When the Census Bureau released its report on state- and district- level school spending a few weeks ago, news outlets across the country made futile attempts to compare the return on investment of their local school districts with those in neighboring states. Because education lacks standard accounting practices, fairly comparing per-pupil expenditures across states is next to impossible. What constitutes per pupil expenditure in one state is different from another, and how expenditures are reported depends on who's doing the reporting.

If you are a superintendent looking to find more money for your schools, you can report the number in a way that makes them look underfunded. If you are a state legislator looking to send less money to public schools, you can report the numbers in a way that makes them look overfunded. If you're a taxpayer interested in how your tax dollars fund your local school, well, you're out of luck.

Determining per pupil expenditure relies on a series of decision rules that vary. Should states report current expenditure or total expenditure (which includes capital outlays and debt services)? Is expenditure the total revenue collected and disbursed to the public schools, or the amount that the district actually spent?

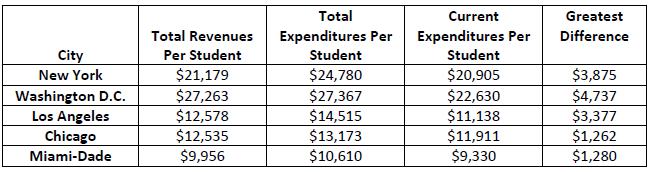

Perhaps most importantly, the method you use to calculate costs affects the final total. To highlight the discrepancies that can exist, I compiled three different calculations of per pupil expenditures from five large, well-known school districts (based off data from the Census Bureau Report). As you can see from the right-most column, the per-pupil expenditure varies widely depending on how cost is calculated.

This is not acceptable. What if we discovered that a private company had changed the way it calculated costs to overstate its return on investment? Remember Enron, anyone?

In order to prevent such malfeasance, our friends in the accounting community have developed a tool called GAAP, or Generally Accepted Accounting Principles, that hold companies to the same standards. If an investor has a question about the stats of a company, he or she can have confidence in the analytic reports that are produced because they must conform to a universally agreed upon standard. When a norm established by GAAP is violated and numbers are no longer trusted (as was in the case of Arthur Andersen watching Enron), accounting firms go out of business. The American Institute of Certified Public Accountants starting regulating themselves in 1887, and today GAAP is defined by a non-profit organization, the Governmental Accounting Standards Board. Education stake-holders could benefit from this kind of streamlined accountability.

Education finance needs GAAP, desperately. Discussions about stretching the school dollar and return on investment depend upon it. States cannot learn from each other if they are using separate cost calculations.

It appears that our friends in the business world realized that it was in everyone's best interest to make decisions based on accurate information. Some people have used that information to make bad decisions and lost their shirts, others have used it to make millions. At minimum, there has been a level playing field by which to base their investments. In the end, that is what we want for schools as well.