February 2013 saw a strong jobs performance and a significant decrease in the U-3 broad unemployment measure. Employment increased by 236,000 net new non-farm payrolls. The broad U-S unemployment measure fell from 7.9% to 7.7%. We did see the January 2013 revision remove 38,000 from the previous report, a reduction to +119,000 from +157,000. The U-6 broad measure of unemployment, that includes involuntary part-timers and the discouraged, was stubbornly high in February 2013, falling to 14.3% from 14.4%. The employment scene remains very difficult for the out of the work, the marginally attached, the young and the less educated. This explains a public far less convinced of recovery than elites.

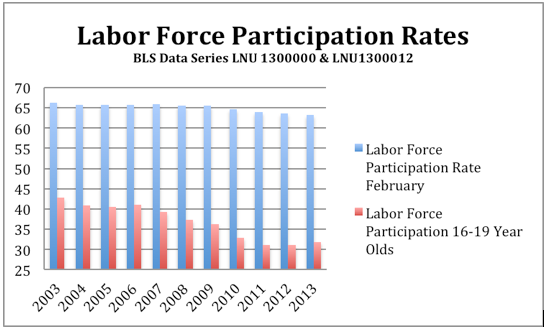

As we enter the Sequester we must suspect employment and economic weakness to tick higher, all else held equal. In February 2013 the government sector was weak, losing 10,000 net jobs on weakness from states, down 8,000 jobs. Construction was a strong contributor to job growth adding 48,000 net new jobs across February. Labor force participation rates continued to be weak and were down slightly overall in February 2013. Our economy is less inclusive and more unequal than it was before 2008. Given our high and rising levels of inequality this is acting as a drag on opportunity and economic growth.

A portion of the decline in unemployment has driven by people dropping out of the labor force. This is consistent with over 40% of our unemployed that have been out of work for 27 weeks or longer. Between longer term unemployed and the drop-outs from the labor force the employment "big tent" is smaller than it has historically been. Labor force participation among the young remains disturbingly low.

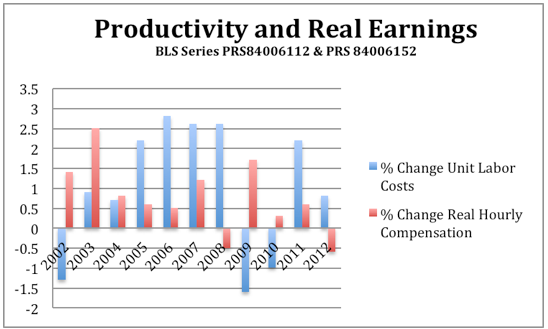

We have seen rapid rises in productivity and dramatic falls in unit labor costs slow. Productivity measures how much output workers create with an hour of work. Unit labor costs measure the changes in output against the employer cost of paying workers for production. As the below chart makes clear, American workers have been doing more for less for years now. This appears to be slowing or reversing. Output is no longer increasing much faster than hours worked. This tells us that producing more with lower head counts and fewer hours worked -- dramatic features of the Great Recession -- have decelerated. The period of rising profits with stagnant to declining wages and elevated unemployment, may have run its course. This is actually positive, as it has contributed to muted labor demand, stagnant wages and long period of weakness in the job market.

February put up strong initial job numbers and significant one month declines in the broad measure of unemployment. We continue to see weakness in wages and employment compared to profits and asset price performance. The slowing of productivity, negative growth in Q4 2012, is likely creating a situation where more hours or employees are required to increase output. This will be supportive to employment and wages if it keeps up. We have had an unusually and fairly savage period for wages and employment opportunities. However, the newer trend, if it holds, suggests that corporate profits may under perform wages and employment.

Improvements in private market hiring and wages are becoming vital. We will continue to see cuts in government services, rising costs of services and net job losses in the public sector. This has also been a feature of the U.S. economy since 2011 and is accelerating. As the federal, state, and local governments do less for folks in need, and charge more for what they do, people in the middle and lower rungs of the distribution tend to suffer disproportionally. We really need the overdue increase in jobs and wages now.