The sequester advocates have gotten their way. The March 1 has passed to reach an agreement to alter the across the board spending cuts, and so government will begin the draconian job cuts that will certainly slow economic growth this year -- up to 750,000 jobs lost and as much as 0.6 percent off GDP growth if some compromise isn't reached in coming weeks.

This all came about because of a lack of understanding of basic economic principles, propagated by those who should know better. One such economist and deficit hawk is Dallas Fed President Richard Fisher, who is calling for a gradual reduction in QE3 bond purchases this year, because of the "money Ritalin," or artificial boost it is giving to economic growth.

"I think it's really time to taper this off," Fisher said recently on CNBC. "It doesn't mean stop it. We're not going from Wild Turkey to cold turkey. But I do think we've run up to the limits of the efficacy of what we're doing. It's a good time to do it."

He maintains the economy is improving but job creation isn't picking up fast enough. Really? That is precisely why QE3 is so important. Fed Chairman Bernanke recently said "We believe the monetary policies that we've conducted have helped get a stronger recovery and more jobs than we otherwise would have had," during his semiannual Congressional testimony.

What is it that Fisher and the deficit hawks don't understand about Bernanke's statement? Why doesn't Fisher believe the facts; that Fed policies have helped a stronger recovery "than we otherwise would have had?"

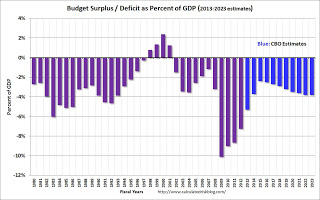

They confuse overall debt with annual deficits, for one. The annual federal deficit is dropping the fastest in history -- and in fact endangering this recovery. While history has shown the only way to reduce overall government debt is by increasing economic growth, which means stimulating job formation and so tax revenues. (Note that economic stimulus shouldn't be a bad word in the context of creating more jobs, since it generates increased revenues to pay down the debt.)

Graph: Calculated Risk

Cutting taxes, which inordinately benefits the wealthiest 1 percent, hasn't stimulated much growth -- especially during the George W. Bush administration which ran up the largest government debt since World War II, accompanying the slowest recovery since then, as well as helping to cause the Great Recession.

The answer to why there are such economic misconceptions should then be obvious. The so-called "debt burden" that economists such as Fisher and even Carmen Reinhardt and Kenneth Rogoff have said slow economic growth, is only a burden if programs aren't in place to stimulate future growth. Cutting government spending for programs that create future jobs (in infrastructure, education, research and development) at a time of weak economic recovery, such as now, only further weakens the recovery.

It's the chicken and the egg conundrum. Will just increasing the supply of money stimulate growth? Not unless it is spent wisely. Conservatives, such as deficit hawks believe that cutting taxes and so government spending puts more money into private pockets. But not when the private sector hoards the increased profits due to a lack of demand for their products, rather than investing it in future growth.

After all, that is the definition of a recession -- falling demand that leads to greater joblessness, due to falling prices or some outside event like the 1970's oil embargos -- that deficit hawks in particular don't want to understand.

It is very basic economics 101. Just cutting spending doesn't reduce debt without also investing in future growth. The sequester job cuts in particular will just diminish the revenues needed to bring down the federal government's overall debt load.