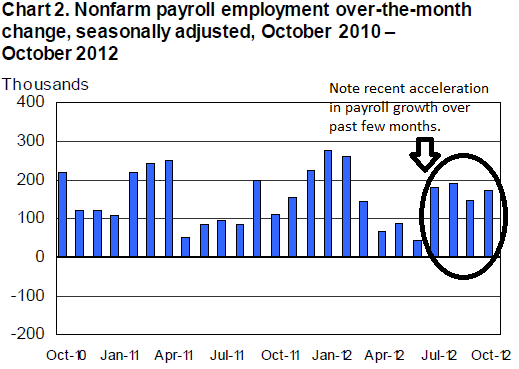

Well, the big jobs report is out showing payrolls grew by a more-than-expected 171,000 last month and the unemployment rate ticked up slightly, as expected, to 7.9%. Job growth for the prior two months was revised up by 84,000, and the average monthly pace of job growth over the past four months-a useful way of smoothing out monthly noise in the data-is 173,000, a sharp acceleration over the second quarter's pace of 67,000 per month (see figure).

The uptick in unemployment was expected after September's 0.3 percentage point drop, but a few things are worth noting. First, the 0.1 point increase is statistically indistinguishable from no change at all-the unemployment rate has to rise or fall about 0.2 points to be significant. At 7.9%, the jobless rate is down significantly-by one full point-from its rate one year ago. Second, one reason for the slight uptick was more people coming into the labor market seeking work. We'll need to see how this development evolves in coming months, but we may be seeing early signs of an improving job market pulling more job seekers in from the sidelines.

All told, given the acceleration in payroll growth, the upward revisions to prior months payroll gains, the trend decline in unemployment, and the pick-up in labor force participation, today's report is generally pointing to job market that's showing signs of improvement.

Obviously, a report like this just a few days before a tight election is going to be a very big deal, and both campaigns will use the results in predictable ways. But if there's anyone out there who's making up their mind based on this one report, please don't. Yes, the monthly employment numbers provide important information about the part of the economy that matters most to people, but that information must be considered as but one relatively noisy set of indicators amid a sea of others.

I always stress, as I did above, the importance of smoothing out some of the monthly noise by averaging over the past few months. As noted, employment growth slowed notably in the second quarter of this year, increasing by only 67,000 jobs per month, but has since accelerated up to an average monthly gain of about 170,000 over the past four months.

- The effects of hurricane Sandy are not in these numbers as the October surveys were fielded well before the storm hit.

- Manufacturing added 13,000 jobs last month, after shedding 14K and 13K jobs in the prior two months. Over the past year, factory employment is up by 189,000, and up about 500,000 since the sector began to recover in early 2010.

- Both hourly and weekly earnings are up, before inflation, by about 1.5% over the past year, trailing the recent trend in prices, up around 2% since last September. Average weekly hours have also been flat over the past few months, suggesting employers are meeting increased labor demand by adding workers rather then extending shifts.

- Most industries added jobs last month; professional services led with 51,000 jobs, retail stores added 36,000 jobs in October, compared to 27K and 18K in the prior two months, perhaps reflecting stronger consumer activity and confidence.

- Construction was up 17,000 last month, driven by both residential and commercial contract work. The sector is showing some early signs of the formerly moribund housing market coming back to life.

- Government employment, however, fell again in October, down 13,000. After posting large losses since the downturn, over the past state and local payrolls have been essentially stagnant.

This post originally appeared at Jared Bernstein's On The Economy blog.

Our 2024 Coverage Needs You

It's Another Trump-Biden Showdown — And We Need Your Help

The Future Of Democracy Is At Stake

Our 2024 Coverage Needs You

Your Loyalty Means The World To Us

As Americans head to the polls in 2024, the very future of our country is at stake. At HuffPost, we believe that a free press is critical to creating well-informed voters. That's why our journalism is free for everyone, even though other newsrooms retreat behind expensive paywalls.

Our journalists will continue to cover the twists and turns during this historic presidential election. With your help, we'll bring you hard-hitting investigations, well-researched analysis and timely takes you can't find elsewhere. Reporting in this current political climate is a responsibility we do not take lightly, and we thank you for your support.

Contribute as little as $2 to keep our news free for all.

Can't afford to donate? Support HuffPost by creating a free account and log in while you read.

The 2024 election is heating up, and women's rights, health care, voting rights, and the very future of democracy are all at stake. Donald Trump will face Joe Biden in the most consequential vote of our time. And HuffPost will be there, covering every twist and turn. America's future hangs in the balance. Would you consider contributing to support our journalism and keep it free for all during this critical season?

HuffPost believes news should be accessible to everyone, regardless of their ability to pay for it. We rely on readers like you to help fund our work. Any contribution you can make — even as little as $2 — goes directly toward supporting the impactful journalism that we will continue to produce this year. Thank you for being part of our story.

Can't afford to donate? Support HuffPost by creating a free account and log in while you read.

It's official: Donald Trump will face Joe Biden this fall in the presidential election. As we face the most consequential presidential election of our time, HuffPost is committed to bringing you up-to-date, accurate news about the 2024 race. While other outlets have retreated behind paywalls, you can trust our news will stay free.

But we can't do it without your help. Reader funding is one of the key ways we support our newsroom. Would you consider making a donation to help fund our news during this critical time? Your contributions are vital to supporting a free press.

Contribute as little as $2 to keep our journalism free and accessible to all.

Can't afford to donate? Support HuffPost by creating a free account and log in while you read.

As Americans head to the polls in 2024, the very future of our country is at stake. At HuffPost, we believe that a free press is critical to creating well-informed voters. That's why our journalism is free for everyone, even though other newsrooms retreat behind expensive paywalls.

Our journalists will continue to cover the twists and turns during this historic presidential election. With your help, we'll bring you hard-hitting investigations, well-researched analysis and timely takes you can't find elsewhere. Reporting in this current political climate is a responsibility we do not take lightly, and we thank you for your support.

Contribute as little as $2 to keep our news free for all.

Can't afford to donate? Support HuffPost by creating a free account and log in while you read.

Dear HuffPost Reader

Thank you for your past contribution to HuffPost. We are sincerely grateful for readers like you who help us ensure that we can keep our journalism free for everyone.

The stakes are high this year, and our 2024 coverage could use continued support. Would you consider becoming a regular HuffPost contributor?

Dear HuffPost Reader

Thank you for your past contribution to HuffPost. We are sincerely grateful for readers like you who help us ensure that we can keep our journalism free for everyone.

The stakes are high this year, and our 2024 coverage could use continued support. If circumstances have changed since you last contributed, we hope you'll consider contributing to HuffPost once more.

Already contributed? Log in to hide these messages.