This one's pretty weedy but worth it for those of us interested in the important question of whether our high levels of income inequality are affecting macroeconomic growth. I laid out the basic issues in this earlier post and elaborate on them in a forthcoming piece from CAP, but the part I want to get into in this post relates to inequality and consumer spending.

One hypothesis you hear a lot -- and it's one with legit theoretical grounding -- is that as more growth and income is concentrated at the top of the scale, consumer spending should slow because high income households have lower consumption propensities (they're more likely to save than spend the marginal dollar) than lower income households.

But you don't see that in the macrodata on consumer spending. Take, as an instructive example, the 2000s, when inequality was growing, middle-class incomes were stagnant, yet consumer spending generally held up well. Of course, it could be that wealthy households spent enough to make up for the consumer demand lost to middle-income stagnation, but a) how many fancy cars and watches and houses can they buy?, and b) evidence in this paper by Cynamon and Fazzari shows otherwise.

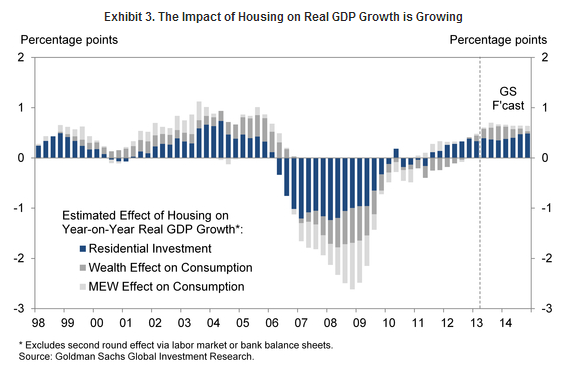

In fact, there was an intervening variable in play: quickly -- and bubbly -- appreciating housing wealth. I was reminded of this dynamic this morning while gazing upon the figure below from a GS research note, showing the contribution to real GDP from housing, decomposed into the investment part, the wealth effect, and MEWs (mortgage equity withdrawals).

In the figure, the wealth effect -- the extra spending you do when your assets appreciate, even if you don't realize the gains -- is scored at four cents on the dollar. That implies that if your home value goes up $50,000 -- no great shakes at all in the bubble years -- you'll spend an extra $2,000. And, sorry to say, visa versa, as the figure clearly reveals.

Be aware that neither higher housing wealth, nor its wealth effect, nor even the MEWs show up in the national income accounts, so if you perfectly reasonably tried to go from income to spending, you'd miss a large part of the action, both on the upside and the downside.

And that downside really jumps out at you. In the depths of the great recession, the imploded housing bubble was snuffing out almost 3 percentage points of GDP, with more than half of that impact coming from lost wealth/equity.

You should also note that inequality was actually coming down in those years, due to capital losses. Thus, if you expected inequality and consumer spending to be inversely correlated, you'd get the wrong sign in both parts of the business cycle. The issue, however, is less that the theory is wrong than the data omits the impact of the housing bubble on spending and thus on growth in an economy that's 70 percent consumer spending.

So, does this imply that inequality is unrelated to growth? As I explain in the CAP piece, no. There are interesting theories and some early evidence linking inequality to this shampoo economic cycle -- bubble, bust, repeat -- in which we appear to be stuck. And as I stress here, I strongly suspect the differing consumption propensity theory is active in the current, demand-constrained economy.

Most of my writing in this area has focused on two problems that concern me most about higher inequality: its linkage to stagnant earnings through the productivity-wage split, and its negative impact on the opportunity set available to the have-nots. But these macroeconomic concerns are also highly worrisome, particularly when you consider the lasting damage done by the bursting of the housing bubble.

Source: GS Research

This post originally appeared at Jared Bernstein's On The Economy blog.