In the age of Piketty, it is increasingly recognized that historically high levels of economic inequality are a serious and growing problem in many economies across the globe. The problems caused by this phenomenon range from stagnant incomes and sticky poverty rates for the majority on the "have-not" side of the divide, to skewed political power (especially, given all the money in politics, here in the US), to possibly slower macroeconomic growth, self-reinforcing wealth accumulation, and a tendency toward terribly damaging bubbles.

The causes of increased inequality are generally viewed to be increased competition through globalization, technological change, diminished union power, lower minimum wages, and persistent slack in the job market, which has the effect of significantly lowering the bargaining power of most workers.

But there's another alleged cause: there's a lot more inequality, especially in earnings, because in this day and age, really talented people are finally able to get paid what they're actually worth (and note that it is rising high-end earnings that explain most of the growth in inequality in recent decades). Some of the factors listed above play a role here, as technology and trade have created access to broad new markets where millions more consumers can interact with producers of entertainment, apps, and clever financial instruments. These forces have helped to unleash the earning power of a small number of individuals who are simply and legitimately earning their "marginal product," i.e., the true value of their contribution to the world (hereafter MP).

Now, I happen to think that's wrong, but contrary to popular opinion, it's actually the first assumption made by economics in evaluating pay. The average person looks at figures showing more wealth or income inequality than ever and sees something out of whack. In economic terms, they see evidence of "rents:" people who are, by dint of some economic inefficiency, being paid well beyond their MP. But the economics textbook sees, by assumption, fair remuneration.

It's both interesting and important to think about why that's wrong. Moreover, it not a simple case to make. For one, an individual's contribution to her firm's bottom line (MP) is awfully hard to back out. Sure, if your factory of 10 workers makes 100 widgets, and, with no changes in technology or prices, you hire one more person and end up with another 10 widgets, you can easily derive the marginal gain. Of course, the real world is more complex.

For example, suppose you could observe relevant market changes wholly outside the control of a CEO and gauge their impact on her compensation. That would make a nice test of the MP theory, since CEO pay shouldn't fluctuate due to such external factors. A clever paper by Betrand and Mullainathan examines just that possibility, through a case study of executive salaries in the oil industry, where the product price is clearly set on the global market. Yet, in contrast to MP assumptions, they find not only that CEO pay in the industry increases with positive price shocks -- "oil CEOs are paid for luck that comes from oil price movements" -- but that the increase tends to be asymmetrical: these execs are paid more for good luck than they lose for bad luck.

Next, there's what I think of as the discontinuity hypothesis, a particularly strong, though nuanced, bit of evidence against the conventional MP theory. The idea here is that if the very talented are finally getting their just desserts, this should occur along a fairly smooth continuum. That is, there's no plausible meritocratic reason why those at the 98th percentile of the skill distribution should be doing just OK while those at the top 0.1 percent are raking in the stuff.

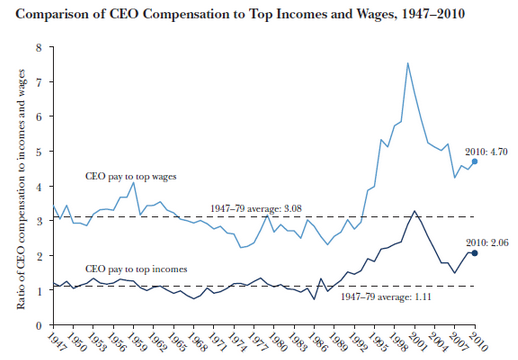

Yet the figure below, from research by Josh Bivens and Larry Mishel, reveals precisely such a discontinuity (their paper is one of the most important in recent years on this question of rents). Each line shows the ratio of CEO compensation to the top 0.1 percent of both household incomes and wages. For decades, the lines wiggled around their historical average, before shooting up sharply in the era of heightened inequality.

Source: Bivens and Mishel, 2013.

While an MP advocate might want to bend herself into a pretzel to describe a model wherein the productivity of the top CEOs pretty suddenly far surpasses that of not the average worker, but the 99.9th percentile worker, such contortions begin to seem implausible, if not desperate. In fact, one problem with the MP assumption is that there is no distributional outcome with which it is inconsistent.

This next example of rent-seeking is the one I find most interesting and perhaps most germane to the nature of inequality today: underpriced risk in finance.

Suppose your company designs cars and a sharp new engineer comes to you with this offer: I can build you a fast, sexy car that gets awesome mileage and is easily affordable to your customer base. Let's say you believe her and offer her a fat pay package of X. Now imagine a similar rap with one twist. Your genius engineer offers you the same car, but adds the fact that it tends to crash a lot. You still might offer her a job, working on risk-reduction. But you'd do so for a fraction of X.

The finance sector, unsurprisingly, has been the focus of some of the most interesting research on rents and a few themes have surfaced, including that of underpriced risk, negative externalities, and the role of deregulation.

First, when someone asks me to explain the Great Recession in two words -- it's happened more than once -- I say "underpriced risk" (or maybe "housing bubble" but they're intimately related). The point in this context is that for years now, finance has supported outsized compensation packages that quite inefficiently fail to reflect the damage that the camouflaged risk of their products pose to the rest of the economy. It's a classic externality problem: the costs imposed by the actions of these financial "innovators" have clearly not been netted out of their compensation.

It's even worse. Not only have they been overpaid relative to the damage their sector has caused, but many of them and their institutions have been made whole at the taxpayers' expense once the depressed risk pricing was revealed and the bubble burst.

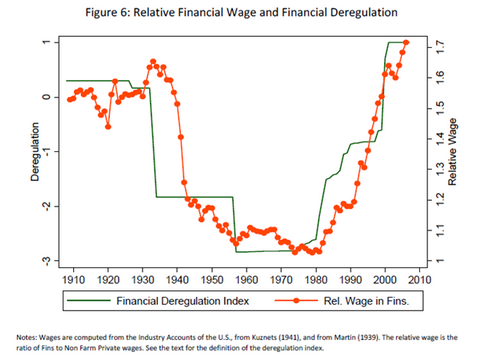

Aren't the financial regulators supposed to prevent this? Of course, but the fact that they've been outgunned by lobbyists and in many cases, seemingly captured by the finance industry, has them playing catch-up at best, and this too is major contributor to rents. Take a look at the figure below, from a paper by Philippon and Reshef that plots an index of financial deregulation against relative pay in the industry (an increase in the deregulation index implies looser regulation).

Source: Philippon, Reshef (2009).

The fit between deregulation and pay in finance relative to the economy-wide average is tight, but does this really disprove MP theory? Perhaps it just shows that when you un-cuff Adam Smith's invisible hand, it works efficient wonders that plodding regulators were formerly blocking. Yet, along with the pretty dispositive negative externality point above, there's a growing body of work relating the growth in the finance sector to price distortions (overpriced financial intermediation), unproductive rent-seeking, and of course, systemic risk.

I could go on in far greater detail, but I'll spare you, other than to note that other advanced economies facing the same technological and global forces as us fail to pay their executives so exorbitantly. One area where this is particularly clear -- where "rents" seem excruciatingly obvious -- is in health care, where pharmaceutical and physician lobbies continue to extract hugely higher costs than are seen elsewhere for similar goods and services.

Finally, what about the superstars? As economist Greg Mankiw argues, it's not at all obvious that Robert Downey, Jr. didn't deserve $50 million for playing Iron Man in a recent film. Again, Mankiw's arguing by assumption -- the actor must deserve $50 mil because he got $50 mil -- but it's harder to see the market failure here than on Wall St.

Here though, I'd evoke Bivens and Mishel's notion of rents or as they call it, "inefficiently high pay:" paying someone more than you need to in order to get them to do the job. I too am in the realm of assertion here, but I'll bet Downey would have done the job for $45 million, though research on "positional pay" suggests he'd only go there if his nearest competitor took a similar pay cut (if I'm wrong about all this, Bob, have your people call my people). Heck, I'd take the part for a couple hundred K -- could I really be $49.8 million worse than Downey?

OK, now I'm arguing by assumption so let's stop. But to look at the inequality landscape and sweepingly assume, with Panglossian certainty, that this is the best and most just of all possible income distributions looks to me to be in pretty deep denial of the evidence and the historical record. And the policy implications of this evidence are actually profound: once you accept that our economy is functioning ever less as a meritocracy, you pave the way -- at least you should pave the way -- for a lot of corrective public policy, starting with more progressive taxation on high earnings and wealth.

___________

This post originally appeared at Jared Bernstein's On The Economy blog.