that would apply if every potential counterparty offered its full ON RRP quota of $30 billion, but slightly larger than the banks' excess reserves.

While the ON RRP mechanism sets a floor under the vast majority of market federal funds rate transactions, there will be occasional trades at a lower rate--as there were on December 23 (see the table above). Since ON RRP operations are done at 1:15pm, there is always the possibility that later in the afternoon a nonbank with excess funds will have no option but to lend at the rate the market will bear. Knowing the lender has no other options that day, banks will be able to bid below the ON RRP rate.

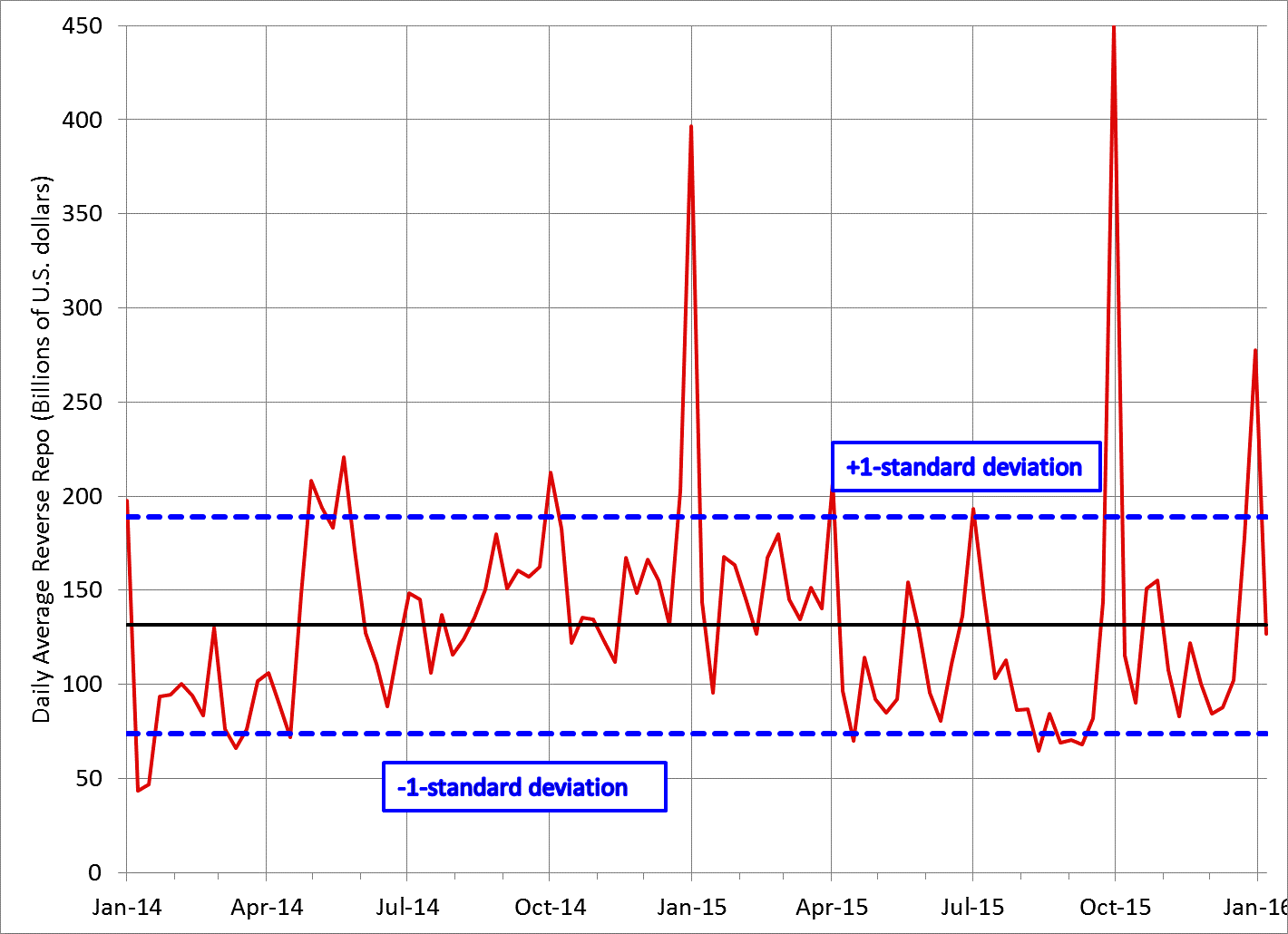

The real news associated with Fed tightening--at least to those of us who care about the policy mechanics--is that the Fed didn't need to accept a large volume of ON RRP funds to keep the effective federal funds rate above the bottom of the target range. In fact, for the week ended December 23, reverse repo (excluding foreign official and international accounts) averaged $178 billion a day. While the volume jumped in the final week of 2015 to $277 billion, this looks to be a year-end anomaly (smaller than the jump at the end of 2014) as the level immediately plunged back below $150 billion during the first week of 2016 (see chart). What this means is that banks' bids for overnight uncollateralized funds from nonbanks were sufficiently strong to raise the effective funds rate without the Fed absorbing much of these nonbank funds directly.

Federal Reserve: Daily average reverse repo excluding foreign official and international accounts (U.S. dollars in billions, weekly data ending Wednesdays), Jan 2014-Jan 6, 2016

Source: FRED.

So, will the Fed's first-week success continue? Our guess is that it probably will, but we can't rule out a few hazards. For example, it is possible that nonbank lenders are still learning about the new regime and will shift toward the ON RRP market and away from loans to banks as they see how the system works. Were that to happen, ON RRPs would expand and bank reserves shrink. And, if the shift were to be so extraordinarily large that the Fed would be unwilling or unable to accommodate the increased demand in ON RRP, the effective funds rate would then slip below the target range. Similarly, as the Fed moves to tighten further over coming months and years, MMMF accounts may attract savers away from bank deposits, raising the possibility of rising demand for ON RRPs and requiring larger allocations by the Fed to keep the market federal funds rate from undershooting the new, higher target range.

So, on a technical level, we see the new IOER/ON RRP framework as a resounding success. But there remain two key challenges for this mechanism of monetary control, one political and another practical. As the IOER rate rises, the Fed will be making larger interest payments to banks--especially to large and foreign institutions who hold most of the balances at the Fed--while scaling back remittances to the U.S. Treasury as profits recede (see here). Populist criticism of these interest payments is already evident and almost sure to grow, potentially posing a real threat to Fed independence (see, for example, Senator Bernie Sanders' New York Times op-ed and this story in the Wall Street Journal).

The second challenge to the Fed's new operational structure comes from the potential for financial instability brought on by an episode of bank stress. If uninsured depositors and other short-term bank creditors were to become concerned about the state of banks, they could switch rapidly--and disruptively--to nonbanks that promise to hold only riskless liabilities in the form of ON RRPs with the Fed (or U.S. government liabilities more generally). Such a disorderly disintermediation could trigger a credit crunch, unless the Fed were to severely limit the volume of ON RRP that it accepts and allow the market funds rate to plunge below the target range, possibly all the way to zero. But perhaps this is the optimal monetary policy response if the alternative is financial and economic disruption.

All that said, the initial experience confirms that the Fed can raise interest rates even though the banking system is awash in excess reserves. By offering to pay interest on reserves, the Fed is placing a floor on the rate banks are willing to lend to households and firms. And, by offering to accept nonbank financial intermediaries overnight reverse repos in large volume, they are creating a floor under the market federal funds rate. If this pattern persists as policy rates rise, the new policy mechanics will be judged remarkably effective. Most importantly, the Fed will have secured the option to adjust its balance sheet gradually as financial conditions warrant, rather than being forced to do so rapidly and disruptively in order to tighten monetary policy. This flexibility is critical not only for Fed credibility, but for the stability of growth and inflation as well.