One of the more important economic questions of the day is the one I pose, but alas, do not answer here: Is an acceleration in labor-saving technology displacing workers in a historically unique and problematic manner? Will the increasing presence of robotics and AI software make it harder to achieve full employment?

Most economists say no, because they're all hung up on evidence and history -- imagine that. Of the evidence, it's mostly anecdotal, as per these guys, who've certainly influenced my thinking on the issue. On history, as I always stress, the past is littered with the prediction that technology is replacing workers in a lasting way.

And yet -- there may be something there.

The idea gets a nod from Paul Krugman this morning. The traditional technology story is that it's just "skilled-biased" -- it gives a relative wage edge to say, college-educated workers. Paul argues that even that part of the story didn't explain increasing inequality well enough, because it failed to account for the intensive income concentration among not just college grads, but the top 1 percent (for that, you need to incorporate financialization and power into your model). But he goes on:

Today, however, a much darker picture of the effects of technology on labor is emerging. In this picture, highly educated workers are as likely as less educated workers to find themselves displaced and devalued, and pushing for more education may create as many problems as it solves.

I'm not sure I'd go that far, though he's right that college workers were by no means insulated from the recession -- trough to peak, both high-school and college grad jobless rates more than doubled (the college unemployment rate went from around 2 percent when the recession began to 5 percent at its peak; the HS rate, from about 5 percent to 11 percent at its peak).

Paul also cites the historically low level of labor's share of national income. That's true too and certainly reveals that income inequality remains a serious problem as economic growth in this recovery is once again looking like a spectator sport for most working households ("it's early in the first half, and look at that folks... Paulson goes long on gold and...and...he's down a few hundred million...and whose got it? It looks like Buffett's intercepted it at midfield...he passes to Goldman, they securitize the asset at the 45 and slip it downfield to the China market...etc...")

But my question has more to do with jobs, and we've seen periods of growing inequality with pretty robust job growth, i.e., the 1980s (I'm talking job quantity here, not quality), and periods with growing inequality with lousy job growth, i.e., the 2000s.

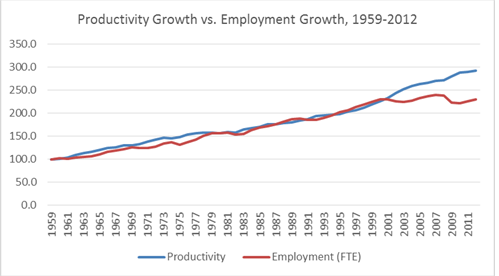

In this regard, the anti-Luddites -- those who argue that history has been unkind to the argument that technology displaces workers (which is subtly different than "it lowers their relative wages") -- point to the long linkage between productivity growth and job growth. If technology were increasingly labor saving, these lines should diverge. They don't, so goes the argument, because of the intervening variable of demand, which increases as we become more productive thus absorbing those who would suffer technological unemployment back into the workplace.

Except for since around 2000, the lines don't converge. The figure below plots full-time equivalent employment against productivity, and the anti-Luddites to whom I've showed this find it a head-scratcher. On the other hand, it makes sense to Brynjolfsson and McAfee, the authors of Race Against the Machine (see link above), and on alternative Wednesdays, to me.

On the other hand, Dean Baker points out that productivity hasn't much accelerated over the period of the split, which you'd expect if labor saving technology was a key factor. More wonkishly, the growth of capital inputs into total factor productivity has considerably decelerated over the last decade, the opposite of what a Luddite might expect. That just means that there's been a slower rate of capital spending feeding into growth relative to earlier periods. (But wait--if labor's share is tanking doesn't that mean capital's share must be rising? Yes, but interestingly, not because of accelerated investment but because of a higher return on capital -- and lower return to work -- see "spectator sport" point above.*)

All of which is to say is that we just don't yet know the extent to which tech is displacing workers. One way to think about it is to ask yourself "in terms of job growth, are we at the cusp of a period that will resemble the 1990s expansion or the 2000s expansion?" The latter sucked for job growth; the former was strong in that regard.

Me, I fear that the path back to full employment is looking very steep, and I suspect accelerated labor-saving technology is one reason for that. So I'm keeping my powder dry and my spreadsheets open.

Source: Moi

*Here's what I'm talking about:

Y=Kr+Lw: national income equals captial (K) times its return (r), and labor (L) times its return (w, for wage).

Divide through by Y to get shares: 1=(K/Y)r+(L/Y)w.

We know that L/Y is going down fast, and w is stagnant. But (K/Y) isn't growing that fast. So r must be rising quickly.