Update (4:15PM EST):

OK. In my last update I vented about how political gridlock got us here and threatens to keep us here. But remember, this is America! We don't lie down, throw up our hands, point our fingers, and give up! We roll up our sleeves and try to fix stuff.

So, what should we do right now? Here are some thoughts, in order of political plausibility.

- The Fed needs to step up. I know... I've argued there's not a lot monetary policy can do on its own right now. My point is that interest rates are already low, investors are pretty flush with cash, and anyway, investment is the one part of GDP that's been pretty reliably growing. Still, all that said, another round of quantitative easing is called for. After all, the FOMC themselves have been saying that if things get worse, they'll pull that trigger. Well, things are worse.

- Do no harm. Readers of my blog know that I do not blithely play the uncertainty card. What's held back growth and hiring in this economy is not clause #572/7 from the Affordable Care Act or the EPA or the 75 year fiscal outlook. It's the near term demand contraction. But I've started citing the problem of uncertainty regarding upcoming fiscal issues and this is something Congress could quickly fix if enough of them grasped the urgency of the situation.

And it's not just market uncertainty I'm thinking of here. There are millions of people working for government contractors who could get stung if automatic cuts hit all at once. Tax increases, along with the loss of the payroll tax break will bite paychecks that are already, on average, falling behind inflation.

That doesn't mean we should extend all the expiring provisions--that would be worse than doing nothing at all. But if the deceleration of job growth we've just seen doesn't convince these folks to put aside their differences and compromise on behalf of working Americans, then they've got no business being here.

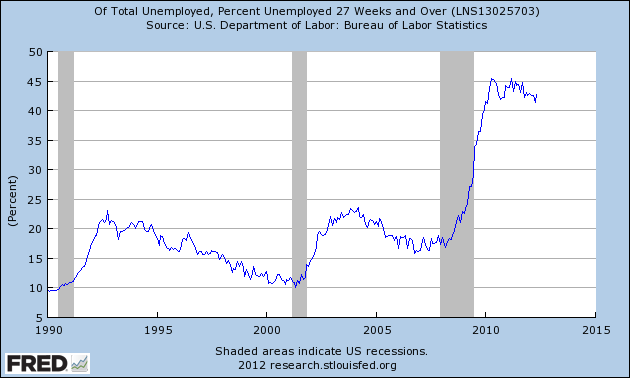

- Keep extended UI going. Extended Unemployment Insurance benefits are just about as necessary as ever, yet the extended benefits program is actively winding down across the nation, as my CBPP colleague Hannah Shaw shows here. Yet, 5.4 million jobless folks -- 43% of the unemployed-have been out of work for at least half a year, and, as shown in the figure, that share hasn't come down much at all.

And since the unemployed... um... don't have jobs, they tend to spend these benefits generating useful multiplier effects.

- Enact fiscal stimulus. Finally, and almost certainly leaving the realm of political reality, measures like state/local fiscal relief and FAST! would help a lot right now.

Now, let's say the Fed acts, which as I said, would be good but not enough. And let's say UI and more stimulus are off the table.

That leaves "do no harm" and that strikes me as perhaps, maybe, I-doubt-it-but-who-knows possible. I suspect it would actually help the economy in no small way if Congress said to America:

We disagree on many fundamental points about the role and size of government. But one thing on which we stand shoulder-to-shoulder is that the American people should not have to suffer because of our disagreements.

We face today a number of fiscal issues that must be resolved in coming months and given what we just learned today about the job market, we've decided to take one big set of worries off the table.

By working together and compromising, we've come to an agreement that avoids the fiscal cliff and lifts the debt ceiling today. We didn't fix everything forever--we'll need to revisit these tough issues in coming months. But despite our inherent differences, there's no way we're going to inflict any more wounds on this economy at a time like this.

I can dream, can't I?

_____________________________

Update (1:28PM EST): I see a lot of the wire reports on the lousy jobs release focusing on Europe, China, and other external factors to explain why employment growth once again appears to have decelerated.

Sure, European instability and a slower growing China are part of the problem. But they are not at its core. For that, we've simply got to look in the mirror.

The economic reason the job market is once again downshifting is because we as a nation failed to take out recovery insurance in the form of temporary stimulative fiscal policy against precisely the situation we now face.

The president proposed the American Jobs Act back in September of last year for just this reason. The economy in general, but especially the job market, has never reliably achieved "escape velocity," i.e., consistently high enough growth rates that would set off the virtuous growth cycle of more jobs leading to more incomes, more consumption, which feeds back into greater demand, more jobs, etc.

And the thing that has blocked us from taking out the insurance we needed was and is political gridlock. In fact, it's worse. Beyond gridlock, dysfunctional Congressional politics have led to self-inflicted wounds to the economy, wounds that are being freshly reopened with talk of going over the fiscal cliff, another debt ceiling fight, and the loss of extended unemployment insurance benefits for hundreds of thousands of jobless persons.

When politicians come to Washington not to solve our immediate pressing problems, not to compromise, but to promote, above the public interest, a narrow political agenda -- when they do so regardless of the degree of hardship in the current economy -- then I'm afraid we shouldn't be surprised at our inability to self-correct.

_____________________________

Original post (9:22AM EST): The Bureau of Labor Statistics just released the employment and unemployment results for May and the results solidly confirm that the pace of job creation has once again slowed significantly.

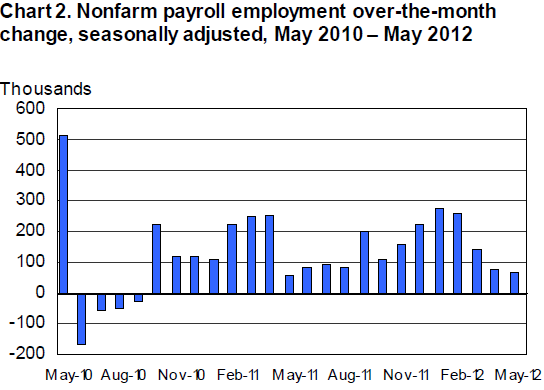

Job growth for May came in at only 69,000 jobs, the worst month in a year. Unemployment ticked up to 8.2%, but that was largely due to more people coming back into the job market. Moreover, April's already weak jobs number was significantly revised downward, to 77,000, a markdown of 38,000 jobs. Weekly hours worked ticked down a bit as well, further confirming the weakening labor demand story told by these numbers.

The deceleration in payroll job growth is alarmingly clear (see figure). It's important to average the past few months to get a better feel for the underlying trend in these data. Over the past three months, net job gains have averaged 96,000 per month, compared to 252,000 in the prior three months.

Source: BLS

These jobs data come from a survey of workplaces, while the unemployment rate comes from a household survey. As is sometimes the case, the two surveys revealed very different results in today's release. Employment growth was strong in the HH survey -- up 422,000 -- but analysts discount this monthly number as the underlying sample is a lot smaller and much more volatile, month-to-month.

Nevertheless, even with this job growth from the HH survey, unemployment rose because the labor force expanded and enough people already in and newly entering the job market were jobless last month to send the rate up one-tenth, to 8.2%.

I'll get into the gory details later, but wow... as it looks today, the job market is simply not providing workers with the employment and earnings opportunities they need to get ahead. This has obvious negative implications for family budgets, but it also threatens the macro-economy. If this pace of job growth sticks, the economy will slow down from a growth rate that's already too slow.

So, will it stick? It's always possible with these monthly reports that some statistical anomalies are in play. A candidate in this case is weather effects, as unseasonably warm weather last winter probably moved job growth that might have occurred in May to earlier months.

If so, that would imply that taking an average of more months of data would give you a more accurate read on the true underlying pace of growth. Over the last six months, net monthly job gains have been 174,000, so a lot depends on whether the current weak trend persists.

However, while one month does not a trend make, three months do. Also, slower job growth is consistent with a number of indicators that slowed in May, along with Europe and fiscal uncertainty regarding the fiscal cliff.

In my next update, I'll get deeper into the numbers and talk about what we should be doing about this tough situation we've put ourselves in by failing to apply more stimulus when the economy clearly hadn't fully recovered from the Great Recession.

This post originally appeared at Jared Bernstein's On The Economy blog.