Several industries tied to metals and manufacturing are among the slowest-growing in the U.S., according to recent data from Sageworks, a financial information company.

While privately held companies on average have been growing annual sales by more than 8 percent over the past 12 months, a handful of industries are seeing flat or lower sales, based on preliminary data from Sageworks' financial statement analysis. Subsectors related to metals make up three of the five slowest-growing industries. A third of the bottom 15 are related to manufacturing, a sector that experienced double-digit sales growth in 2011 and 2012 but has since experienced slower growth.

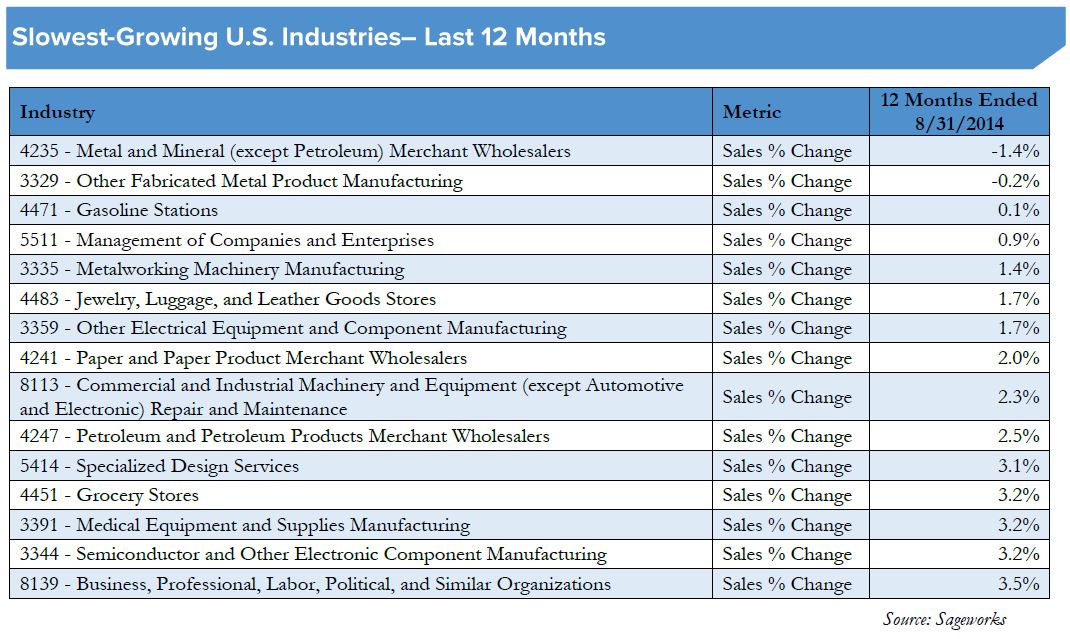

The worst-performing industry by change in sales? Metal and mineral merchant wholesalers, a category that includes metal service centers, the go-between that purchase metals from mills and distribute them to manufacturers, often after cutting, finishing or otherwise handling the metals. This industry (NAICS 4235) had a 1.4 percent drop in sales over the year ended Aug. 31.

Fabricated metal product manufacturers, which include makers of metal industrial valves, fabricated pipes and bearings, had a 0.2 percent sales decline, according to Sageworks' data.

"The first thing it's important to remember is that with the exception of these two industries, all of these industries have positive sales growth, so they have increased sales over the last year, even if they're not increasing sales as fast as the average for all private companies," said Sageworks analyst Jenna Weaver.

Other industries in the bottom 15 include: gasoline stations, grocery stores and manufacturers of metalworking machinery, semiconductors, medical equipment/supplies and a category of electrical equipment that includes batteries and fiber optic cables.

Weaver said it's unclear from Sageworks' data what's behind the sluggish sales trends among metals-related industries. But outside data show prices of many base metals and raw materials for steel have been dropping since 2011 as oversupplies encounter cooling demand from China, a top metal consumer.

"We've seen the prices of metals dropping, and that can come into play for some of these wholesalers and manufacturers in that they may not be able to get the same price as they once did for their products," Weaver said. "We have to remember the sales growth metric is a factor of both the price the company is able to charge for the product or service and the amount or volume of the product or service sold."

In many instances, the drop in prices may be tied to lower demand, providing a double hit to sales growth prospects.

Weaver said that it may seem obvious, but how much revenue a company or industry generates is important, because it drives many other financial ratios on the income statement and the statement of cash flows. Still, she noted, revenue is but one indicator of an industry or company's financial health, and it should always be reviewed in conjunction with other metrics, such as profitability, cash flow and liquidity in order to get a more compete view.

Besides the metals-dependent industries, many other industries on the list of slowest-growing subsectors are also either selling products that are commodities or are using a commodity as a major raw material. For example, sales at gasoline stations increased only 0.1 percent over the last 12 years, but station owners have to balance their retail prices with rapidly changing prices they pay for the product. Selling commodities or selling products that are made with commodities can often create pricing challenges for those businesses.

Only two service-based industries were on the most recent list of slow-growing industries: Management of companies and enterprises, which includes holding companies, and specialized design services. This sub-industry includes interior, industrial and graphic design.

Through its cooperative data model, Sageworks collects financial statements for private companies from accounting firms, banks and credit unions, and aggregates the data at an approximate rate of 1,000 statements a day. Net profit margin has been adjusted to exclude taxes and include owner compensation in excess of their market-rate salaries. These adjustments are commonly made to private company financials in order to provide a more accurate picture of the companies' operational performance.