Co-written by Associate Professor Hokyoung Blake Ryu

A large part of developing innovative offerings is to correctly perceive and manage risk in the design process. The best strategy seems to be taking more risk early on in the process when exploring opportunities and then continuously clarifying and reducing risk as criteria and design crystallize.

Traditionally, design performance is determined by the team members' combination of personalities (values, beliefs, attitude and behavior), professional competencies (knowledge, skills and experience). However, little to no attention has been given to understanding how the team's risk perception and decision biases affect design performance.

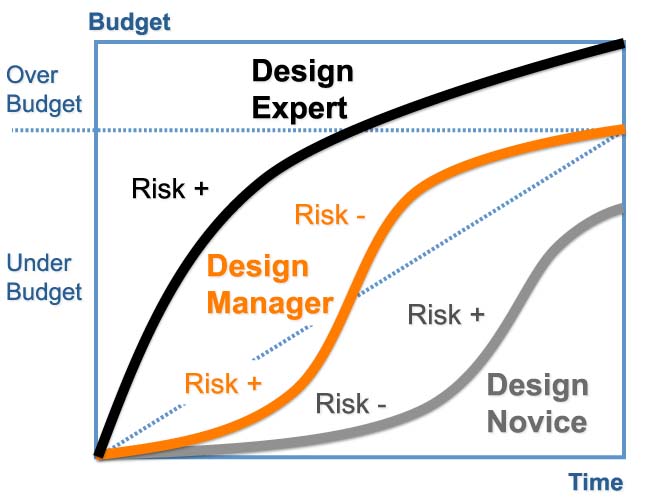

Informal semi-structured interviews with experienced project managers and design educators suggest that novice designers, expert designers and experienced project managers handle design projects in three distinctly different ways. See illustration.

a) Novices designers are risk-averse (R -) in the beginning of the project phase and take on excessive risk (R +) at the end of the project phase. They procrastinate and rely on the pressure of deadlines for creativity and decision-making. Consequently, they tend to waste time in the earlier design stages, resulting in under performance.

b) Expert designers take on considerable risk (R +) throughout each project phase. Overconfidence and a commitment to perfection can cause them to rely on internal motivation to drive a high level of design outcome from start to deadline. They are inclined to over-invest their time for this ideation stage and consequently over deliver and go over budget.

c) Experienced project managers take risk (R +) in the beginning of projects and become risk averse (R -) at the end of the project phases. They limit time on projects in the beginning and invest the time later when key criterion has been resolved and risk reduced. Consequently, they customarily deliver on all project criteria.

Creative professionals on a social professional network were invited to share their experiences with balancing risk taking and risk aversion and their conversations provided the following insights:

1) Risk begins with interpreting the user's need and encompasses the complete life-cycle of the offering. This includes identifying and characterizing several risks at each step of the project, such as schedule, resources, design idea choices and activities. It is essential to think though the product-life-cycle of the offering and weigh the cycle according to probabilities.

2) It is important to focus on the conceptual phase and the worst case/highest probability items of implementation and to define backups or ways to mitigate each of these. The cost of correcting errors escalates from one phase to another by a factor ten, so that correction made in product design is ten times more expensive than errors made in testing, which again is ten times more expensive than errors done in the design process.

3) Individual team members' risk preferences change over time and past experiences can color their risk preferences so that someone who has been severely "burned" naturally becomes more risk averse.

Previous studies show that the seam between marketing and design and the translation of customer information into design briefs remains a challenge, so, focusing on the right mix of strategy, context and execution can assist in providing the critical design quality criteria for final execution.

As inaccurate risk perceptions, fruitless risk preferences and decision-biases arise during the design process, how does one make designers aware of these pitfalls and support them in increasing their design performance?

For the critical conceptual phase, where the cost of failure is highest, identifying ways of changing how we think and approach risk in design could offer huge benefits. The approaches we have identified are: Design quantification (metrics for how designers support their concept with storytelling), behavioral economics (how people actually make decisions as opposed to purely rational decisions) and persuasive technologies (changing user's attitudes or behaviors through persuasion and social influence). Combined, these methods could identify critical aspects, analyze perceived and real risk and foster informed risk preferences.

Murphy's Law states: "If anything can go wrong, it will," so the biggest risk might be to be confident that one has defined all possible risks.

Special thanks to Associate Professor Hokyoung Blake Ryu for researching and co-writing this article.